Securing the right auto insurance in Wisconsin is crucial, not just for legal compliance but for financial protection in the event of an accident. This guide delves into the intricacies of Wisconsin’s auto insurance landscape, providing a clear understanding of coverage options, cost factors, and the process of finding the best policy for your needs. From understanding mandatory liability limits to exploring optional add-ons, we’ll equip you with the knowledge to make informed decisions about your auto insurance.

Wisconsin’s auto insurance market offers a range of choices, and understanding the nuances of each policy type is key to finding the right fit. This guide aims to simplify the process, clarifying the complexities of coverage, premiums, and the various factors that influence your insurance costs. We’ll also explore how to find reputable providers, compare quotes effectively, and identify potential savings through available discounts.

Wisconsin Auto Insurance Laws and Regulations

Navigating Wisconsin’s auto insurance landscape requires understanding the state’s specific laws and regulations. This information is crucial for ensuring compliance and avoiding potential penalties. This section will Artikel key aspects of Wisconsin’s auto insurance requirements, including minimum coverage, proof of insurance acquisition, penalties for non-compliance, and a comparison with neighboring states.

Minimum Liability Coverage Requirements in Wisconsin

Wisconsin mandates minimum liability coverage for bodily injury and property damage. Drivers must carry at least $25,000 in coverage for injuries to one person in an accident, $50,000 for injuries to multiple people in a single accident, and $10,000 for property damage. These are the bare minimums; purchasing higher coverage limits offers greater protection in the event of a serious accident. Failing to meet these minimums can result in significant financial and legal repercussions.

Obtaining Proof of Insurance in Wisconsin

Proof of insurance in Wisconsin is typically provided through an insurance ID card issued by your insurance company. This card must be carried in your vehicle at all times and presented upon request by law enforcement. Electronic proof of insurance is also becoming increasingly accepted, but it’s crucial to check with your insurance provider and local authorities regarding the legality and acceptance of digital proof. If you’re involved in an accident, providing proof of insurance is a critical step in the claims process.

Penalties for Driving Without Insurance in Wisconsin

Driving without insurance in Wisconsin is a serious offense. Penalties include fines, license suspension, and even vehicle impoundment. The specific penalties can vary depending on the circumstances and the number of offenses. Repeat offenders face increasingly severe consequences. Beyond the legal penalties, being uninsured leaves you personally liable for all accident-related costs, which can quickly become overwhelming.

Comparison of Wisconsin’s Auto Insurance Laws with Neighboring States

Wisconsin’s minimum liability coverage requirements are relatively standard compared to neighboring states like Minnesota, Iowa, and Illinois. However, specific regulations regarding uninsured/underinsured motorist coverage, personal injury protection (PIP), and other optional coverages can differ significantly. It’s advisable to research the laws of neighboring states if you frequently travel across state lines. For example, while Wisconsin may have similar minimum liability, another state might mandate PIP coverage, which Wisconsin doesn’t require.

Summary of Wisconsin Auto Insurance Regulations

| Regulation | Details |

|---|---|

| Minimum Liability Coverage | $25,000/$50,000/$10,000 (Bodily Injury/Property Damage) |

| Proof of Insurance | Insurance ID card or approved electronic proof |

| Penalties for Uninsured Driving | Fines, license suspension, vehicle impoundment |

| Comparison to Neighboring States | Similar minimum liability, but variations in other coverages exist. |

Types of Auto Insurance Coverage Available in Wisconsin

Choosing the right auto insurance coverage in Wisconsin is crucial for protecting yourself and your finances. Understanding the various types of coverage available will help you make informed decisions and ensure you have adequate protection. This section details the key coverages you should consider.

Liability Coverage: Bodily Injury and Property Damage

Liability coverage protects you financially if you cause an accident that injures someone or damages their property. It’s typically divided into two parts: bodily injury liability and property damage liability. Bodily injury liability covers medical bills, lost wages, and pain and suffering for individuals injured in an accident you caused. Property damage liability covers the cost of repairing or replacing damaged vehicles or other property. The amounts of coverage are expressed as limits, such as 25/50/10, meaning $25,000 per person for bodily injury, $50,000 total for bodily injury per accident, and $10,000 for property damage. Wisconsin requires minimum liability coverage, but higher limits are strongly recommended to protect against significant financial losses.

Uninsured/Underinsured Motorist Coverage

This coverage protects you if you’re involved in an accident caused by an uninsured or underinsured driver. Uninsured motorist coverage compensates you for your injuries and vehicle damage, while underinsured motorist coverage covers the difference between the other driver’s liability limits and your actual losses. Given the prevalence of uninsured drivers, this coverage offers essential protection against significant out-of-pocket expenses. For example, if an uninsured driver causes an accident resulting in $50,000 in medical bills, your uninsured motorist coverage would help cover those costs, up to your policy’s limits.

Collision and Comprehensive Coverage

Collision coverage pays for repairs or replacement of your vehicle if it’s damaged in an accident, regardless of fault. Comprehensive coverage covers damage to your vehicle caused by events other than collisions, such as theft, vandalism, fire, hail, or falling objects. While not legally required, these coverages provide valuable protection against unexpected vehicle damage. Imagine a hailstorm damaging your car; comprehensive coverage would take care of the repairs.

Optional Coverages: Roadside Assistance and Rental Reimbursement

Several optional coverages can enhance your auto insurance policy. Roadside assistance provides services such as towing, flat tire changes, and lockout assistance. Rental reimbursement helps cover the cost of a rental car while your vehicle is being repaired after an accident or due to a covered comprehensive claim. While these add to your premium, they offer significant convenience and peace of mind. Consider the frequency with which you might need these services when deciding if they are worthwhile additions to your policy.

Comparison of Key Coverage Features

Below is a comparison of the key features of each coverage type. Choosing the right combination depends on your individual needs and risk tolerance.

- Liability Coverage (Bodily Injury & Property Damage): Protects others involved in accidents you cause. Required by law in Wisconsin. Limits are crucial.

- Uninsured/Underinsured Motorist Coverage: Protects you if hit by an uninsured or underinsured driver. Highly recommended.

- Collision Coverage: Pays for damage to your vehicle in an accident, regardless of fault. Optional, but valuable.

- Comprehensive Coverage: Covers damage to your vehicle from non-collision events (theft, fire, etc.). Optional, but valuable.

- Roadside Assistance: Provides towing, lockout, and other roadside services. Optional.

- Rental Reimbursement: Covers rental car costs during repairs. Optional.

Factors Affecting Wisconsin Auto Insurance Premiums

Understanding the factors that influence your Wisconsin auto insurance premiums is crucial for budgeting and securing the best possible rate. Several key elements contribute to the final cost, ranging from your driving record to the type of vehicle you drive and even your location within the state. This section will delve into these factors, providing you with a clearer picture of how your premiums are determined.

Driving Record

Your driving history significantly impacts your insurance premiums. A clean record with no accidents or traffic violations will generally result in lower rates. Conversely, accidents and tickets, particularly those involving significant damage or injuries, will lead to higher premiums. The severity of the infraction and the frequency of incidents are both considered. For example, a single speeding ticket might result in a modest increase, while a DUI or multiple accidents could dramatically raise your rates. Insurance companies view a history of at-fault accidents as a higher risk, justifying increased premiums to cover potential future claims.

Age and Driving Experience

Age is a significant factor in determining insurance rates. Younger drivers, particularly those under 25, typically pay higher premiums due to statistically higher accident rates in this age group. As drivers gain experience and reach a certain age (usually around 25), their premiums tend to decrease. This reflects the reduced risk associated with more experienced drivers. Conversely, older drivers might see slightly higher premiums due to potential health concerns affecting driving ability, although this is often less impactful than the younger driver surcharge.

Vehicle Type

The type of vehicle you insure also plays a crucial role in determining your premiums. The make, model, and year of your car influence its insurance cost. Sports cars and high-performance vehicles generally command higher premiums due to their higher repair costs and increased risk of accidents. Conversely, smaller, less expensive vehicles often have lower premiums. Features like anti-theft devices can also influence rates, potentially leading to discounts. For example, a new, high-performance SUV will likely have a higher premium than an older, smaller sedan.

Location

Your location within Wisconsin influences your insurance rates. Areas with higher rates of accidents and theft tend to have higher premiums. This is because insurance companies assess the risk associated with specific geographic locations. Urban areas often have higher premiums than rural areas due to increased traffic congestion and higher crime rates. The specific zip code used in your address is a significant factor in calculating premiums. For example, someone living in Milwaukee might pay more than someone in a smaller, less populated town.

Credit Score

In Wisconsin, credit-based insurance scores are used by many insurers to assess risk. A good credit score generally translates to lower premiums, while a poor credit score can result in higher premiums. This is based on the statistical correlation between credit history and insurance claims. While this practice is controversial, it’s legal in Wisconsin, and many companies use it as one factor among many in determining your rate. The exact impact varies by insurer but can significantly influence the overall cost.

Table of Factors Affecting Wisconsin Auto Insurance Premiums

| Factor | Relative Importance | Impact on Premiums | Example |

|---|---|---|---|

| Driving Record | High | Higher premiums for accidents and violations | Multiple accidents lead to significantly higher premiums |

| Age | High | Younger drivers generally pay more | Drivers under 25 typically face higher rates |

| Vehicle Type | Medium | More expensive vehicles cost more to insure | A sports car is more expensive to insure than a sedan |

| Location | Medium | Higher risk areas have higher premiums | Milwaukee residents might pay more than rural residents |

| Credit Score | Medium | Good credit leads to lower premiums | A high credit score can result in significant savings |

Finding and Choosing an Auto Insurance Provider in Wisconsin

Securing the right auto insurance in Wisconsin involves careful consideration of various factors. Choosing the right provider can significantly impact your premiums and the level of coverage you receive. Understanding the process and available options is key to making an informed decision.

Reputable Auto Insurance Companies in Wisconsin

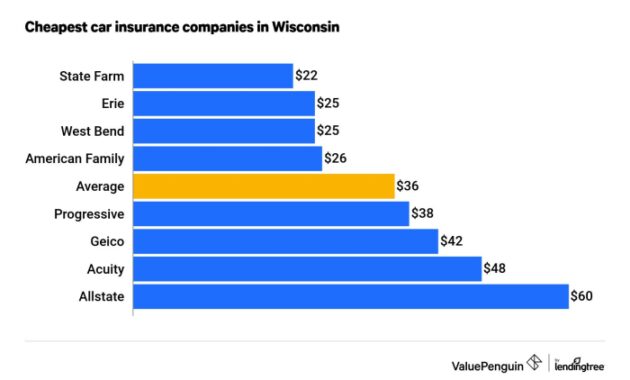

Many reputable insurance companies operate within Wisconsin, offering a range of coverage options to suit diverse needs and budgets. Selecting a company with a strong financial rating and positive customer reviews is crucial for ensuring reliable service and claims processing. Some examples of companies with a significant presence in Wisconsin include State Farm, American Family Insurance, Geico, Progressive, and Farmers Insurance. It’s important to remember that this is not an exhaustive list, and the best provider for you will depend on your individual circumstances.

Comparing Auto Insurance Quotes

Comparing quotes from multiple insurers is a vital step in finding the most cost-effective policy that meets your requirements. This involves obtaining quotes from at least three to five different companies. Pay close attention to the coverage details included in each quote, not just the price. Consider factors such as deductibles, coverage limits, and any additional features offered. Online comparison tools can streamline this process, allowing you to input your information once and receive multiple quotes simultaneously. Remember to be consistent with the information you provide to each company for accurate comparisons.

Importance of Carefully Reading Policy Details

Before committing to an auto insurance policy, meticulously review all policy documents. Understanding the specific terms, conditions, exclusions, and coverage limits is paramount. Pay particular attention to the definitions of covered events, the claims process, and any potential limitations on coverage. Don’t hesitate to contact the insurer directly if any aspect of the policy is unclear. Failing to understand your policy can lead to unexpected costs or coverage gaps in the event of an accident.

Filing an Auto Insurance Claim

Filing a claim typically involves reporting the incident to your insurer as soon as possible. This often includes providing details of the accident, including date, time, location, and the involved parties. You might be required to provide police reports, witness statements, and photographic evidence. Your insurer will guide you through the necessary steps, including assessments, repairs, and potential settlements. Prompt and accurate reporting is crucial for a smooth claims process. Be prepared to provide all relevant documentation as requested.

Step-by-Step Guide to Obtaining Auto Insurance in Wisconsin

Obtaining auto insurance in Wisconsin follows a straightforward process. First, gather necessary information such as your driver’s license, vehicle information (year, make, model), and driving history. Next, obtain quotes from multiple insurers using online comparison tools or by contacting companies directly. Carefully compare the quotes, focusing on coverage details and premiums. Once you’ve chosen a policy, complete the application process, providing all required documentation. Finally, pay your premium and receive your insurance card. Maintain accurate records of your policy and payments. Remember to notify your insurer of any changes to your driving record or vehicle information.

Discounts and Savings on Wisconsin Auto Insurance

Securing affordable auto insurance in Wisconsin is achievable through various discounts offered by insurance providers. Understanding these discounts and how to qualify for them can significantly reduce your premiums. This section details common discounts, eligibility criteria, and examples of potential savings.

Common Auto Insurance Discounts in Wisconsin

Many Wisconsin auto insurers offer a range of discounts to incentivize safe driving habits and responsible insurance practices. These discounts can substantially lower your overall premium cost.

| Discount Type | Description | Eligibility Requirements | Example Savings |

|---|---|---|---|

| Good Driver Discount | Rewards drivers with a clean driving record. | Typically requires a minimum of three years of driving history without accidents or traffic violations. Specific requirements vary by insurer. | Could save 10-20% or more depending on driving history and insurer. For instance, a driver with a spotless record for five years might save $200 annually on a $1000 premium. |

| Multi-Car Discount | Offered when insuring multiple vehicles under the same policy. | Requires insuring at least two vehicles with the same insurer. | Often provides a 10-15% discount on each vehicle insured. Insuring two cars could save $150 annually if each car’s premium is $1000. |

| Bundling Discount | Combining auto insurance with other types of insurance, such as homeowners or renters insurance. | Requires purchasing both auto and another type of insurance from the same provider. | Savings can reach 10-25% depending on the bundled policies and insurer. Bundling home and auto insurance could save $300 annually on a combined premium of $1500. |

| Defensive Driving Course Discount | Completing a state-approved defensive driving course. | Proof of course completion is usually required. | Can reduce premiums by 5-10%. A 5% discount on a $1000 premium would save $50. |

| Vehicle Safety Features Discount | For vehicles equipped with safety features like anti-theft devices, airbags, or anti-lock brakes. | Verification of safety features might be needed. | Savings vary based on the features and insurer, potentially saving 5-15%. A vehicle with advanced safety features might yield a $100 savings on a $1000 premium. |

Comparing Discount Programs Across Major Insurers

Discount programs vary considerably between major insurers in Wisconsin. For example, some insurers might offer a higher percentage discount for good drivers, while others might provide more substantial savings for bundling insurance policies. It’s crucial to compare quotes from multiple insurers to find the best deal tailored to your individual circumstances. This requires contacting each insurer directly or using online comparison tools to get personalized quotes.

Calculating Potential Savings

Calculating potential savings requires obtaining quotes from different insurers with and without the discounts you qualify for. For example:

Let’s say your initial quote without discounts is $1200 annually. If you qualify for a good driver discount (15%), a multi-car discount (10%), and a bundling discount (5%), your potential savings would be:

Good Driver Discount: $1200 x 0.15 = $180

Multi-Car Discount: $1200 x 0.10 = $120

Bundling Discount: $1200 x 0.05 = $60

Total Savings: $180 + $120 + $60 = $360

Final Premium: $1200 – $360 = $840

This example demonstrates the significant impact that multiple discounts can have on your overall insurance costs. Remember that these are illustrative examples; actual savings will depend on your specific circumstances and the insurer’s policies.

Understanding Wisconsin’s No-Fault System

Wisconsin is a no-fault insurance state, meaning that after a car accident, each driver’s insurance company pays for their own medical bills and lost wages, regardless of who caused the accident. This system aims to expedite the claims process and reduce litigation. However, it has limitations and exceptions.

The No-Fault Claims Process

Filing a no-fault claim typically involves contacting your insurance company as soon as possible after the accident. You’ll need to provide information about the accident, your injuries, and any lost wages. Your insurer will then investigate the claim and begin processing payments for your covered expenses. Documentation, such as medical bills and proof of lost income, is crucial for a smooth claim process. Failure to promptly notify your insurer could jeopardize your claim.

Limitations of No-Fault Coverage

Wisconsin’s no-fault system doesn’t cover all damages. While it covers medical expenses and lost wages, it generally doesn’t cover pain and suffering unless your injuries meet a specific threshold, such as a significant permanent injury or death. This threshold is often high, meaning that many individuals injured in accidents do not receive compensation for pain and suffering under the no-fault system. Property damage is also typically not covered under no-fault; it’s handled separately through liability coverage.

Comparison with Other Systems

In contrast to no-fault systems, some states operate under a tort system, where individuals can sue the at-fault driver to recover damages, including pain and suffering, regardless of the severity of their injuries. This can lead to more litigation but potentially broader coverage. Other states utilize a hybrid system, combining aspects of both no-fault and tort systems. Wisconsin’s system prioritizes quicker payment for medical bills and lost wages but restricts compensation for pain and suffering unless significant injuries are involved.

Examples of No-Fault Applicability

Imagine a scenario where two cars collide at an intersection. Both drivers are injured. Under Wisconsin’s no-fault system, each driver’s insurance company would pay for their own medical bills and lost wages, even if one driver was clearly at fault. Another example would be a single-car accident where the driver sustains injuries. Their insurance would cover their medical bills and lost wages, regardless of the cause of the accident (e.g., a pothole, icy road). However, if one driver sustains significant, permanent injuries, they might be able to pursue a lawsuit against the at-fault driver to recover for pain and suffering beyond their no-fault coverage.

Last Point

Successfully navigating the world of Wisconsin auto insurance requires careful planning and informed decision-making. By understanding the state’s regulations, available coverage options, and the factors influencing premiums, you can secure a policy that provides adequate protection while fitting within your budget. Remember to compare quotes, read policy details thoroughly, and take advantage of any available discounts to optimize your coverage and savings. Driving safely and maintaining a clean driving record are also crucial steps in keeping your insurance costs manageable.

Top FAQs

What happens if I’m in an accident and don’t have insurance?

Driving without insurance in Wisconsin is illegal and results in significant penalties, including fines, license suspension, and potential vehicle impoundment. You’ll also be responsible for all accident-related costs.

How often can I expect my insurance rates to change?

Insurance rates can change annually, or even more frequently, depending on your driving record, claims history, and changes in risk assessment by the insurance company.

Can I get insurance if I have a poor driving record?

Yes, but it will likely be more expensive. Many insurers offer coverage to high-risk drivers, though you might find fewer options and higher premiums.

What is SR-22 insurance?

SR-22 insurance is proof of financial responsibility required by the state after certain driving offenses (like DUI). It’s a certificate filed with the state showing you maintain the minimum required liability insurance.