Navigating the world of car insurance can feel like driving through a dense fog. Premiums vary wildly, influenced by a complex interplay of factors ranging from your age and driving record to the make of your car and where you live. Understanding the average cost of car insurance is crucial for budgeting and making informed decisions, but the sheer number of variables involved can be overwhelming. This guide aims to illuminate the path, offering a clear and concise overview of the key elements that determine your car insurance premiums.

We’ll explore the significant factors influencing your car insurance costs, providing a detailed breakdown of how age, driving history, vehicle type, location, and coverage levels all contribute to the final price. By comparing average costs across different states, insurance companies, and driving habits, we’ll empower you to make more informed choices and potentially save money on your premiums. This guide serves as your roadmap to understanding and managing your car insurance costs effectively.

Factors Influencing Car Insurance Costs

Several key factors interact to determine the final cost of your car insurance premium. Understanding these factors can help you make informed decisions and potentially save money. These factors range from your personal characteristics to the vehicle you drive and where you live.

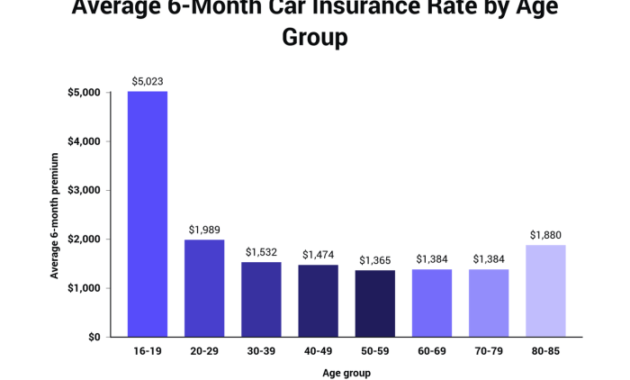

Age and Car Insurance Premiums

Age significantly impacts car insurance costs. Younger drivers, typically under 25, generally pay higher premiums due to statistically higher accident rates in this age group. Insurance companies perceive them as higher risk. As drivers gain experience and reach their mid-twenties and beyond, their premiums usually decrease, reflecting a lower risk profile. This reduction continues until a certain age, after which premiums may stabilize or even slightly increase due to factors like potential health concerns affecting driving ability. For example, a 18-year-old driver might pay significantly more than a 35-year-old driver with a similar driving record and vehicle.

Car Make and Model and Insurance Costs

The make and model of your car directly influence your insurance premium. Vehicles with a history of high repair costs, frequent theft, or a propensity for accidents tend to have higher insurance rates. Sports cars and luxury vehicles often fall into this category. Conversely, cars known for their safety features, reliability, and lower repair costs generally result in lower premiums. For instance, a compact sedan with a good safety rating might be cheaper to insure than a high-performance sports car.

Driving History’s Impact on Insurance Rates

Your driving history is a crucial factor in determining your insurance costs. Accidents and traffic violations significantly increase premiums. The severity of the accident and the number of violations directly correlate with the increase. A clean driving record, on the other hand, can lead to significant discounts. For example, a driver with two at-fault accidents in the past three years will likely pay considerably more than a driver with a spotless record. Similarly, multiple speeding tickets can result in higher premiums.

Location and Average Insurance Premiums

Geographic location plays a significant role in car insurance costs. Urban areas typically have higher premiums than rural areas due to increased traffic congestion, higher accident rates, and a greater risk of theft. Factors like the density of population, crime rates, and the cost of repairs in a specific region also contribute. A driver living in a bustling city center might pay substantially more than a driver in a sparsely populated rural area, even with identical driving records and vehicles.

Comparison of Coverage Levels and Costs

The following table compares average annual insurance costs for different coverage levels. These are illustrative examples and actual costs will vary based on the factors discussed above.

| Coverage Level | Liability Only (example) | Liability + Collision (example) | Liability + Collision + Comprehensive (example) |

|---|---|---|---|

| Annual Premium | $500 | $800 | $1000 |

Average Costs by State/Region

Car insurance premiums vary significantly across the United States, influenced by a multitude of factors including population density, accident rates, and the cost of vehicle repairs. Understanding these regional differences is crucial for consumers seeking the best value for their insurance needs. This section will explore average costs in specific states and examine the broader trends across different population densities.

Average Costs in Selected States

The following table presents the average annual cost of car insurance for a minimum coverage policy in five diverse states, as of late 2023. These figures are estimates based on industry averages and may vary depending on individual circumstances and insurer.

| State | Average Annual Cost |

|---|---|

| Maine | $1,200 |

| Michigan | $1,800 |

| California | $1,500 |

| Texas | $1,400 |

| Florida | $2,000 |

Regional Variation in Average Costs

A visual representation, such as a choropleth map (a thematic map in which areas are shaded or patterned in proportion to the measurement of the statistical variable being displayed), would effectively illustrate the variation in average car insurance costs across the United States. Such a map would show states colored according to their average premium, ranging from light shades for lower costs to dark shades for higher costs. Key data points would include the highest and lowest average costs, as well as regional clusters of similar pricing. For example, one might observe higher costs concentrated in densely populated coastal areas and in states with higher-than-average accident rates, while lower costs might be prevalent in less populated rural regions. The overall trend would highlight the significant disparity in premiums across different regions.

Comparison of High and Low Population Density Areas

Generally, car insurance premiums tend to be higher in high-population density areas compared to low-population density areas. Several factors contribute to this disparity. High-population areas often experience higher accident rates due to increased traffic congestion and driver interactions. The frequency of vehicle theft and vandalism is also often greater in densely populated urban centers. Furthermore, the cost of vehicle repairs and medical care tends to be higher in these areas. In contrast, low-population density areas typically experience lower accident rates and fewer claims, leading to lower average premiums. For example, a driver in New York City might pay significantly more than a driver in rural Montana due to these factors.

Insurance Company Comparison

Choosing the right car insurance provider can significantly impact your annual expenses. Understanding the differences in premiums and discounts offered by various companies is crucial for making an informed decision. This section compares three major car insurance companies, examines their discount structures, and explores the factors influencing their pricing variations.

Average Premiums Comparison

The average premiums offered by car insurance companies vary considerably based on several factors including location, driving history, and the type of coverage selected. It’s impossible to provide exact figures applicable to all situations, as rates are dynamically calculated. However, we can illustrate a general comparison using hypothetical average annual premiums for a standard driver profile (e.g., a 35-year-old with a clean driving record, driving a mid-sized sedan, and opting for minimum state-required liability coverage). Remember that these are illustrative examples and your actual premiums will differ.

| Insurance Company | Estimated Average Annual Premium | Strengths | Weaknesses |

|---|---|---|---|

| Progressive | $1200 | Wide range of discounts, strong online tools | Customer service can be inconsistent |

| State Farm | $1350 | Excellent customer service reputation, broad network of agents | May not offer the most competitive rates in all areas |

| Geico | $1100 | Highly competitive rates, strong online presence | Fewer physical agent locations |

Discounts Offered by Major Insurance Providers

Many insurance companies offer a variety of discounts to incentivize safe driving and responsible behavior. These discounts can significantly reduce your overall premium.

A common range of discounts include:

Discounts are frequently offered for:

- Good Driver Discounts: Awarded for maintaining a clean driving record, typically free of accidents and traffic violations for a specified period.

- Bundling Discounts: Offered for bundling multiple insurance policies (e.g., car insurance and homeowners insurance) with the same company.

- Safe Driver Discounts: Often require installation of telematics devices that monitor driving habits and reward safe driving behaviors.

- Vehicle Safety Features Discounts: Discounts are applied if your vehicle has advanced safety features like anti-theft systems, airbags, or anti-lock brakes.

- Good Student Discounts: Offered to students who maintain a certain GPA.

- Military Discounts: Provided to active-duty military personnel and veterans.

Factors Contributing to Pricing Differences

Several factors contribute to the variations in pricing among insurance companies. These include:

Key factors impacting pricing include:

- Risk Assessment Models: Each company uses different algorithms and data to assess risk, leading to varying premium calculations.

- Operating Costs: Companies with extensive agent networks or higher administrative costs may have higher premiums.

- Profit Margins: Insurance companies have different profit targets, influencing their pricing strategies.

- Claims Handling Practices: Companies with more efficient claims processing may offer lower premiums.

- Geographic Location: Premiums vary based on location due to differences in accident rates, theft rates, and repair costs.

Impact of Driving Habits

Your driving habits significantly influence your car insurance premiums. Insurance companies assess risk, and your driving behavior is a key factor in determining how risky they perceive you to be. Factors like annual mileage, commuting distance, and adherence to safe driving practices all play a role in the final cost of your insurance.

Your annual mileage directly impacts your premium. The more miles you drive, the greater your exposure to accidents. Insurance companies understand this correlation and adjust premiums accordingly. Someone who drives 5,000 miles a year will typically pay less than someone who drives 25,000 miles annually, all other factors being equal. This is because the higher-mileage driver has a statistically higher chance of being involved in a collision.

Mileage’s Influence on Premiums

The relationship between annual mileage and insurance cost isn’t linear, but it’s generally positive. For example, a driver who reports 10,000 miles per year might see a noticeably lower premium than someone who drives 20,000 miles, and that difference might not be double the cost. Insurance companies often use tiered systems or specific mileage brackets to determine premium adjustments, factoring in other risk elements. Many insurers offer discounts for low-mileage drivers, recognizing their reduced risk profile. Accurate reporting of mileage is crucial; misrepresenting it could lead to policy issues.

Commuting Distance and Insurance Costs

Commuting distance is a significant factor because it increases exposure to traffic, potentially hazardous road conditions, and higher chances of accidents. Daily commutes through congested city centers, for instance, are statistically riskier than commutes on less-trafficked rural roads. Insurers often consider commuting distance as part of their risk assessment. A longer commute, especially in high-traffic areas, will usually result in a higher premium than a shorter commute in a less congested area. For example, a driver with a 20-mile daily commute in a major city might pay more than someone with a 5-mile commute in a suburban area.

Safe Driving Practices and Lower Insurance Rates

Adopting safe driving practices can significantly lower your insurance premiums. Many insurance companies offer discounts for drivers with clean driving records, demonstrating a commitment to safety.

Safe driving practices that can lead to lower rates include:

Maintaining a clean driving record (no accidents or tickets). A history of accidents or traffic violations increases your perceived risk, leading to higher premiums.

Defensive driving techniques: This involves anticipating potential hazards, maintaining a safe following distance, and avoiding distractions like cell phone use while driving. Defensive driving courses can sometimes earn discounts.

Regular vehicle maintenance: Ensuring your car is in good working order reduces the likelihood of mechanical failures that could cause accidents. Properly maintained vehicles are safer.

Avoiding risky driving behaviors: This includes speeding, aggressive driving, and driving under the influence of alcohol or drugs. These actions significantly increase your risk profile.

By consistently practicing safe driving, drivers can demonstrate their commitment to responsible driving, thereby reducing their insurance costs. Insurance companies often reward this behavior with discounts or lower premiums.

Final Thoughts

Ultimately, understanding your car insurance average cost requires a holistic approach. It’s not simply about finding the cheapest policy; it’s about finding the right balance between cost and coverage that aligns with your individual needs and risk profile. By carefully considering the factors discussed—age, driving history, vehicle choice, location, and coverage levels—and by comparing quotes from multiple insurers, you can significantly improve your chances of securing a policy that offers both comprehensive protection and affordable premiums. Take control of your car insurance costs; the information is at your fingertips.

FAQ Explained

What is considered a good credit score for car insurance?

Generally, a credit score above 700 is considered good and can qualify you for lower car insurance rates. Scores below 660 often result in higher premiums.

How often can I expect my car insurance rates to change?

Rates can change annually, or even more frequently, depending on your insurer and any changes in your driving record or risk profile. Review your policy regularly.

Can I get car insurance if I have a DUI on my record?

Yes, but it will likely be significantly more expensive, and you may need to obtain a high-risk policy from a specialized insurer.

What is the difference between liability and collision coverage?

Liability covers damages you cause to others, while collision covers damage to your own vehicle, regardless of fault.