Car insurance NJ is a necessity for all drivers in the Garden State, and understanding its complexities can be overwhelming. This guide delves into the intricacies of car insurance in New Jersey, providing insights into coverage options, factors affecting premiums, and tips for saving money.

Navigating the world of car insurance can feel like driving through a maze, but with the right knowledge, you can find the best coverage at a price that fits your budget.

Understanding Car Insurance in New Jersey

Driving a car in New Jersey requires you to have car insurance. It protects you financially in case of an accident. This insurance covers damages to your vehicle and injuries to yourself or others.

Types of Car Insurance Coverage

Car insurance in New Jersey is divided into different types of coverage. Each type protects you from specific risks. Understanding these types helps you choose the right coverage for your needs.

- Liability Coverage: This is the most basic type of car insurance. It covers damages to other people’s property or injuries caused by you in an accident. It includes two parts:

- Bodily Injury Liability: This covers medical expenses, lost wages, and pain and suffering for people injured in an accident caused by you.

- Property Damage Liability: This covers repairs or replacement costs for damages to another person’s vehicle or property in an accident caused by you.

- Personal Injury Protection (PIP): This coverage pays for your medical expenses and lost wages, regardless of who caused the accident. It also covers medical expenses for passengers in your car.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): This coverage protects you if you are involved in an accident with a driver who doesn’t have insurance or has insufficient coverage. It helps pay for your medical expenses, lost wages, and property damage.

- Collision Coverage: This coverage pays for repairs or replacement costs for your vehicle if it is damaged in an accident, regardless of who caused it.

- Comprehensive Coverage: This coverage pays for damages to your vehicle caused by events other than accidents, such as theft, vandalism, or natural disasters.

Minimum Liability Coverage Requirements

New Jersey law requires drivers to carry a minimum amount of liability coverage. These minimums are:

- Bodily Injury Liability: $15,000 per person/$30,000 per accident.

- Property Damage Liability: $5,000 per accident.

Benefits of Additional Coverage

While the minimum liability coverage is required, having additional coverage provides greater protection.

- Collision and Comprehensive Coverage: These coverages protect you from financial losses due to damages to your vehicle caused by accidents or other events.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): This coverage is crucial in a state like New Jersey, where a significant number of drivers may not have adequate insurance.

Factors Affecting Car Insurance Premiums in New Jersey

Several factors influence car insurance premiums in New Jersey, and understanding these factors can help you make informed decisions about your coverage and potentially save money.

Driving History

Your driving history is a major factor in determining your car insurance premium. A clean driving record with no accidents or violations will result in lower premiums. However, accidents, traffic violations, and DUI convictions can significantly increase your rates.

- Accidents: Accidents are a significant factor in premium calculations. The severity of the accident and whether you were at fault can heavily influence your rates.

- Traffic Violations: Traffic violations like speeding tickets, running red lights, and parking violations can also lead to higher premiums. The number and severity of violations play a role.

- DUI Convictions: DUI convictions are among the most serious offenses and can lead to substantial premium increases. Insurance companies view DUI convictions as a significant risk factor.

Age

Age is another crucial factor in car insurance premiums. Younger drivers, especially those under 25, generally face higher premiums due to their higher risk of accidents. Insurance companies statistically recognize that young drivers have less experience and may engage in riskier driving behaviors.

- Young Drivers: Young drivers are statistically more likely to be involved in accidents.

- Mature Drivers: Older drivers, especially those over 65, may also see higher premiums due to factors such as declining eyesight and slower reaction times.

Vehicle Type

The type of vehicle you drive significantly influences your insurance premium.

- Expensive Vehicles: High-performance vehicles, luxury cars, and vehicles with high repair costs are generally more expensive to insure.

- Safety Features: Vehicles equipped with safety features like anti-lock brakes, airbags, and electronic stability control can qualify for discounts, leading to lower premiums.

- Vehicle Age: Older vehicles, especially those more prone to breakdowns, may have higher premiums.

Credit Score

In New Jersey, insurance companies can use your credit score as a factor in determining your car insurance premium. This practice is controversial, but it’s important to understand its impact.

- Credit Score and Risk: Insurance companies argue that individuals with good credit are more financially responsible and, therefore, less likely to file fraudulent claims.

- Impact on Premiums: A higher credit score generally leads to lower premiums, while a lower credit score can result in higher premiums.

Location

Your location in New Jersey plays a role in your car insurance premium.

- Urban vs. Rural Areas: Urban areas with higher traffic density and greater risk of accidents often have higher insurance premiums.

- Crime Rates: Areas with higher crime rates, including car theft, can also lead to higher premiums.

Finding the Best Car Insurance in New Jersey: Car Insurance Nj

Finding the best car insurance in New Jersey requires careful research and comparison. With numerous providers offering various coverage options and prices, navigating this process can feel overwhelming. This section will guide you through the steps of finding the best insurance for your needs and budget.

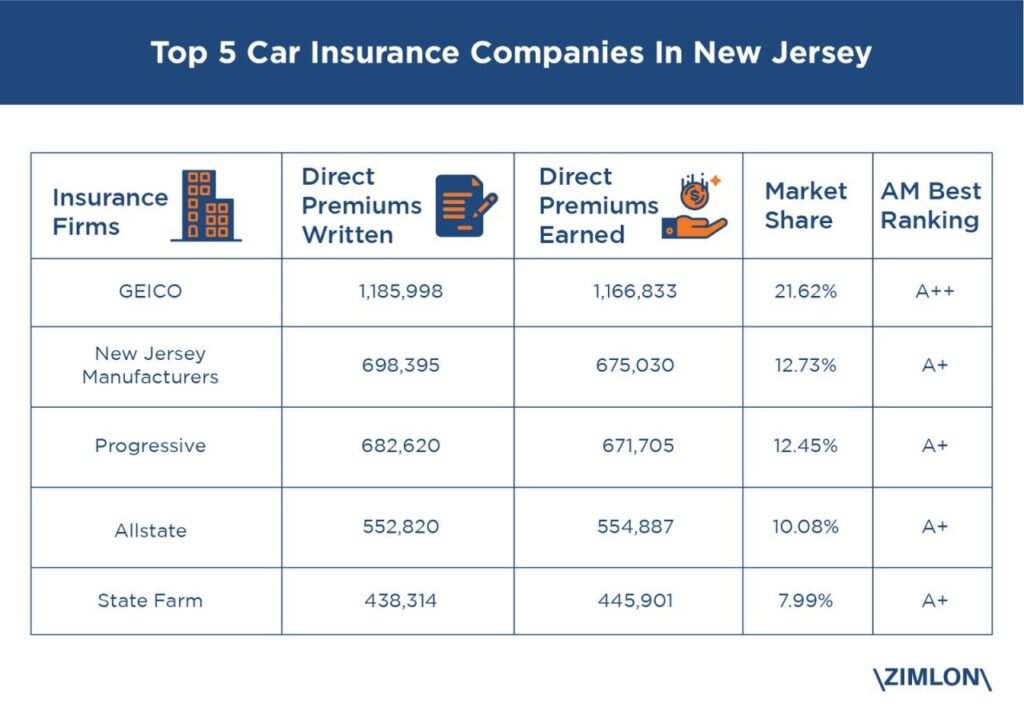

Comparing Car Insurance Providers in New Jersey

Comparing car insurance providers in New Jersey is crucial to finding the best value. Each provider has its own strengths and weaknesses, and it’s essential to understand these differences before making a decision. Here’s a comparison of some prominent providers in New Jersey:

- State Farm: Known for its extensive network of agents, comprehensive coverage options, and competitive pricing.

- Geico: Popular for its online-focused approach, offering convenient quotes and policy management. It’s often praised for its competitive rates.

- Progressive: Offers a wide range of discounts and customization options, allowing drivers to tailor their coverage to their specific needs.

- Allstate: Provides a strong reputation for customer service and a wide range of coverage options, including specialized insurance for high-value vehicles.

- Liberty Mutual: Offers competitive rates, especially for drivers with good driving records and multiple vehicles.

Obtaining Quotes from Multiple Insurers

To find the best car insurance rates, it’s vital to obtain quotes from multiple insurers. This process is straightforward and can be done online, over the phone, or through an insurance broker. Here’s a guide on how to obtain quotes:

- Gather your information: Before contacting insurers, have your driver’s license, vehicle registration, and any relevant information about your driving history readily available. This will streamline the quoting process.

- Use online comparison tools: Several online comparison websites allow you to enter your information once and receive quotes from multiple insurers simultaneously. This saves time and effort.

- Contact insurers directly: You can also contact insurers directly through their websites, phone numbers, or by visiting their local offices.

- Be transparent with your information: Provide accurate information about your driving history, vehicle details, and any other relevant factors to ensure you receive accurate quotes.

Evaluating Car Insurance Policies

Once you’ve received quotes from multiple insurers, it’s time to carefully evaluate the policies and choose the best option. Consider the following checklist:

- Coverage: Ensure the policy provides the coverage you need, including liability, collision, comprehensive, and uninsured/underinsured motorist coverage.

- Deductibles: Choose deductibles that balance your risk tolerance with your budget. Higher deductibles typically result in lower premiums but mean you’ll pay more out-of-pocket in case of an accident.

- Premiums: Compare the monthly premiums from different insurers and ensure they fit within your budget.

- Discounts: Explore available discounts, such as good driver discounts, safe driver discounts, multi-car discounts, and bundling discounts for home and auto insurance.

- Customer service: Consider the insurer’s reputation for customer service, claims handling, and overall responsiveness. Look for positive reviews and ratings from other customers.

Understanding New Jersey’s Car Insurance Laws

New Jersey has a unique car insurance system that differs from many other states. Understanding the regulations and requirements is crucial for every driver in the state. This section delves into the key aspects of New Jersey’s car insurance laws, providing a clear overview of the no-fault system, the claims process, and other essential information.

New Jersey’s No-Fault Insurance System

New Jersey operates under a no-fault insurance system. This means that after an accident, each driver involved files a claim with their own insurance company, regardless of who caused the accident. This system aims to streamline the claims process and reduce litigation. Under the no-fault system, drivers are primarily compensated for their own injuries and losses, regardless of who caused the accident. This is typically handled through Personal Injury Protection (PIP) coverage.

Filing a Claim in New Jersey, Car insurance nj

When an accident occurs, drivers must file a claim with their insurance company. The process involves:

- Reporting the accident: Notify your insurance company as soon as possible after the accident.

- Providing details: You’ll need to provide information about the accident, including the date, time, location, and details of the other vehicles involved.

- Submitting a claim: You’ll need to file a claim with your insurance company, including details about your injuries and losses.

- Supporting documentation: You may need to provide supporting documentation, such as medical bills, repair estimates, or police reports.

The New Jersey Department of Banking and Insurance (DOBI) plays a vital role in overseeing the insurance industry and ensuring fair treatment for policyholders. If you have a dispute with your insurance company, you can contact the DOBI for assistance.

Driver’s Licenses, Vehicle Registration, and Insurance Verification in New Jersey

New Jersey has specific requirements for driver’s licenses, vehicle registration, and insurance verification.

- Driver’s Licenses: All drivers in New Jersey must have a valid driver’s license. You can apply for a driver’s license at a New Jersey Motor Vehicle Commission (MVC) agency.

- Vehicle Registration: All vehicles driven in New Jersey must be registered with the MVC. You can register your vehicle at an MVC agency.

- Insurance Verification: You must provide proof of insurance to the MVC when you register your vehicle. This ensures that you have the required minimum coverage for your vehicle.

New Jersey law requires all drivers to carry proof of insurance in their vehicles. This could be a physical insurance card or a digital copy on your smartphone.

Tips for Saving on Car Insurance in New Jersey

Car insurance in New Jersey can be expensive, but there are several ways to reduce your premiums and save money. By understanding the factors that affect your rates and implementing smart strategies, you can find the best coverage at a price that fits your budget.

Discounts and Bundling

Discounts are a valuable way to reduce your car insurance costs in New Jersey. Many insurers offer a wide range of discounts for various factors, such as good driving records, safety features in your car, and bundling insurance policies.

- Good Driver Discounts: Maintaining a clean driving record with no accidents or violations can significantly lower your premiums. Insurers reward safe drivers with discounts, demonstrating their commitment to responsible driving.

- Safe Vehicle Discounts: Vehicles equipped with advanced safety features, such as anti-theft devices, airbags, and anti-lock brakes, often qualify for discounts. These features reduce the risk of accidents and injuries, making your car a safer investment.

- Bundling Discounts: Combining your car insurance with other policies, such as homeowners or renters insurance, can result in significant savings. Insurers often offer discounts for bundling multiple policies, rewarding loyalty and simplifying your insurance needs.

- Other Discounts: Many insurers offer discounts for various other factors, such as being a good student, completing a defensive driving course, or being a member of certain organizations. Exploring these options can lead to substantial savings on your premiums.

Safe Driving Practices

Safe driving habits are crucial for reducing your risk of accidents and earning discounts. Insurers recognize the value of safe driving and reward drivers who prioritize safety on the road.

- Defensive Driving: Participating in a defensive driving course can not only improve your driving skills but also qualify you for discounts. These courses teach strategies for avoiding accidents and managing risky situations, making you a safer driver.

- Maintaining Your Vehicle: Regular vehicle maintenance is essential for safety and can also influence your insurance rates. Ensuring your car is in good working order, with regular oil changes and tire rotations, demonstrates responsible car ownership.

- Avoiding Distractions: Distracted driving is a major cause of accidents. By minimizing distractions, such as using your phone or eating while driving, you reduce your risk of accidents and demonstrate a commitment to safe driving.

Car Insurance and Accidents in New Jersey

Accidents are an unfortunate reality on the road, and navigating the aftermath can be stressful. Understanding the procedures and responsibilities involved is crucial for New Jersey drivers. This section will guide you through the process of reporting accidents, filing claims, and understanding the legal responsibilities of drivers involved in accidents. We’ll also explore the role of insurance companies in handling accident claims.

Reporting Accidents and Filing Claims

After an accident, the first step is to ensure the safety of everyone involved. If anyone is injured, call 911 immediately. If the accident involves only property damage and everyone is safe, you should:

- Exchange information: Gather the other driver’s contact information, insurance details, and license plate number.

- Document the accident: Take pictures of the damage to your vehicle and the other vehicle, as well as the accident scene.

- Contact your insurance company: Report the accident to your insurance company as soon as possible, even if the damage seems minor.

In New Jersey, you are required to file a police report if the accident results in an injury or property damage exceeding $500. You can file the report online or in person at a local police station.

Legal Responsibilities of Drivers Involved in Accidents

New Jersey law requires drivers to be financially responsible for any damages they cause in an accident. This means that you are legally obligated to pay for any injuries or property damage you cause to others.

- Fault: Determining fault in an accident is crucial for insurance purposes. The driver who is deemed at fault is responsible for covering the costs of the accident. In some cases, multiple drivers may share fault.

- No-Fault Insurance: New Jersey has a no-fault insurance system, which means that drivers must first file claims with their own insurance companies, regardless of who is at fault. This system is designed to expedite the claims process and reduce litigation.

Role of Insurance Companies in Handling Accident Claims

Your insurance company plays a significant role in the aftermath of an accident. They will handle the claims process, including:

- Investigating the accident: Your insurance company will investigate the accident to determine fault and the extent of damages.

- Negotiating with other insurance companies: If the other driver is at fault, your insurance company will negotiate with their insurance company to settle the claim.

- Providing coverage: Your insurance company will provide coverage for your medical expenses, lost wages, and property damage, up to the limits of your policy.

It’s important to cooperate with your insurance company and provide them with all the necessary information and documentation. This will help ensure a smooth and efficient claims process.

Wrap-Up

Whether you’re a new driver or a seasoned veteran of the roads, understanding car insurance in New Jersey is crucial for staying safe and financially secure. By carefully considering your coverage options, comparing quotes, and following the tips Artikeld in this guide, you can ensure you have the right protection for your vehicle and yourself.

FAQ Insights

What are the minimum liability coverage requirements in New Jersey?

New Jersey requires drivers to carry a minimum of $15,000 in liability coverage per person, $30,000 per accident, and $5,000 for property damage.

How can I get a discount on my car insurance?

There are many ways to save on car insurance, including safe driving courses, bundling policies, and maintaining a good credit score.

What happens if I get into an accident in New Jersey?

New Jersey operates under a no-fault insurance system, meaning you file a claim with your own insurance company, regardless of who caused the accident.

What is the role of the New Jersey Department of Banking and Insurance?

The Department of Banking and Insurance regulates the insurance industry in New Jersey, ensuring fair practices and protecting consumers.