Navigating the complex world of car insurance in New York City can feel overwhelming. Premiums vary drastically based on numerous factors, leaving drivers searching for the best possible rates. This guide delves into the intricacies of finding the cheapest car insurance in NYC, exploring the key elements that influence costs and providing actionable strategies to secure affordable coverage.

From understanding the impact of your driving history and vehicle type to leveraging discounts and effectively negotiating with insurers, we’ll equip you with the knowledge and tools to make informed decisions. We’ll compare major providers, highlight cost-saving strategies, and offer insights into policy details to ensure you’re fully protected without breaking the bank.

Understanding NYC Car Insurance Costs

Securing affordable car insurance in New York City can feel like navigating a maze. The cost of insurance in NYC is significantly higher than the national average, influenced by a complex interplay of factors. Understanding these factors is crucial to finding the best policy for your needs and budget.

Factors Influencing NYC Car Insurance Premiums

Several key factors determine your car insurance premium in NYC. These factors are assessed by insurance companies to determine your risk profile, ultimately affecting the price you pay. Higher-risk drivers generally pay more.

| Driver Profile | Average Annual Premium | Factors Affecting Cost | Savings Tips |

|---|---|---|---|

| Young, Inexperienced Driver (20 years old, no accidents) | $3,000 – $5,000 | Age, lack of driving history, potential for risky behavior | Consider a telematics program, maintain a clean driving record, explore discounts for good students. |

| Experienced Driver with Minor Accidents (35 years old, 1 accident in 5 years) | $1,500 – $2,500 | Driving history (one accident), age, vehicle type | Maintain a clean driving record for several years, consider increasing your deductible. |

| Senior Driver (65 years old, clean driving record) | $1,000 – $2,000 | Age, generally lower risk profile due to experience and statistically fewer accidents. | Explore senior citizen discounts, bundle insurance policies. |

| Driver in High-Crime Area (Manhattan, Brooklyn) | $2,000 – $4,000 | Location (higher theft and accident rates), vehicle type (luxury cars are more expensive to insure) | Consider parking in secure garages, explore different coverage options. |

Types of Car Insurance Coverage in NYC

New York State mandates specific minimum coverage levels, but you can choose higher coverage limits for greater protection. Understanding the different types of coverage is essential to making an informed decision. These coverages protect you financially in case of accidents or damage to your vehicle.

Impact of Traffic Violations and Accidents on Insurance Rates

Traffic violations and accidents significantly impact your insurance premiums. Each incident is considered a risk factor, leading to increased premiums. For example, a speeding ticket might lead to a 10-20% increase, while an at-fault accident could result in a much larger increase, depending on the severity of the accident and your insurance history. Maintaining a clean driving record is crucial for keeping your premiums low.

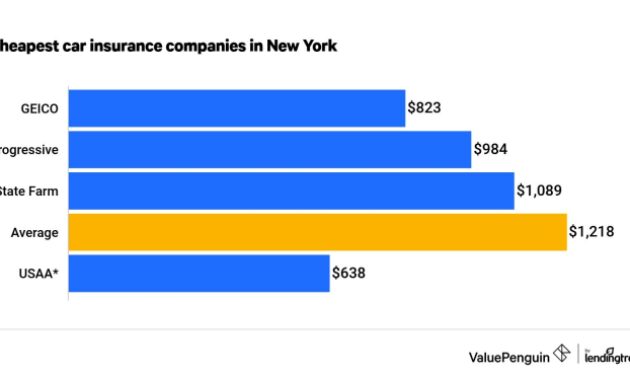

Finding the Cheapest Providers

Securing affordable car insurance in New York City requires understanding the diverse pricing strategies employed by insurance companies and leveraging available discounts. Navigating the market effectively involves comparing offers from multiple providers and utilizing online tools designed to simplify the process.

Major car insurance companies in NYC utilize various pricing models, often based on sophisticated risk assessment algorithms. These algorithms consider factors like driving history, vehicle type, location, and credit score. While some companies might prioritize broader customer bases with slightly higher average premiums, others may focus on niche markets, offering potentially lower rates to drivers with specific profiles (e.g., those with excellent driving records or specific vehicle types). This competitive landscape necessitates careful comparison shopping.

Pricing Strategies of Major Car Insurance Companies

The pricing strategies of major insurers in NYC are complex and often proprietary. However, general trends can be observed. Some companies, known for their broader market reach, may offer slightly higher average premiums but provide extensive coverage options and customer service. Conversely, other insurers may focus on attracting price-sensitive customers by offering more limited coverage at lower rates. Understanding this spectrum is crucial for finding the best balance between cost and coverage. For example, a company like Geico might be known for its competitive pricing through targeted advertising and streamlined online processes, while a company like State Farm might offer a wider range of coverage options at a potentially higher premium.

Key Features and Benefits of Budget-Friendly Insurance Providers

Budget-friendly insurers often prioritize efficiency and digital tools to minimize operational costs, passing the savings onto the consumer. These providers may offer streamlined online applications, digital policy management, and automated claims processing. While the level of personalized customer service might be less extensive than with some larger companies, the cost savings can be significant. Features like telematics programs, which track driving behavior to offer discounts, are increasingly common among budget-friendly options. These programs incentivize safe driving and can lead to substantial premium reductions.

Discounts and Promotions Offered by NYC Insurers

Many insurers in NYC offer a variety of discounts to attract and retain customers. Common discounts include those for good driving records (accident-free periods), safe driver courses (completion of defensive driving programs), bundling home and auto insurance, and installing anti-theft devices. Additionally, some insurers provide discounts for students with good grades, military personnel, and affiliations with certain organizations. Seasonal promotions and limited-time offers are also frequently available. For example, a driver with a clean driving record for five years might qualify for a significant discount, while bundling home and auto insurance could result in a combined savings of 10-15%.

Reputable Insurance Comparison Websites

Several reputable websites facilitate the comparison of car insurance quotes from multiple providers. These platforms allow users to input their information once and receive multiple quotes simultaneously, simplifying the process of finding the cheapest option. Examples include The Zebra, NerdWallet, and Policygenius. These websites typically offer a wide range of insurers and allow for filtering based on coverage options and price points, enabling a thorough comparison before selecting a policy. Using these resources is highly recommended to avoid manually contacting numerous insurance companies individually.

Strategies for Lowering Insurance Costs

Securing affordable car insurance in New York City can feel like navigating a maze, but implementing the right strategies can significantly reduce your premiums. Understanding your options and taking proactive steps can lead to substantial savings. This section Artikels effective methods to lower your car insurance costs.

Increasing Deductibles

Raising your deductible, the amount you pay out-of-pocket before your insurance coverage kicks in, is a common way to lower your premiums. A higher deductible means lower monthly payments, as you’re essentially accepting more financial risk upfront. However, carefully consider your financial situation before increasing your deductible; ensure you can comfortably afford the higher out-of-pocket expense in case of an accident. For example, increasing your deductible from $500 to $1000 could result in a noticeable decrease in your premium, but you would need to be prepared to pay $1000 in the event of a claim.

Bundling Policies

Many insurance companies offer discounts for bundling multiple policies. Combining your car insurance with homeowners or renters insurance, or even other types of coverage, can often lead to significant savings. This is because insurers reward loyalty and reduce their administrative costs by managing multiple policies for a single customer. The exact discount varies by insurer and policy type, but it’s generally worthwhile to inquire about bundling options.

Improving Driving Record

Maintaining a clean driving record is arguably the most effective way to lower your insurance premiums. Accidents and traffic violations significantly increase your risk profile, leading to higher rates. Driving safely, obeying traffic laws, and avoiding accidents are crucial. Even a single speeding ticket can impact your premiums for several years. Conversely, a long history of safe driving will likely result in lower rates over time, often reflected in discounts for safe driving records.

Defensive Driving Courses

Completing a state-approved defensive driving course can often lead to a discount on your car insurance. These courses teach safe driving techniques and strategies for avoiding accidents. By demonstrating a commitment to safe driving, you signal to insurers that you’re a lower-risk driver, justifying a reduction in your premiums. Many insurers offer specific discounts for completing these courses, so check with your provider for details. The course completion certificate serves as proof of completion, allowing you to claim the discount.

Obtaining Multiple Quotes

Comparing quotes from multiple insurers is essential to finding the cheapest car insurance. This involves obtaining quotes from at least three to five different companies. Start by using online comparison tools, which allow you to enter your information once and receive quotes from several insurers simultaneously. Then, contact the insurers directly to discuss specific details and potentially negotiate rates. Remember to provide consistent information across all quotes for accurate comparisons.

Negotiating with Insurance Companies

Don’t hesitate to negotiate with your insurance company. Explain your driving record, any safety features in your vehicle, or other factors that might make you a low-risk driver. Point out any discounts you’re eligible for and ask if they can offer a better rate. Be polite but firm in your request. Many insurers are willing to negotiate, particularly if you’ve been a loyal customer or if you’re considering switching providers. Document all communications and agreements in writing.

Understanding Policy Details

Choosing the cheapest car insurance in NYC is only half the battle; understanding the details of your policy is crucial to ensure you’re adequately protected. A seemingly low premium might leave you vulnerable if you don’t grasp the specifics of what’s covered and what’s excluded. This section clarifies essential policy components, common limitations, and potential scenarios where coverage might be denied or restricted.

Essential Components of a Standard NYC Car Insurance Policy

A standard New York car insurance policy typically includes several key coverages. Liability coverage protects you financially if you cause an accident that injures someone or damages their property. Uninsured/Underinsured Motorist coverage safeguards you if you’re involved in an accident with a driver who lacks sufficient insurance or is uninsured. Collision coverage pays for repairs to your vehicle regardless of fault, while Comprehensive coverage covers damage from events like theft, vandalism, or weather-related incidents. Personal Injury Protection (PIP) covers medical expenses and lost wages for you and your passengers, regardless of fault. Finally, Medical Payments coverage can help pay for medical bills, regardless of fault. The specific limits and details of each coverage will vary depending on your policy.

Common Exclusions and Limitations in Insurance Policies

Insurance policies often exclude certain types of damages or situations. For instance, damage caused by wear and tear, lack of proper maintenance, or driving under the influence of alcohol or drugs is typically not covered. Similarly, using your vehicle for illegal activities or operating it without a valid license can void your coverage. Many policies also have limitations on the amount they will pay for specific types of damages, such as rental car reimbursement or towing fees. Specific exclusions and limitations vary greatly between insurance providers and policy types; therefore, careful review of the policy document is essential.

Examples of Situations Where Insurance Coverage Might Be Denied or Limited

Consider these scenarios: If you’re involved in an accident while driving a vehicle not listed on your policy, your claim may be denied. If you fail to report an accident promptly to your insurance company, your claim might be affected. If you modify your vehicle significantly without notifying your insurer, your coverage could be reduced or invalidated. Furthermore, if you provide false information on your application, your policy could be canceled, and any claims you make could be denied. These are just a few examples; the specifics will depend on the wording of your individual policy.

Important Questions to Ask Insurance Providers Before Purchasing a Policy

Before committing to a policy, it’s crucial to ask clarifying questions. A thorough understanding of the policy’s terms and conditions is vital. To this end, you should ask: What are the specific limits of liability, collision, and comprehensive coverage? What are the deductibles for each coverage? Are there any exclusions or limitations on coverage? What is the process for filing a claim? What are the penalties for late payments? What is the cancellation policy? Does the policy include roadside assistance or rental car reimbursement? Are there any discounts available? By obtaining clear answers to these questions, you can make an informed decision about your car insurance needs and choose the policy that best suits your circumstances.

Illustrative Examples of Savings

Saving money on car insurance in NYC is achievable through strategic choices. The examples below demonstrate how seemingly small decisions can significantly impact your annual premium. Understanding these factors allows for informed choices leading to substantial cost reductions.

Car Type and Coverage Level Impact on Premiums

Choosing a vehicle impacts your insurance costs. Consider two drivers, both with clean driving records and similar profiles, but different cars. Driver A chooses a fuel-efficient, smaller sedan, while Driver B opts for a high-performance SUV. Driver A might receive a quote for $1,200 annually with liability-only coverage, while Driver B’s premium for the same coverage could be $1,800 due to the higher repair costs and perceived risk associated with the SUV. Adding collision and comprehensive coverage would further increase both premiums, but the difference between Driver A and Driver B would likely remain significant. For example, comprehensive coverage might add $300 to Driver A’s premium and $500 to Driver B’s, highlighting the impact of vehicle choice on the total cost.

Bundling Insurance Policies: A Case Study

Bundling home and auto insurance with the same provider often results in significant savings. Let’s imagine Sarah, who pays $1,500 annually for car insurance and $800 annually for homeowners insurance with separate companies. By bundling these policies with a single provider offering a 15% discount for bundled services, her total annual cost would decrease to $1,955 (1,500 * 0.85 + 800 * 0.85 = $1955). This represents a saving of $145 compared to her previous separate policies ($2300 – $1955 = $145).

Clean Driving Record Cost Savings

A clean driving record is a significant factor in determining insurance premiums. Compare two drivers with identical profiles, vehicles, and coverage levels, but different driving histories. Driver C has a clean record, while Driver D has been involved in a minor accident within the past three years. Driver C might receive a quote of $1,400, whereas Driver D’s quote could be $1,800 or more, reflecting the increased risk associated with their accident history. This $400 difference illustrates the substantial financial benefit of maintaining a safe driving record.

Infographic: Potential Savings from Cost-Reducing Strategies

The infographic would feature a bar graph comparing the average annual car insurance premiums in NYC under different scenarios. The horizontal axis would list the scenarios: “Standard Premium,” “Safe Driving Discount,” “Bundled Insurance,” “Fuel-Efficient Car,” and “Higher Deductible.” The vertical axis would represent the annual premium cost in dollars. The bars would visually demonstrate the cost reductions associated with each strategy. For example, the “Standard Premium” bar might be $1,600, while the “Safe Driving Discount” bar might be $1,200 (a $400 reduction), “Bundled Insurance” $1,360 (a further reduction from the safe driving discount), “Fuel-Efficient Car” $1,100 and “Higher Deductible” $1,000. Below the graph, a small table would summarize the percentage savings for each strategy. The infographic’s color scheme would be clean and professional, utilizing a combination of blues and greens to convey a sense of trust and financial stability. The overall design would be simple and easy to understand, clearly highlighting the significant savings achievable through various cost-reducing measures.

Epilogue

Securing the cheapest car insurance in NYC requires careful planning and research. By understanding the factors that influence premiums, comparing providers, and employing cost-saving strategies, New York City drivers can significantly reduce their insurance expenses. Remember, a thorough understanding of your policy and proactive engagement with your insurer are key to maximizing savings and ensuring you have the right coverage for your needs. Don’t settle for overpriced insurance – take control of your premiums today.

Question & Answer Hub

What is SR-22 insurance and do I need it?

SR-22 insurance is proof of financial responsibility required by the state after certain driving offenses (like DUI). You only need it if mandated by the DMV.

Can I get car insurance if I have a DUI?

Yes, but it will likely be significantly more expensive. You’ll need to shop around and be upfront about your driving record.

How often can I change my car insurance provider?

You can typically switch providers whenever your current policy renews. There may be cancellation fees depending on your policy.

What is the difference between liability and comprehensive coverage?

Liability covers damages you cause to others. Comprehensive covers damage to your own vehicle from events like theft or weather.

What documents do I need to get a car insurance quote?

You’ll generally need your driver’s license, vehicle information (VIN, year, make, model), and driving history.