Securing adequate insurance for your car and home is a crucial aspect of responsible financial planning. This guide delves into the complexities of finding the best car and homeowners insurance, exploring various policy options, factors influencing premiums, and strategies for saving money. We’ll navigate the often-confusing world of insurance jargon, empowering you to make informed decisions that protect your assets and provide peace of mind.

From understanding bundled packages and the impact of your credit score to comparing different insurance providers and filing claims effectively, we’ll cover all the essential elements to help you navigate the insurance landscape confidently. We’ll also provide practical tips and actionable advice to help you secure the best possible coverage at the most competitive price.

Bundled Insurance Packages

Bundling your car and homeowners insurance is a popular strategy that can lead to significant savings and simplified insurance management. This approach combines both your auto and home insurance policies under a single provider, often resulting in lower premiums than purchasing separate policies from different companies. Let’s explore the advantages and disadvantages of this approach.

Bundling your car and homeowners insurance offers several key advantages. Primarily, it often results in lower overall premiums. Insurance companies incentivize bundling by offering discounts to customers who consolidate their policies. This is because managing a single customer’s multiple policies is more efficient than handling separate policies from different individuals. Furthermore, bundling simplifies the insurance process. You have a single point of contact for all your insurance needs, making it easier to manage claims, payments, and policy updates. This streamlined approach can save time and reduce administrative hassle.

Comparison of Bundled and Separate Policies

Purchasing separate policies offers flexibility. You can choose different insurers for each policy, potentially finding the best coverage and price for each individually. However, this approach requires managing multiple policies, payments, and potentially dealing with different claims processes. Bundling, while potentially limiting your choice of insurer, provides the convenience of a single provider and the financial benefit of bundled discounts.

Common Discounts for Bundled Insurance

Many insurance providers offer a variety of discounts for bundling car and homeowners insurance. Common discounts include multi-policy discounts (the most common), good driver discounts (if you have a clean driving record), home security discounts (if you have a security system), and loyalty discounts (for long-term customers). The specific discounts available vary depending on the insurer and your individual circumstances. For example, a company might offer a 10% discount for bundling, an additional 5% for a good driving record, and another 5% for having a home security system, resulting in a substantial overall savings.

Example Bundled Insurance Packages

| Package | Price (Annual) | Car Coverage | Home Coverage |

|---|---|---|---|

| Basic Bundle | $1200 | $25,000 liability, $5,000 collision | $100,000 dwelling, $20,000 personal property |

| Standard Bundle | $1500 | $50,000 liability, $10,000 collision, Uninsured/Underinsured Motorist Coverage | $200,000 dwelling, $40,000 personal property, $10,000 liability |

| Premium Bundle | $1800 | $100,000 liability, $20,000 collision, Uninsured/Underinsured Motorist Coverage, Rental Car Reimbursement | $300,000 dwelling, $60,000 personal property, $20,000 liability, Replacement Cost Coverage |

Factors Affecting Insurance Premiums

Understanding the factors that influence your insurance premiums is crucial for securing the best coverage at a reasonable price. Several key elements contribute to the final cost of both car and homeowners insurance, and being aware of these can help you make informed decisions to potentially lower your premiums.

Driving History’s Impact on Car Insurance Premiums

Your driving record significantly impacts your car insurance premium. Insurance companies assess risk based on your history of accidents, traffic violations, and claims. A clean driving record, characterized by no accidents or tickets, typically results in lower premiums. Conversely, multiple accidents or serious violations, such as driving under the influence (DUI), will significantly increase your premiums. The severity and frequency of incidents are weighted differently; a single minor accident might have a less dramatic impact than multiple speeding tickets or a DUI conviction. Many insurers utilize a points system, where each incident adds points to your record, directly correlating to higher premiums. For example, a driver with three speeding tickets in a year might see a 20-30% increase in their premium compared to a driver with a clean record.

Credit Score’s Influence on Car and Homeowners Insurance Rates

Surprisingly, your credit score plays a significant role in determining both your car and homeowners insurance rates. Insurers often use credit-based insurance scores (CBIS) as an indicator of risk. A higher credit score generally correlates with a lower risk profile, resulting in lower premiums. The reasoning behind this is that individuals with good credit history tend to demonstrate responsible financial behavior, which is seen as a predictor of responsible behavior in other areas, including driving and home maintenance. Conversely, a lower credit score may indicate a higher risk of claims, leading to higher premiums. The impact can be substantial; a poor credit score could result in premiums 20-40% higher than for someone with excellent credit, depending on the insurer and the specific circumstances.

Home Location and Features Impact on Homeowners Insurance Costs

The location of your home and its features significantly influence homeowners insurance premiums. Homes in areas prone to natural disasters, such as hurricanes, earthquakes, or wildfires, will generally command higher premiums due to the increased risk of damage. Proximity to fire hydrants, the quality of local fire services, and the presence of security systems all factor into the assessment of risk. A home equipped with advanced security systems, such as alarm systems and fire suppression systems, may qualify for discounts. Similarly, a home located in a neighborhood with a low crime rate and close proximity to a well-equipped fire department will likely receive lower premiums compared to a home in a high-risk area. For instance, a home in a flood zone might see a premium increase of 50% or more compared to a similar home in a non-flood zone.

Five Factors to Lower Insurance Premiums

Several actions can significantly lower your insurance premiums for both car and home.

- Maintain a clean driving record: Avoid accidents and traffic violations.

- Improve your credit score: Pay bills on time and manage your debt effectively.

- Install security systems: Burglar alarms and fire suppression systems can reduce premiums.

- Bundle your insurance: Combine car and homeowners insurance with the same provider for potential discounts.

- Increase your deductible: Choosing a higher deductible can lower your premiums (though it means a higher out-of-pocket cost if you need to file a claim).

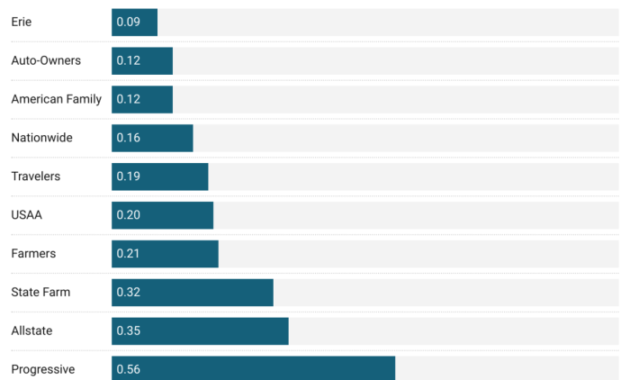

Choosing the Right Insurance Provider

Selecting the right insurance provider is a crucial decision impacting your financial well-being. A comprehensive understanding of different providers, their customer service, and claim processing procedures is essential for making an informed choice that best suits your individual needs and preferences. This section will compare three major insurance providers, highlighting key aspects to consider.

Comparison of Three Major Insurance Providers

Choosing an insurance provider involves more than just comparing premiums. Customer service and efficient claim processing are equally vital. Below, we compare three hypothetical major providers – InsureSafe, CoverAll, and SecureFirst – to illustrate the importance of thorough research. Note that the data presented here is for illustrative purposes and should not be considered definitive financial advice. Always consult the providers directly for the most up-to-date information.

| Provider | Customer Service Rating (Hypothetical) | Claim Processing Speed (Hypothetical, in days) | Average Annual Premium (Hypothetical) |

|---|---|---|---|

| InsureSafe | 4.5 out of 5 stars | 7-10 | $1200 |

| CoverAll | 4.0 out of 5 stars | 10-14 | $1100 |

| SecureFirst | 3.8 out of 5 stars | 15-21 | $1000 |

The Importance of Customer Reviews and Policy Detail Comparison

Before committing to an insurance provider, thoroughly examining customer reviews and meticulously comparing policy details is paramount. Online platforms like Yelp, Google Reviews, and dedicated insurance review sites offer valuable insights into the experiences of other policyholders. These reviews often highlight aspects such as responsiveness of customer service representatives, ease of filing claims, and the overall fairness of claim settlements. Furthermore, a careful side-by-side comparison of policy documents ensures you understand coverage limits, deductibles, exclusions, and other crucial terms and conditions. Discrepancies in seemingly minor details can significantly affect your financial liability in case of an incident. For example, one provider might offer broader coverage for specific types of damage or have more flexible payment options. Ignoring these details can lead to unexpected costs and dissatisfaction.

Saving Money on Insurance

Saving money on your car and homeowners insurance is achievable with a strategic approach. By understanding the factors that influence your premiums and implementing some simple changes, you can significantly reduce your annual costs without compromising your coverage. This section Artikels effective strategies for both car and homeowners insurance.

Strategies for Reducing Car Insurance Premiums

Several factors influence your car insurance premium. Understanding these allows for targeted cost-saving measures. These range from driving habits to the type of vehicle you insure.

- Maintain a Clean Driving Record: Accidents and traffic violations significantly increase premiums. Defensive driving and adherence to traffic laws are crucial. For example, a single speeding ticket can lead to a 10-20% increase in premiums depending on the insurer and severity of the violation.

- Bundle Your Insurance: Many insurers offer discounts for bundling car and homeowners insurance. This can result in substantial savings compared to purchasing separate policies.

- Choose a Higher Deductible: Opting for a higher deductible reduces your monthly premium, as you agree to pay more out-of-pocket in the event of a claim. However, carefully assess your financial situation to ensure you can comfortably afford the higher deductible.

- Shop Around and Compare Quotes: Different insurers offer varying rates. Comparing quotes from multiple companies ensures you secure the best possible price for your coverage.

- Consider Your Vehicle Choice: The make, model, and safety features of your car influence premiums. Safer vehicles with lower theft rates often attract lower insurance costs. For instance, a smaller, fuel-efficient car will typically have a lower premium than a high-performance sports car.

- Improve Your Credit Score: In many states, your credit score is a factor in determining your insurance premium. Improving your credit score can lead to lower rates.

- Take Advantage of Discounts: Many insurers offer discounts for things like good student status, completing a defensive driving course, or having anti-theft devices installed in your vehicle. Inquire about available discounts with your insurer.

Methods for Lowering Homeowners Insurance Costs

Similar to car insurance, several factors impact your homeowners insurance premiums. Taking proactive steps can lead to significant savings.

- Improve Your Home’s Security: Installing security systems, including alarms and deadbolt locks, can reduce your premiums. These measures demonstrate a lower risk to the insurer.

- Upgrade Your Home’s Safety Features: Installing smoke detectors, fire sprinklers, and updated electrical systems can lower your premiums by demonstrating a reduced risk of fire or other damage.

- Maintain Your Property: Regular maintenance, including roof repairs and landscaping, shows the insurer that you are proactive in protecting your property. Neglecting maintenance can lead to higher premiums.

- Increase Your Deductible: Similar to car insurance, increasing your deductible on your homeowners policy can lower your premiums. This requires careful consideration of your financial capacity to cover a larger out-of-pocket expense in the event of a claim.

- Shop Around for the Best Rates: Just as with car insurance, comparing quotes from different insurers is crucial for finding the best homeowners insurance rate.

Benefits of Increasing Deductibles to Lower Premiums

Increasing your deductible, both for car and homeowners insurance, is a common strategy to reduce premiums. This involves agreeing to pay a higher amount out-of-pocket in the event of a claim. The trade-off is a lower monthly premium.

The benefit is a lower monthly or annual premium. However, it’s crucial to assess your financial capacity to comfortably afford the higher deductible in case of a claim. A realistic assessment of your financial situation is paramount before making this decision.

Final Wrap-Up

Ultimately, securing the best car and homeowners insurance involves a careful assessment of your individual needs and risk profile. By understanding the factors that influence premiums, comparing different policy options, and selecting a reputable insurance provider, you can create a comprehensive insurance plan that safeguards your valuable possessions and provides financial security. Remember to regularly review your policies and make adjustments as needed to ensure you maintain optimal coverage throughout life’s changes.

Key Questions Answered

What is the difference between liability and collision coverage for car insurance?

Liability coverage pays for damages to other people’s property or injuries sustained by others in an accident you caused. Collision coverage pays for repairs to your vehicle regardless of fault.

How often should I review my insurance policies?

It’s recommended to review your policies at least annually, or whenever there’s a significant life change (e.g., marriage, new home, new car).

Can I get homeowners insurance if I have a poor credit score?

Yes, but a poor credit score will likely result in higher premiums. Some insurers specialize in high-risk individuals, though you may pay more.

What is an umbrella insurance policy?

Umbrella insurance provides additional liability coverage beyond the limits of your car and homeowners insurance policies, offering greater protection against significant lawsuits.