Securing affordable auto insurance in Indiana can feel like navigating a maze, but understanding the key factors influencing premiums empowers you to make informed decisions. This guide unravels the complexities of the Indiana auto insurance market, providing practical strategies to find the best coverage at the most competitive price. We’ll explore various insurance providers, discuss the impact of driving history and lifestyle choices, and offer actionable tips to lower your premiums.

From comparing minimum coverage requirements to understanding the benefits of various discounts, this resource equips you with the knowledge needed to confidently navigate the Indiana insurance landscape and obtain the most suitable and cost-effective policy for your individual needs. We will examine the influence of factors like vehicle type, location, and driving habits on your insurance rates, helping you identify areas where you can potentially save.

Understanding Indiana’s Auto Insurance Market

Navigating the Indiana auto insurance market requires understanding several key factors that influence costs and coverage options. This information will help you make informed decisions about your insurance needs and find the best policy for your circumstances.

Indiana’s auto insurance costs are influenced by a variety of factors. These include your driving history (accidents, tickets), age and gender, the type of vehicle you drive (make, model, year), your location within the state, and the coverage levels you choose. Higher risk profiles generally lead to higher premiums. For example, drivers with multiple speeding tickets or a history of accidents will typically pay more than drivers with clean records. Similarly, living in a high-crime area or driving a high-performance vehicle can increase your insurance costs.

Types of Auto Insurance Coverage in Indiana

Indiana, like other states, offers various types of auto insurance coverage. Understanding these options is crucial for choosing a policy that adequately protects you and your vehicle. These coverages are often bundled together, but can also be purchased individually (though minimum coverage requirements must be met).

- Liability Coverage: This is the most basic type of auto insurance and is required in Indiana. It covers bodily injury and property damage caused to others in an accident where you are at fault. Liability coverage is expressed as a three-number limit, such as 25/50/25. This means $25,000 per person for bodily injury, $50,000 total for bodily injury in an accident, and $25,000 for property damage.

- Uninsured/Underinsured Motorist Coverage: This coverage protects you if you’re involved in an accident with an uninsured or underinsured driver. It can cover your medical bills and vehicle repairs if the other driver doesn’t have enough insurance to cover the damages.

- Collision Coverage: This covers damage to your vehicle caused by an accident, regardless of who is at fault. This includes collisions with other vehicles or objects, such as a tree or a fence.

- Comprehensive Coverage: This covers damage to your vehicle caused by events other than collisions, such as theft, vandalism, fire, or hail damage.

- Personal Injury Protection (PIP): PIP coverage pays for your medical bills and lost wages, regardless of who is at fault in an accident. It can also cover the medical expenses of your passengers.

Minimum versus Recommended Coverage Levels

Indiana mandates minimum liability coverage, but these limits might not be sufficient to cover significant damages in a serious accident. While Indiana’s minimum liability coverage is 25/50/25, many insurance professionals recommend higher limits, such as 100/300/100 or even higher, depending on individual circumstances and assets. Similarly, while not mandated, uninsured/underinsured motorist coverage and collision/comprehensive coverage are highly recommended to protect against various risks. Failing to carry adequate coverage could leave you financially responsible for substantial costs in the event of an accident.

Average Auto Insurance Costs in Indiana Cities

Average auto insurance premiums vary across Indiana cities, reflecting differences in factors like accident rates, crime rates, and population density. The following table provides a general comparison (Note: These are average estimates and actual costs will vary based on individual factors):

| City | Average Annual Cost | City | Average Annual Cost |

|---|---|---|---|

| Indianapolis | $1200 | Fort Wayne | $1100 |

| South Bend | $1050 | Evansville | $950 |

Finding Affordable Auto Insurance Options

Securing affordable auto insurance in Indiana requires a strategic approach. By understanding the factors influencing your premiums and actively employing cost-saving strategies, you can significantly reduce your annual expenses without compromising necessary coverage. This section Artikels key strategies and considerations to help you find the best value for your auto insurance needs.

Strategies for Reducing Auto Insurance Premiums

Several factors directly impact your auto insurance premiums. Choosing a vehicle with safety features, maintaining a clean driving record, and bundling insurance policies can lead to substantial savings. Furthermore, exploring different coverage options and comparing quotes from multiple insurers is crucial for finding the most competitive rates. Consider increasing your deductible to lower your premiums, but carefully weigh this against the potential out-of-pocket expense in case of an accident. Finally, maintaining a good credit score can also positively influence your insurance rates.

Impact of Driving History and Credit Score on Insurance Rates

Your driving history is a primary factor in determining your insurance premiums. Accidents, traffic violations, and even the number of years you’ve held a license all contribute to your risk profile. A history of accidents or traffic violations will typically result in higher premiums, reflecting the increased likelihood of future claims. Conversely, a clean driving record can earn you significant discounts. Similarly, your credit score often plays a significant role, with higher scores generally correlating to lower insurance rates. Insurers often use credit-based insurance scores to assess risk, although this practice varies by state and insurer. For example, a driver with a history of at-fault accidents and a poor credit score will likely face substantially higher premiums compared to a driver with a clean record and excellent credit.

Benefits and Drawbacks of Insurance Discounts

Many insurers offer discounts to incentivize safe driving and responsible behavior. Good student discounts, for example, reward students who maintain a certain GPA, recognizing their lower risk profile. Safe driver discounts are often available after a period of accident-free driving, rewarding consistent safe driving habits. However, these discounts often come with conditions. For instance, a good student discount might require proof of enrollment and academic standing. Safe driver discounts may be contingent upon maintaining a clean driving record for a specified duration. While these discounts can significantly reduce premiums, it’s crucial to understand the eligibility criteria and maintain the requirements to keep the discount.

Questions to Ask Insurance Providers When Comparing Quotes

Before committing to an insurance policy, it’s essential to thoroughly compare quotes and understand the coverage offered. This involves asking specific questions to ensure you’re making an informed decision. Specifically, inquire about the specifics of their liability coverage, uninsured/underinsured motorist coverage, collision and comprehensive coverage, and the availability of roadside assistance. It is also important to ask about the deductible amounts and what they cover, along with the availability of any discounts and the process for filing a claim. Finally, clarify the payment options and whether there are any additional fees or charges. By asking these clarifying questions, you can compare apples to apples and ensure you choose a policy that aligns with your budget and risk tolerance.

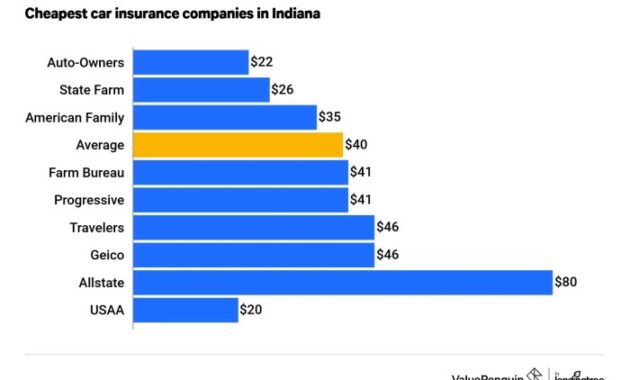

Types of Cheap Auto Insurance Providers

Finding the right auto insurance provider in Indiana can significantly impact your budget. Understanding the different types of insurers available, and their respective strengths and weaknesses, is crucial for securing affordable coverage without sacrificing essential protection. This section will explore the key categories of auto insurance providers in Indiana, highlighting their comparative advantages and disadvantages.

Major Types of Auto Insurance Providers in Indiana

Indiana’s auto insurance market is diverse, offering a range of providers to suit various needs and preferences. Three primary categories stand out: large national companies, regional insurers, and online providers. Each offers a unique combination of pricing, service, and coverage options.

- Large National Companies: These insurers, with extensive nationwide operations, often boast significant brand recognition and a wide network of agents and claims adjusters. Their established infrastructure generally ensures reliable service, but their broad reach can sometimes translate to less personalized service and potentially higher premiums compared to regional competitors. Examples include State Farm, Progressive, and Allstate.

- Regional Insurers: Focusing on specific geographic areas, such as Indiana or the surrounding states, regional insurers often offer a more personalized approach and potentially lower premiums. Their smaller scale might mean fewer agents and a less extensive network, but they frequently prioritize customer relationships and community involvement, fostering strong local ties. Examples of regional insurers that may offer competitive rates in Indiana (specific availability varies) would need further research of companies operating in Indiana and their current pricing models.

- Online Providers: These digital-first companies operate exclusively or primarily online, often leveraging technology to streamline processes and offer competitive pricing. Their efficiency can lead to lower overhead costs, translating into lower premiums for consumers. However, the lack of a physical office or local agent might limit in-person service options and necessitate reliance on digital communication channels. Examples include companies like Geico and others offering direct-to-consumer policies.

Comparison of Provider Types

The best choice among these provider types depends heavily on individual needs and priorities. While online providers might offer the lowest initial premiums, the lack of a local agent could be a drawback for those preferring in-person assistance. Conversely, large national companies offer widespread accessibility but may not always provide the most competitive pricing. Regional insurers attempt to balance these aspects, offering a potentially personalized experience with competitive rates.

- Example Comparison (Illustrative): Let’s compare three hypothetical Indiana-based providers. Provider A (Large National Company) might offer comprehensive coverage with a wide agent network but at a higher premium (e.g., $120/month). Provider B (Regional Insurer) might offer similar coverage with more personalized service for a slightly lower premium (e.g., $100/month). Provider C (Online Provider) might have a lower premium (e.g., $90/month) but offer limited in-person support. These are illustrative figures and actual premiums will vary widely based on individual factors.

Tips for Saving Money on Auto Insurance

Securing affordable auto insurance in Indiana requires a proactive approach. By understanding your options and implementing smart strategies, you can significantly reduce your premiums without compromising coverage. This section details effective methods for lowering your insurance costs.

Negotiating Lower Insurance Premiums

Negotiating your insurance premium can be surprisingly effective. Start by reviewing your policy and identifying areas where you might be overpaying. For example, if you’ve improved your driving record or added safety features to your car, these are strong points to bring up during a negotiation. Contact your insurer directly and politely explain your situation, highlighting these positive changes. Be prepared to discuss other offers you’ve received from competitors; this can incentivize them to match or beat a lower price. Remember to be respectful and professional throughout the process. A friendly and informed approach often yields the best results.

Improving Driving Habits to Reduce Risk and Costs

Safe driving habits directly impact your insurance premiums. Insurance companies reward drivers with clean records. Maintaining a spotless driving record by avoiding accidents and traffic violations is paramount. Furthermore, consider taking a defensive driving course; many insurers offer discounts for completing such courses. These courses often provide valuable insights into safe driving techniques, which can lead to fewer accidents and lower premiums. Regular vehicle maintenance is another factor; well-maintained vehicles are less likely to be involved in accidents due to mechanical failure.

Bundling Insurance Policies to Save Money

Bundling your auto insurance with other insurance policies, such as homeowners or renters insurance, often results in significant savings. Many insurance companies offer discounts for bundling multiple policies under one provider. This is because it simplifies administration for the insurer and reduces their overall risk. By bundling your policies, you consolidate your payments and benefit from a reduced overall cost. Compare quotes from different insurers offering bundling options to find the best deal. Be sure to carefully review the terms and conditions of each bundled policy to ensure you are receiving adequate coverage.

Comparing Quotes from Multiple Insurers Effectively

Comparing quotes from multiple insurers is crucial for finding the best price. Use online comparison tools to quickly obtain quotes from various companies. However, remember that these tools often present only basic coverage options. It’s essential to contact insurers directly to discuss your specific needs and obtain personalized quotes. When comparing quotes, pay close attention to the coverage details, deductibles, and any additional fees or surcharges. Don’t solely focus on the price; ensure the coverage adequately protects you and your vehicle. Consider factors such as customer service ratings and claims handling processes when making your final decision.

Ultimate Conclusion

Ultimately, finding cheap auto insurance in Indiana involves a proactive approach. By carefully comparing quotes, understanding the factors that influence premiums, and employing smart strategies, drivers can significantly reduce their costs while ensuring adequate coverage. Remember that the cheapest policy isn’t always the best; prioritizing a balance between affordability and comprehensive protection is crucial for peace of mind on the road.

Essential Questionnaire

What is the minimum auto insurance coverage required in Indiana?

Indiana requires minimum liability coverage of $25,000 per person and $50,000 per accident for bodily injury, and $25,000 for property damage.

How does my credit score affect my auto insurance rates?

In Indiana, insurers can consider your credit score when determining your rates. A good credit score typically leads to lower premiums.

Can I bundle my auto and homeowners insurance for discounts?

Yes, many insurance companies offer discounts for bundling auto and homeowners (or renters) insurance policies.

What is SR-22 insurance and do I need it?

SR-22 insurance is proof of liability coverage required by the state after certain driving offenses. You’ll only need it if mandated by the court or BMV.