Navigating the world of auto insurance in Michigan can feel like driving through a blizzard – confusing and potentially costly. Michigan’s unique no-fault system significantly impacts insurance premiums, making finding inexpensive coverage a priority for many drivers. This guide cuts through the complexities, offering practical strategies and insights to help you secure affordable auto insurance without compromising essential protection.

We’ll explore the intricacies of Michigan’s insurance market, examining factors influencing costs, comparing coverage options, and providing actionable steps to lower your premiums. From understanding your driving record’s impact to negotiating rates effectively, this guide empowers you to make informed decisions and secure the best possible coverage at a price that fits your budget.

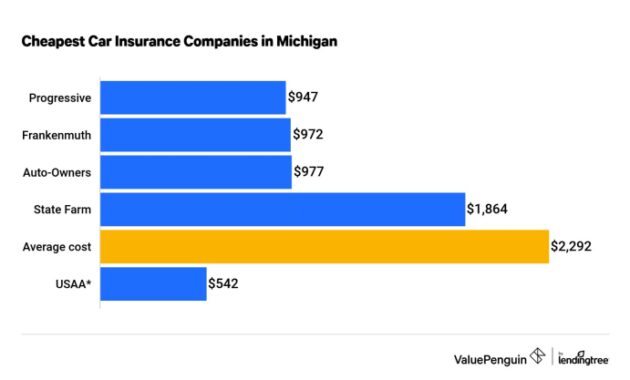

Understanding Michigan’s Auto Insurance Market

Michigan’s auto insurance market is unique due to its no-fault system, which significantly impacts costs and coverage options. Understanding the intricacies of this system is crucial for residents seeking affordable insurance. This section provides a comprehensive overview of the Michigan auto insurance landscape, covering key aspects that influence pricing and coverage choices.

Michigan’s No-Fault Insurance System

Michigan operates under a no-fault auto insurance system, meaning that regardless of who caused an accident, your own insurance company covers your medical expenses and lost wages. This system, while designed to provide quicker access to benefits, has contributed to higher insurance premiums in the state compared to many others. The system mandates Personal Injury Protection (PIP) coverage, which pays for medical bills, rehabilitation, and lost wages, regardless of fault. However, it also allows for lawsuits in cases of serious injury or death, leading to significant legal costs that ultimately drive up premiums. The recent reforms aimed at giving consumers more choice regarding PIP coverage have begun to influence the market, but the system remains complex.

Factors Influencing Auto Insurance Costs in Michigan

Several factors interact to determine the cost of auto insurance in Michigan. These include driving history (accidents and tickets), age and gender of the driver, vehicle type and value, location of residence, and the selected coverage levels. Higher-risk drivers, those living in areas with higher accident rates, or those driving more expensive vehicles will generally pay more. Credit scores can also be a factor in determining premiums, although this is subject to regulation and varies among insurers. The type of coverage chosen, as detailed below, will significantly impact the overall cost. Finally, the insurance company itself plays a role, with different companies having different pricing structures and risk assessments.

Types of Auto Insurance Coverage in Michigan

Michigan law mandates several types of auto insurance coverage. Beyond the mandatory PIP, drivers must carry Property Damage Liability (PDL), which covers damage to another person’s property in an accident you cause. Uninsured/Underinsured Motorist (UM/UIM) coverage protects you if you’re involved in an accident with an uninsured or underinsured driver. Collision coverage pays for repairs to your vehicle regardless of fault, while Comprehensive coverage covers damage from events other than collisions, such as theft or weather damage. Choosing higher coverage limits for each of these types will increase the premium, offering greater financial protection. Drivers can opt for lower PIP coverage limits, which significantly reduces premiums, but also limits the benefits received in the event of an accident.

Average Auto Insurance Costs in Major Michigan Cities

The following table provides estimated average annual costs for different coverage levels in several major Michigan cities. These are averages and individual costs can vary significantly based on the factors discussed above. Note that these are estimates and may not reflect current market conditions. It is always recommended to obtain quotes from multiple insurers for the most accurate pricing.

| City | Minimum Coverage (PIP $2500) | Mid-Range Coverage (PIP $50,000) | High Coverage (PIP $Unlimited) |

|---|---|---|---|

| Detroit | $1500 | $2500 | $4000 |

| Grand Rapids | $1200 | $2000 | $3500 |

| Ann Arbor | $1300 | $2200 | $3800 |

| Lansing | $1100 | $1800 | $3200 |

Finding Affordable Auto Insurance Options

Securing affordable auto insurance in Michigan requires a proactive approach. Understanding your options and employing effective strategies can significantly reduce your premiums. This section Artikels resources, factors influencing cost, negotiation techniques, and a step-by-step guide for comparing quotes.

Finding the best auto insurance rates in Michigan involves leveraging various resources and understanding the factors that influence your premium. Many online comparison tools and independent insurance agents can assist in finding competitive quotes. Additionally, understanding your driving record, vehicle type, and coverage needs will significantly impact your ability to secure a lower rate.

Resources for Finding Inexpensive Auto Insurance Quotes

Several avenues exist for obtaining multiple auto insurance quotes in Michigan. These resources provide a convenient way to compare prices and coverage options from different insurers.

- Online Comparison Websites: Websites like The Zebra, NerdWallet, and Insurance.com allow you to input your information and receive quotes from multiple insurers simultaneously. This saves considerable time and effort in the search process.

- Independent Insurance Agents: These agents work with multiple insurance companies, allowing them to shop around for the best rates on your behalf. They can often provide personalized advice and assistance navigating the insurance process.

- Directly Contacting Insurance Companies: You can obtain quotes directly from individual insurance companies, such as AAA, State Farm, Geico, and Progressive. This allows you to explore specific company offerings and potentially negotiate rates.

Factors that Lower Auto Insurance Premiums

Several factors influence the cost of auto insurance. By focusing on these elements, you can potentially lower your premiums considerably.

- Good Driving Record: Maintaining a clean driving record with no accidents or traffic violations is crucial for securing lower rates. Insurance companies view drivers with a history of accidents as higher risk.

- Vehicle Choice: The type of vehicle you drive significantly impacts your insurance costs. Generally, safer, less expensive vehicles to insure. Consider factors like safety ratings, theft rates, and repair costs when choosing a vehicle.

- Location: Where you live impacts your insurance rates. Areas with higher crime rates or more accidents tend to have higher insurance premiums.

- Discounts: Many insurers offer various discounts, such as good student discounts, multi-car discounts, and safe driver discounts. Inquire about available discounts to potentially reduce your premium.

- Coverage Levels: While comprehensive coverage is beneficial, consider if you need the highest level of coverage for all aspects of your policy. Opting for slightly lower coverage levels, if appropriate, can lead to savings.

Strategies for Negotiating Lower Insurance Rates

Negotiating lower insurance rates requires a strategic approach. By presenting yourself as a low-risk driver and actively comparing quotes, you can increase your chances of securing a better deal.

- Shop Around: Obtaining multiple quotes from different insurers is crucial for identifying the most competitive rates. Don’t settle for the first quote you receive.

- Bundle Policies: Combining your auto insurance with other types of insurance, such as homeowners or renters insurance, can often result in significant discounts.

- Highlight Positive Driving History: Emphasize your clean driving record and any relevant safety courses you’ve completed when speaking with insurance agents or representatives.

- Consider Increasing Your Deductible: Raising your deductible can lead to lower premiums, but it’s important to weigh the potential savings against the increased out-of-pocket expense in the event of an accident.

- Negotiate Directly: Don’t hesitate to negotiate directly with insurance companies. Explain your situation and inquire about potential discounts or rate reductions.

Comparing Auto Insurance Quotes Effectively: A Step-by-Step Guide

Effectively comparing auto insurance quotes involves a systematic approach to ensure you are making an informed decision.

- Gather Information: Collect necessary information, including your driver’s license, vehicle information, and details about your driving history.

- Use Online Comparison Tools: Utilize online comparison websites to receive quotes from multiple insurers simultaneously.

- Contact Insurance Agents: Reach out to independent insurance agents to discuss your needs and obtain personalized quotes.

- Compare Coverage: Carefully compare the coverage offered by each insurer. Ensure the coverage meets your needs and complies with Michigan’s no-fault insurance laws.

- Review Policy Details: Thoroughly review the policy details, including premiums, deductibles, and any exclusions or limitations.

- Choose the Best Option: Select the policy that best balances cost and coverage based on your individual circumstances and risk tolerance.

Factors Affecting Insurance Premiums

Several key factors influence the cost of auto insurance in Michigan. Understanding these elements can help you make informed decisions to potentially lower your premiums. These factors interact in complex ways, so it’s crucial to consider them holistically.

Driving History

Your driving record significantly impacts your insurance rates. Insurance companies assess risk based on past driving behavior. A clean record, free of accidents and traffic violations, will generally result in lower premiums. Conversely, accidents, especially those resulting in significant damage or injuries, can lead to substantial premium increases. The severity and frequency of incidents are critical factors. For example, a single minor fender bender might result in a moderate increase, while multiple at-fault accidents or serious violations like DUI could lead to significantly higher premiums or even policy cancellation. Maintaining a safe driving record is the most effective way to keep your insurance costs down.

Age and Gender

Age and gender are statistical factors used by insurance companies to assess risk. Younger drivers, particularly those under 25, typically pay higher premiums due to statistically higher accident rates in this demographic. As drivers age and gain experience, their premiums generally decrease. Gender also plays a role, although the impact varies by insurer and state regulations. Historically, male drivers in certain age groups have been statistically associated with higher accident rates than female drivers, potentially resulting in higher premiums for males in those groups. However, this is a generalization, and individual driving records ultimately have a greater influence on rates.

Vehicle Type and Value

The type and value of your vehicle directly influence your insurance premiums. Sports cars and high-performance vehicles are generally more expensive to insure due to their higher repair costs and increased risk of theft. Conversely, smaller, less expensive vehicles typically have lower insurance premiums. The vehicle’s value also plays a significant role; insuring a new, expensive car will be more costly than insuring an older, less valuable one. This is because the insurer’s liability is higher in the event of an accident or theft. Consider the insurance costs when choosing a vehicle.

Common Discounts

Michigan insurers offer various discounts to incentivize safe driving and responsible insurance practices. These can significantly reduce your premiums.

- Good Student Discount: Offered to students maintaining a certain GPA.

- Safe Driver Discount: Rewards drivers with a clean driving record over a specified period.

- Multi-Vehicle Discount: Provides a discount for insuring multiple vehicles under the same policy.

- Multi-Policy Discount: Offers a discount for bundling auto insurance with other types of insurance, such as homeowners or renters insurance.

- Anti-theft Device Discount: Reduces premiums for vehicles equipped with anti-theft devices.

- Defensive Driving Course Discount: Completing a state-approved defensive driving course can often earn a discount.

High-Risk Drivers and Insurance

Finding affordable car insurance in Michigan can be challenging for drivers with less-than-perfect driving records. High-risk drivers often face significantly higher premiums due to their increased likelihood of accidents or violations. Understanding your options and the process is crucial to securing coverage.

Insurance Options for Drivers with Poor Driving Records

Several insurance companies in Michigan cater to high-risk drivers, though they typically charge higher premiums. These companies often utilize a points-based system to assess risk, considering factors like accidents, speeding tickets, and DUIs. Some insurers specialize in non-standard auto insurance, which is designed for drivers who have been rejected by standard insurers due to their driving history. It’s essential to shop around and compare quotes from multiple providers to find the most competitive rates. Consider factors beyond price, such as the level of coverage and the insurer’s reputation for claims handling.

Obtaining SR-22 Insurance in Michigan

An SR-22 is a certificate of insurance that proves you maintain the minimum liability coverage required by the state. Michigan requires high-risk drivers, often those with DUI convictions or multiple serious violations, to obtain an SR-22. This certificate is filed with the Michigan Secretary of State by your insurance company, verifying your compliance with the state’s minimum insurance requirements. The SR-22 itself isn’t insurance; it’s proof that you have the required insurance. You’ll need to maintain continuous coverage for a specified period, usually three to five years, depending on the severity of your driving infractions. Failure to maintain continuous coverage can result in license suspension. Obtaining an SR-22 usually means higher premiums than standard insurance.

Appealing a Denied Insurance Application

If your application for auto insurance is denied, you have the right to appeal the decision. The process typically involves providing additional information or documentation to support your case. This could include evidence of improved driving habits, completion of a defensive driving course, or a letter of explanation addressing the reasons for previous violations. You should carefully review the reasons for denial provided by the insurance company and gather any relevant documentation that contradicts those reasons. Contacting the insurer directly to discuss the denial and understand their concerns is often a crucial first step. If the appeal is unsuccessful, you might consider seeking assistance from a consumer protection agency or an attorney specializing in insurance disputes.

Comparison of Insurance Options for Drivers with Different Risk Levels

| Risk Level | Typical Premiums | Coverage Options | Insurance Type |

|---|---|---|---|

| Low Risk (Clean Driving Record) | Lower premiums | Broad range of coverage options available | Standard auto insurance |

| Medium Risk (Minor Violations) | Moderately higher premiums | Most standard coverage options available, some limitations may apply | Standard or Non-Standard auto insurance |

| High Risk (Serious Violations/Accidents) | Significantly higher premiums | Limited coverage options, often higher deductibles | Non-Standard auto insurance, SR-22 required |

| Extremely High Risk (Multiple serious offenses, DUI) | Very high premiums, potential difficulty finding coverage | Highly limited coverage options, potentially only minimum liability | Specialized high-risk insurers, SR-22 required, possible state-mandated coverage |

Choosing the Right Insurance Provider

Selecting the right auto insurance provider in Michigan is crucial for securing affordable and reliable coverage. The market offers a diverse range of companies, each with its own strengths and weaknesses. Careful consideration of various factors is essential to make an informed decision that best suits your individual needs and budget.

Comparing Michigan Auto Insurance Companies

Many insurance companies operate in Michigan, each offering different coverage options, pricing structures, and customer service experiences. Direct comparison is key. For example, AAA, Geico, and Progressive are three major players, each with a different approach to policy offerings and customer interaction. AAA often emphasizes local service and community involvement, while Geico and Progressive are known for their national advertising and online-focused approach. Smaller, regional insurers might offer more personalized service but potentially less expansive coverage options. Comparing quotes from several companies, including both national and regional providers, is the best way to find the best value.

Local versus National Insurers: Benefits and Drawbacks

Choosing between a local and a national insurer involves weighing several factors. Local insurers often provide more personalized service and may have a deeper understanding of the local community and its specific risks. However, they may have fewer resources and a smaller range of coverage options compared to national insurers. National insurers, conversely, often offer broader coverage choices, more advanced technology, and potentially lower premiums due to economies of scale. Their customer service, however, might be less personalized, potentially involving longer wait times or less direct interaction with local representatives. The ideal choice depends on individual priorities – prioritizing personalized service versus broader coverage and potentially lower cost.

Selecting an Insurer with Excellent Customer Service

Excellent customer service is paramount when choosing an auto insurance provider. Look for companies with readily available customer support channels, such as phone, email, and online chat. Read online reviews and check customer satisfaction ratings from independent sources like the Better Business Bureau to gauge the company’s responsiveness and effectiveness in handling customer issues. Consider factors like claim processing speed and the ease of communication with claims adjusters. A company with a history of resolving customer complaints efficiently and fairly is a strong indicator of reliable service.

Comparison of Three Leading Michigan Insurers

The following table visually compares three leading Michigan auto insurers: AAA, Geico, and Progressive. The comparison focuses on three key areas: average premium cost (based on a hypothetical profile of a 30-year-old driver with a clean driving record and a mid-range vehicle), customer service rating (based on aggregated online reviews and independent ratings), and coverage options (represented by the breadth of available coverages).

| Feature | AAA | Geico | Progressive |

|---|---|---|---|

| Average Premium (Hypothetical) | $1200/year | $1000/year | $1100/year |

| Customer Service Rating (Scale of 1-5, 5 being highest) | 4.5 | 4.0 | 4.2 |

| Coverage Options (Broad, Moderate, Limited) | Moderate | Broad | Broad |

Note: These figures are hypothetical examples for illustrative purposes only and should not be considered definitive. Actual premiums and ratings can vary significantly based on individual circumstances and location.

Understanding Your Policy

Understanding your Michigan auto insurance policy is crucial for protecting yourself financially in the event of an accident. A thorough understanding of its components, coverage limits, and claims process will ensure you’re prepared for any unforeseen circumstances. This section will break down the key aspects of a typical policy.

Key Components of a Michigan Auto Insurance Policy

A standard Michigan auto insurance policy typically includes several key components. These components work together to provide comprehensive coverage for various situations. The specific coverage and limits will depend on the policy you choose and the level of coverage you select. Common components include liability coverage, personal injury protection (PIP), property damage liability, uninsured/underinsured motorist coverage, and collision and comprehensive coverage. Each of these offers different types of protection.

Filing a Claim with Your Insurer

Filing a claim with your insurer involves a straightforward process, although the specific steps may vary slightly depending on your insurer. Generally, you will need to contact your insurer as soon as possible after an accident, providing them with all relevant details, including the date, time, location, and circumstances of the accident. You should also gather information from any other parties involved, including their contact information, insurance details, and driver’s license numbers. You will likely need to complete a claim form and provide any supporting documentation, such as police reports and photographs of the damage. Your insurer will then investigate the claim and determine the appropriate course of action.

Understanding Your Policy’s Coverage Limits

Your policy’s coverage limits define the maximum amount your insurer will pay for covered losses. These limits are usually expressed as numerical values, such as 25/50/10. This represents $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $10,000 for property damage per accident. Understanding these limits is essential, as exceeding them leaves you personally liable for any remaining costs. Carefully review your policy documents to understand your specific coverage limits for each type of coverage. For example, if your PIP coverage is $50,000, that is the maximum your insurer will pay for medical bills and lost wages, regardless of the actual cost of your injuries.

Examples of Covered and Uncovered Situations

Understanding which situations are covered and which are not is crucial for avoiding unexpected financial burdens. For instance, a collision with another vehicle resulting in damage to your car is typically covered under collision coverage. However, damage caused by a deer hitting your car would usually fall under comprehensive coverage. On the other hand, damage caused by driving under the influence of alcohol is generally not covered. Similarly, damage to your car from vandalism might be covered under comprehensive coverage, depending on the specific terms of your policy. A common misconception is that damage to your car while parked is always covered. However, this may depend on the cause of the damage; for instance, damage caused by a falling tree is usually covered, while damage caused by a neighbor backing into your car might be covered by their insurance or not covered at all, depending on the circumstances. Always review your policy documents for specific details and exclusions.

Conclusion

Securing inexpensive auto insurance in Michigan requires careful planning and informed decision-making. By understanding the factors that influence premiums, actively comparing quotes, and leveraging available discounts, you can significantly reduce your insurance costs. Remember, the key is to balance affordability with adequate coverage to protect yourself and your vehicle. This guide provides a solid foundation for your search, equipping you to navigate the Michigan auto insurance landscape with confidence and find a policy that meets your needs and budget.

FAQ Summary

What is the minimum car insurance coverage required in Michigan?

Michigan’s no-fault law requires specific minimum coverages for personal injury protection (PIP) and property damage liability (PDL). The exact amounts can change, so it’s best to check the current Michigan Department of Insurance and Financial Services website for the most up-to-date information.

How does my credit score affect my insurance rates?

In many states, including Michigan, your credit score can be a factor in determining your insurance premiums. A higher credit score often translates to lower rates.

Can I bundle my auto and home insurance for a discount?

Yes, many insurance companies offer discounts for bundling your auto and homeowners insurance policies. This is a common strategy to save money.

What is an SR-22 insurance form?

An SR-22 is a certificate of insurance that proves you have the minimum required liability coverage. It’s often required for high-risk drivers after a serious driving offense.