Securing adequate insurance for your home and vehicle is a crucial aspect of financial responsibility. Navigating the complexities of insurance policies, however, can be daunting. This guide aims to demystify the process, providing a clear understanding of the various coverages, comparison methods, and factors influencing premium costs, ultimately helping you find the best auto and home insurance to suit your individual needs.

From understanding the nuances of liability and collision coverage to comparing different insurers and policy options, we’ll explore the key elements you need to consider. We will delve into the often-overlooked aspects of claims processes and customer service, ensuring you’re fully equipped to make informed decisions about protecting your most valuable assets.

Defining “Best” in Auto and Home Insurance

Finding the “best” auto and home insurance isn’t about a single, universally applicable policy. Instead, it’s a highly personalized search driven by individual needs and priorities. The ideal policy for one person might be entirely unsuitable for another, highlighting the importance of careful consideration and comparison.

Consumers weigh numerous factors when determining which insurance provider offers the “best” coverage. Price is often a primary concern, but it shouldn’t overshadow the importance of adequate coverage limits, reputable claims handling processes, and financial strength of the insurer. A lower premium might seem attractive initially, but insufficient coverage in the event of an accident or disaster could prove far more costly in the long run.

Factors Influencing the Choice of “Best” Insurance

The definition of “best” insurance is deeply personal and depends on a variety of interconnected factors. Consumers typically prioritize a combination of affordability, comprehensive coverage, and reliable customer service. However, the relative importance of each factor varies considerably depending on individual circumstances.

- Price: The monthly or annual premium is a significant consideration for most people. However, it’s crucial to compare coverage levels, not just prices, to ensure you’re getting adequate protection for your assets.

- Coverage Limits: This refers to the maximum amount the insurer will pay for covered losses. Higher limits offer greater protection but usually come with higher premiums. Choosing the right limits requires careful assessment of your assets and potential liabilities.

- Deductibles: The amount you pay out-of-pocket before your insurance coverage kicks in. Higher deductibles generally lead to lower premiums, but you’ll bear more of the cost in the event of a claim.

- Customer Service: A positive experience with claims handling and customer support is invaluable. Look for companies known for their responsiveness and efficiency in resolving issues.

- Financial Stability: It’s essential to choose an insurer with a strong financial rating, ensuring they can meet their obligations in the event of a large-scale claim.

Insurance Rating Methodologies Comparison

Several organizations rate insurance companies based on various factors, offering consumers valuable insights into their financial stability and customer satisfaction. Comparing ratings from different sources provides a more comprehensive picture.

| Rating Agency | Focus | Methodology | Strengths |

|---|---|---|---|

| J.D. Power | Customer Satisfaction | Surveys and data analysis focusing on customer experiences with claims, billing, and overall service. | Provides insights into customer service quality and ease of doing business. |

| AM Best | Financial Strength | Comprehensive financial analysis of insurers’ balance sheets, underwriting performance, and overall risk profile. | Offers a reliable assessment of an insurer’s ability to pay claims. |

| Moody’s | Financial Strength | Similar to AM Best, focusing on financial stability and creditworthiness. | Provides an independent perspective on insurer financial health. |

| Standard & Poor’s | Financial Strength | Another credit rating agency that assesses the financial strength and creditworthiness of insurance companies. | Offers a different perspective on insurer financial health, providing a broader view. |

Influence of Personal Circumstances on Insurance Needs

Individual circumstances significantly impact insurance needs and the definition of “best” coverage. Factors such as age, location, driving history, and home value all play a crucial role in determining appropriate coverage and premiums.

- Age: Younger drivers typically pay higher premiums due to statistically higher accident rates. Older drivers might benefit from discounts or specialized policies catering to their needs.

- Location: Insurance rates vary significantly based on location, reflecting factors like crime rates, accident frequency, and the cost of repairs. Living in a high-risk area generally translates to higher premiums.

- Driving History: A clean driving record usually results in lower premiums, while accidents or traffic violations can significantly increase costs. Insurance companies use this data to assess risk.

- Home Value: For homeowners insurance, the value of your property directly impacts the premium. Higher-value homes require more extensive coverage and thus higher premiums.

Types of Auto Insurance Coverage

Choosing the right auto insurance coverage can feel overwhelming, but understanding the different types available is crucial for protecting yourself and your vehicle. This section will Artikel common coverages, compare coverage levels, and provide scenarios where each type proves beneficial. Remember, the best coverage for you depends on your individual needs and risk tolerance.

Understanding the various types of auto insurance coverage is essential for responsible vehicle ownership. Different policies offer varying degrees of protection, ranging from minimum state requirements to comprehensive coverage that safeguards against a wider array of potential incidents. The following sections will clarify the distinctions between these options and their practical implications.

Liability Coverage

Liability coverage protects you financially if you cause an accident that injures someone or damages their property. It covers the costs of medical bills, lost wages, and property repairs for the other party involved. Liability coverage is typically divided into bodily injury liability and property damage liability. Bodily injury liability covers injuries to others, while property damage liability covers damage to their vehicle or other property. State minimums for liability coverage vary significantly, and opting for higher limits is often advisable to protect yourself from potentially catastrophic financial losses.

- Scenario: You rear-end another car, causing injuries and significant damage. Liability coverage pays for the other driver’s medical bills and vehicle repairs.

- Scenario: You accidentally hit a parked car, causing damage to the vehicle. Property damage liability coverage covers the cost of repairs.

Collision Coverage

Collision coverage pays for repairs to your vehicle if it’s damaged in an accident, regardless of who is at fault. This means that even if you cause the accident, your insurance will help cover the cost of repairing or replacing your vehicle. This is particularly important if you have a newer car or a loan on your vehicle.

- Scenario: You are involved in a collision and your car sustains significant damage. Collision coverage pays for repairs or replacement, even if you are at fault.

Comprehensive Coverage

Comprehensive coverage protects your vehicle from damage caused by events other than collisions, such as theft, vandalism, fire, hail, or natural disasters. It provides broader protection than collision coverage, covering a wider range of potential risks.

- Scenario: Your car is stolen. Comprehensive coverage will reimburse you for the value of your vehicle.

- Scenario: A tree falls on your car during a storm. Comprehensive coverage will pay for the repairs.

- Scenario: Your car is damaged by hail. Comprehensive coverage will cover the cost of repairs.

Uninsured/Underinsured Motorist Coverage

Uninsured/underinsured motorist coverage protects you if you’re involved in an accident with a driver who is uninsured or underinsured. This coverage can help pay for your medical bills, lost wages, and vehicle repairs, even if the other driver is at fault and lacks sufficient insurance.

- Scenario: You are hit by an uninsured driver who causes significant injuries and property damage. This coverage helps cover your medical bills and vehicle repairs.

Minimum vs. Full Coverage

Minimum coverage refers to the minimum amounts of liability insurance required by your state. Full coverage typically includes liability, collision, and comprehensive coverage, providing more comprehensive protection. While minimum coverage is legally sufficient, it may leave you financially vulnerable in the event of a serious accident. Full coverage offers greater peace of mind but comes with higher premiums. The decision of which to choose depends on your individual circumstances, financial situation, and risk tolerance. For example, if you have a newer car with a loan, full coverage is often recommended.

Types of Home Insurance Coverage

Protecting your home is a significant financial undertaking, and understanding your home insurance policy is crucial. A comprehensive policy typically includes several key coverage areas designed to safeguard your property and your financial well-being in the event of unforeseen circumstances. This section details the common types of coverage found in most homeowners’ insurance policies.

Dwelling Coverage

This is the most fundamental part of your home insurance. Dwelling coverage protects the physical structure of your house, including attached structures like garages and porches, against damage from covered perils. Covered perils typically include fire, windstorms, hail, and vandalism, but the specific perils covered can vary depending on your policy and location. The amount of dwelling coverage you purchase should reflect the current replacement cost of your home, not its market value. This ensures you have enough money to rebuild your home if it’s completely destroyed.

Liability Coverage

Liability coverage protects you financially if someone is injured on your property or if you accidentally damage someone else’s property. This coverage pays for medical bills, legal fees, and any judgments awarded against you. For example, if a guest slips and falls on your icy walkway and sustains injuries, your liability coverage would help cover their medical expenses and legal costs. The amount of liability coverage you carry should be substantial, considering the potential costs associated with significant injuries or property damage.

Personal Property Coverage

This coverage protects your belongings inside your home, such as furniture, clothing, electronics, and jewelry. It also often extends to personal property outside your home, such as a shed or patio furniture. Personal property coverage typically pays for the actual cash value (ACV) or replacement cost of your belongings, depending on your policy. It’s important to accurately assess the value of your possessions and consider purchasing additional coverage if necessary, especially for high-value items like jewelry or electronics. Consider creating a home inventory with photos or videos as proof of ownership and value.

Other Structures Coverage

This section of your policy covers structures on your property that are not attached to your main dwelling, such as a detached garage, shed, or fence. Similar to dwelling coverage, it typically covers damage from covered perils. The amount of coverage should reflect the replacement cost of these structures.

Loss of Use Coverage

This coverage helps cover additional living expenses if your home becomes uninhabitable due to a covered loss. For instance, if a fire damages your home, this coverage can help pay for temporary housing, meals, and other necessary expenses while your home is being repaired or rebuilt.

Actual Cash Value (ACV) vs. Replacement Cost Coverage

Many homeowners insurance policies offer a choice between actual cash value (ACV) and replacement cost coverage for personal property and dwelling coverage. ACV coverage pays for the current market value of your damaged property, minus depreciation. Replacement cost coverage, on the other hand, pays for the cost to replace your damaged property with new, similar items, without deducting for depreciation. For example, if your ten-year-old sofa is damaged, ACV would only compensate you for its current value, while replacement cost would cover the cost of a new sofa. While replacement cost is more expensive, it offers better protection against inflation and the rising cost of goods.

Policy Deductibles: Benefits and Drawbacks

The following table compares different policy deductibles and their implications:

| Deductible Amount | Premium Cost | Benefits | Drawbacks |

|---|---|---|---|

| $500 | Higher | Lower out-of-pocket expense in case of a claim. | Higher annual premium cost. |

| $1000 | Moderate | Lower premium cost than a $500 deductible. | Higher out-of-pocket expense than a $500 deductible. |

| $2500 | Lower | Lowest annual premium cost. | Significantly higher out-of-pocket expense in case of a claim. |

| $5000 | Lowest | Lowest annual premium. | Very high out-of-pocket expense if a claim is filed. May not be suitable for all homeowners. |

Finding and Comparing Insurance Quotes

Securing the best auto and home insurance involves more than just picking the first policy you see. A thorough comparison of quotes from multiple providers is crucial to finding the right balance of coverage and cost. This process allows you to identify the insurer best suited to your individual needs and budget.

Finding suitable insurance quotes involves exploring several avenues. Directly contacting insurance companies, utilizing online comparison websites, and even consulting with independent insurance agents all provide different perspectives and access to a broader range of options. Each method offers unique advantages and disadvantages that should be considered.

Methods for Obtaining Insurance Quotes

Several effective methods exist for obtaining insurance quotes. These methods offer varying levels of convenience and access to a range of insurers. Understanding the nuances of each approach helps ensure a comprehensive search.

- Online Comparison Tools: Websites such as NerdWallet, The Zebra, and others allow you to input your information once and receive quotes from multiple insurers simultaneously. This method is convenient and efficient, providing a quick overview of available options. However, it may not include every insurer in your area.

- Direct Contact with Insurers: Contacting insurance companies directly allows for personalized attention and the opportunity to ask specific questions about their policies. This approach can be time-consuming but ensures you receive detailed information tailored to your needs. Examples include contacting Geico, State Farm, or Progressive directly through their websites or phone numbers.

- Independent Insurance Agents: Independent agents represent multiple insurance companies, allowing them to compare policies across various providers. They can offer expert advice and help you navigate the complexities of insurance options. This approach saves you the time and effort of contacting multiple companies individually.

Key Factors to Consider When Comparing Quotes

Comparing insurance quotes solely on price is a mistake. Several crucial factors, beyond the premium, influence the overall value and suitability of a policy. A balanced assessment is essential.

- Coverage: Compare the types and amounts of coverage offered by each insurer. Ensure the policy adequately protects your assets and liabilities. For example, consider the liability limits for auto insurance and the dwelling coverage for home insurance. Higher limits generally mean greater protection but higher premiums.

- Price: While price is a significant factor, it shouldn’t be the sole determining factor. A lower premium might mean less coverage, potentially leaving you vulnerable in the event of a claim.

- Customer Service: Read online reviews and check ratings from organizations like the Better Business Bureau to gauge the quality of customer service. A responsive and helpful insurer can significantly ease the claims process.

- Claims Process: Research each insurer’s claims process. Look for information on how easily claims are filed, processed, and settled. A streamlined claims process can make a significant difference during a stressful time.

A Step-by-Step Guide for Effectively Comparing Insurance Quotes

A structured approach ensures a comprehensive and efficient comparison of insurance quotes. Following these steps minimizes the risk of overlooking crucial details.

- Gather Necessary Information: Collect details such as your driving history, address, vehicle information (for auto insurance), and home details (for home insurance). Accurate information ensures accurate quotes.

- Use Online Comparison Tools: Start by using online comparison tools to get a broad overview of available options and pricing. This provides a benchmark for further investigation.

- Contact Insurers Directly: Follow up by contacting insurers directly, focusing on those with quotes that initially appeal to you. This allows for clarification on specific policy details.

- Compare Coverage and Prices: Carefully compare the coverage offered by each insurer, not just the price. Consider the deductibles, limits, and exclusions of each policy.

- Review Customer Service and Claims Process Information: Research the insurer’s reputation for customer service and its claims process. This information is readily available online through reviews and ratings.

- Make a Decision: Based on your comparison, choose the policy that best balances price, coverage, and customer service.

Understanding Insurance Policies

Insurance policies, whether for auto or home, are legally binding contracts outlining the agreement between you and the insurance company. Understanding your policy is crucial to ensuring you receive the coverage you need when you need it. This section will break down key policy components and the claims process.

Policy Terms and Conditions

Insurance policies contain a variety of terms and conditions that define the scope of coverage, limitations, and responsibilities of both the insured and the insurer. These terms are often presented in legal jargon, making it essential to carefully review and understand each section. Key terms include the policy period (the dates the coverage is effective), the named insured (the individual or entity covered by the policy), the covered perils (the specific events or occurrences covered by the policy, such as fire, theft, or accidents), and exclusions (events or situations that are specifically not covered). The policy will also detail the premiums, deductibles (the amount you pay out-of-pocket before the insurance coverage begins), and limits of liability (the maximum amount the insurer will pay for a covered claim). For example, a home insurance policy might exclude flood damage unless a separate flood insurance policy is purchased. Similarly, an auto insurance policy might exclude coverage for damage caused by driving under the influence.

The Claims Process

Filing a claim is a crucial step in receiving the benefits of your insurance policy. The process generally involves reporting the incident to your insurance company as soon as possible. This usually involves a phone call to their claims department, followed by providing necessary information such as the date, time, and location of the incident, as well as details of the damages or injuries sustained. You will likely be required to file a formal claim, which often includes providing supporting documentation, such as police reports, medical bills, and repair estimates. The insurance company will then investigate the claim to verify the details and assess the extent of the damages. This investigation might involve inspections, interviews, or the review of supporting documents. Once the investigation is complete, the insurance company will determine the amount they will pay towards the claim, considering the policy terms, coverage limits, and any applicable deductibles. For instance, if you are involved in a car accident, you would report it to your insurer, provide details of the accident, and cooperate with their investigation. They will assess the damage to your vehicle and potentially the other party’s vehicle, and pay out according to your policy coverage.

Reading and Understanding Your Policy

Insurance policies can be complex legal documents, but understanding them is crucial. Start by reading the policy’s declaration page. This page summarizes key information, such as the policyholder’s name, address, policy number, coverage amounts, and premium. Then, review the policy’s sections covering specific types of coverage. Each section will describe the extent of coverage, limitations, and exclusions for that specific type of coverage. Pay close attention to definitions of key terms and exclusions. Don’t hesitate to contact your insurance agent or company representative if you have questions or need clarification on any aspect of your policy. Many companies provide policy summaries or materials in addition to the full policy document, making it easier to grasp the key features of your coverage. Remember, it’s your responsibility to understand your policy; relying solely on an agent’s verbal explanation is insufficient. A thorough review of your policy document ensures you are adequately protected and aware of your rights and responsibilities.

Ultimate Conclusion

Choosing the “best” auto and home insurance policy is a deeply personal decision, heavily influenced by your unique circumstances and risk tolerance. By carefully considering the factors discussed – coverage types, premium costs, insurer reputation, and the claims process – you can confidently select a policy that offers comprehensive protection and peace of mind. Remember to regularly review your policy to ensure it continues to meet your evolving needs.

Key Questions Answered

What is the difference between actual cash value (ACV) and replacement cost coverage for home insurance?

ACV pays for the current market value of damaged property, minus depreciation. Replacement cost coverage pays for the cost to replace the damaged item with a new one, regardless of depreciation.

How does my credit score affect my insurance premiums?

Many insurers use credit-based insurance scores to assess risk. A higher credit score generally leads to lower premiums, while a lower score can result in higher premiums.

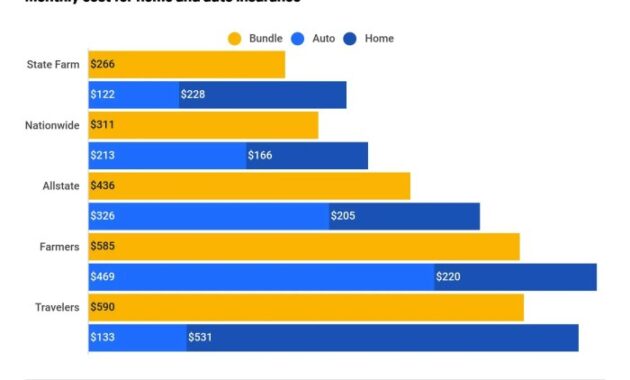

Can I bundle my auto and home insurance with different companies?

Generally, no. Bundling usually refers to purchasing both types of insurance from the same company, allowing for potential discounts.

What should I do immediately after an auto accident?

Ensure everyone is safe, call emergency services if needed, exchange information with other drivers, take photos of the damage, and contact your insurer to report the accident.