The unwavering bond between humans and their canine companions is undeniable, but the unforeseen costs of veterinary care can strain even the most robust budgets. This guide delves into the world of low-cost dog insurance, exploring how responsible pet ownership can be balanced with financial prudence. We’ll examine various coverage options, compare providers, and equip you with the knowledge to make informed decisions about protecting your furry friend’s health.

Navigating the complexities of pet insurance can feel daunting, but understanding the nuances of low-cost plans can unlock significant savings without compromising essential coverage. This exploration will demystify the process, enabling you to find a plan that aligns with your dog’s needs and your financial capabilities, ensuring peace of mind knowing your beloved pet is protected.

Defining “Low Cost Dog Insurance”

Low-cost dog insurance offers essential coverage at a more affordable price point than comprehensive plans. While it may not include every bell and whistle, it provides a valuable safety net for unexpected veterinary expenses, helping pet owners manage the financial burden of pet healthcare. Understanding the nuances of these plans is key to making an informed decision about your dog’s health protection.

Types of Coverage Offered Under Low-Cost Plans

Low-cost dog insurance plans typically offer a range of coverage options, although the extent of coverage will vary between providers. Commonly included are accident-only plans, which cover injuries resulting from accidents such as broken bones or lacerations. Some low-cost plans may also include limited illness coverage, focusing on specific conditions or offering a lower reimbursement percentage compared to comprehensive plans. It’s crucial to carefully review the policy wording to understand exactly what is and isn’t covered. For example, a plan might cover accidents and some illnesses, but with a maximum payout per year or a high deductible.

Factors Influencing the Cost of Dog Insurance

Several factors determine the cost of your dog’s insurance premium. Breed plays a significant role, as certain breeds are predisposed to specific health problems, resulting in higher premiums. For instance, a Great Dane, known for hip dysplasia, will generally cost more to insure than a Labrador Retriever. Age is another crucial factor; puppies typically have lower premiums than older dogs, as the risk of developing health issues increases with age. Your location also influences premiums, reflecting regional variations in veterinary care costs. Finally, the level of coverage you choose directly impacts the price; a comprehensive plan with a low deductible will naturally be more expensive than a basic accident-only plan.

Comparison of Low-Cost and Comprehensive Plans

Low-cost plans and comprehensive plans differ significantly in their coverage scope and cost. Comprehensive plans offer broader protection, covering a wider range of illnesses and accidents, often with higher reimbursement percentages and lower deductibles. Low-cost plans, on the other hand, provide more limited coverage, focusing on essential needs and offering lower premiums. The choice between the two depends on your budget and risk tolerance. A pet owner with a limited budget might opt for a low-cost plan to cover basic emergencies, while someone with a higher budget and a desire for maximum protection might prefer a comprehensive plan.

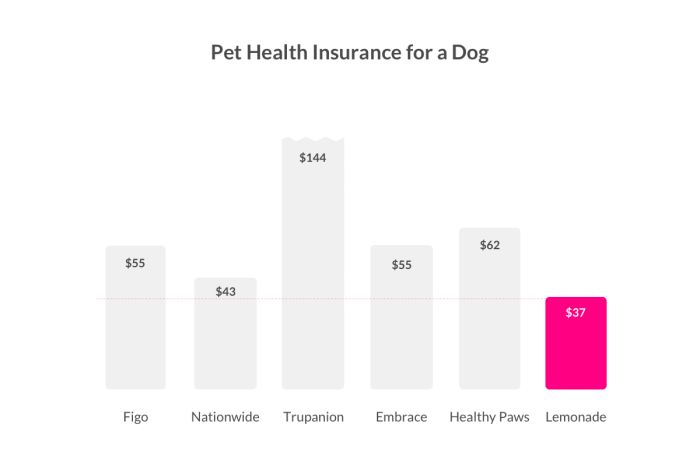

Comparison of Three Low-Cost Providers

The cost and coverage offered by low-cost dog insurance providers can vary significantly. It’s important to compare plans carefully before selecting one. The following table provides a simplified comparison, but always refer to the provider’s policy documents for complete details. Remember that prices and coverage details are subject to change.

| Provider | Accident Only Annual Premium (Example) | Accident & Illness Annual Premium (Example) | Key Features |

|---|---|---|---|

| Provider A | $150 | $300 | Limited illness coverage, high deductible |

| Provider B | $120 | $250 | Accident and illness, lower reimbursement percentage |

| Provider C | $180 | $350 | Broader illness coverage, lower deductible than A and B |

Finding and Evaluating Low-Cost Providers

Securing affordable dog insurance requires diligent research and a keen eye for detail. Navigating the market effectively involves understanding which providers offer genuinely low-cost plans without compromising essential coverage. This section will guide you through the process of identifying reputable providers and evaluating their offerings to find the best fit for your pet’s needs and your budget.

Finding suitable low-cost dog insurance involves comparing quotes from multiple providers and carefully examining the policy details. This ensures you get the best value for your money while avoiding unexpected costs or limited coverage down the line. Remember, the cheapest option isn’t always the best option; comprehensive coverage is crucial for your dog’s well-being.

Reputable Low-Cost Dog Insurance Providers

Several companies specialize in providing affordable dog insurance plans. Researching and comparing options from different providers is crucial to finding the best fit. While specific company names are subject to change and regional availability, look for companies with positive customer reviews and a proven track record of paying out claims fairly and promptly. Consider providers with transparent pricing structures and clear policy language. Checking independent review sites and online forums can offer valuable insights into the experiences of other pet owners.

Comparing Insurance Quotes

When comparing quotes, focus on more than just the premium. Consider the level of coverage offered, the deductible, the annual payout limit, and any exclusions. For example, a lower premium might come with a high deductible, meaning you’ll pay a significant amount out-of-pocket before the insurance kicks in. Similarly, a policy with a low annual payout limit might not cover extensive or long-term treatments. Compare the overall value, factoring in the potential costs of veterinary care, against the premium cost. A simple spreadsheet can be helpful in organizing and comparing different quotes side-by-side.

Reading Policy Details Carefully

Thoroughly reviewing the policy wording is crucial. Pay close attention to what is and isn’t covered. Many policies exclude pre-existing conditions, so understanding this exclusion is paramount. Look for clauses regarding waiting periods before coverage begins, limitations on specific treatments, and any exclusions related to breed-specific health issues. Don’t hesitate to contact the provider directly if you have any questions or require clarification on any aspect of the policy. Understanding the fine print protects you from unexpected costs and disappointments.

Evaluating Provider Trustworthiness and Financial Stability

Before committing to a provider, assess their financial stability and reputation. Check their Better Business Bureau (BBB) rating and look for any significant complaints or negative reviews. Investigate how long they have been in business, which indicates experience and stability. Consider whether the company is transparent about its claims-paying process and customer service record. A checklist might include: Checking the BBB rating, researching years in operation, reviewing customer testimonials and reviews, verifying state licensing and regulatory compliance, and inquiring about the claims payment process. A financially stable and reputable company is less likely to leave you stranded when you need them most.

Understanding Policy Coverage and Exclusions

Choosing low-cost dog insurance requires careful consideration of what’s covered and, equally importantly, what’s excluded. While attractive for their affordability, these policies often have limitations that can significantly impact your ability to afford veterinary care should your dog become ill or injured. Understanding these limitations is crucial before committing to a policy.

Common exclusions in low-cost dog insurance policies frequently involve pre-existing conditions, certain breeds deemed high-risk, and specific types of illnesses or injuries. Many also place limitations on the amount of coverage provided for certain procedures or illnesses, potentially leaving you with substantial out-of-pocket expenses. It’s vital to thoroughly review the policy document to avoid unpleasant surprises.

Common Exclusions in Low-Cost Dog Insurance

Low-cost dog insurance policies often exclude coverage for pre-existing conditions, meaning any health issues your dog had before the policy started. This can include hereditary conditions, allergies, or injuries sustained before the policy’s effective date. Additionally, some policies exclude specific breeds considered inherently prone to certain health problems, such as certain types of giant breeds or brachycephalic breeds. Finally, many low-cost plans limit coverage for certain conditions, such as cruciate ligament injuries or cancer treatments, which can be incredibly expensive. For example, a policy might cover only a portion of the cost of surgery for a torn ACL, leaving the owner responsible for a substantial co-pay.

Scenarios Where Low-Cost Plans Might Be Insufficient

Imagine your dog, a large breed predisposed to hip dysplasia, develops the condition. A low-cost policy might only offer limited coverage for treatment, leaving you with thousands of dollars in unexpected veterinary bills. Similarly, if your dog requires extensive cancer treatment, the cost could easily exceed the lifetime maximum coverage offered by a low-cost plan. Another example would be a dog needing emergency surgery for a swallowed foreign object; the emergency room visit and subsequent surgery could easily exhaust the annual coverage limit of a budget plan. These scenarios highlight the potential limitations of low-cost insurance and the importance of carefully evaluating your needs and budget.

Filing a Claim with a Low-Cost Insurer

The claim process typically involves submitting detailed veterinary bills and a completed claim form. Response times can vary significantly between insurers, with some low-cost providers potentially having longer processing times than their more expensive counterparts. Be sure to keep meticulous records of all veterinary visits and expenses to facilitate a smooth claims process. Understanding the insurer’s specific requirements and deadlines for submitting claims is essential to avoid delays or claim denials.

Essential Questions to Ask a Provider Before Purchasing

Before purchasing a low-cost dog insurance policy, it’s crucial to gather all necessary information. Specifically, inquire about the policy’s exclusions for pre-existing conditions and breed restrictions. Understanding the reimbursement percentage for different types of treatment and the annual and lifetime coverage limits is also essential. Inquire about the claim process, including required documentation and typical processing times. Finally, it’s advisable to compare several providers to ensure you are receiving the best coverage for your budget and your dog’s specific needs.

The Value of Pet Insurance

Pet insurance, especially low-cost options, presents a compelling case for responsible pet ownership. While the monthly premiums represent an ongoing expense, the potential savings against unforeseen veterinary bills can significantly outweigh the cost of coverage, offering peace of mind and financial protection. Weighing the cost of insurance against the potential costs of veterinary care without it is crucial for making an informed decision.

The cost of veterinary care can be surprisingly high. A single unexpected illness or injury can easily lead to thousands of dollars in bills for diagnostics, treatments, surgeries, and medications. Even routine care like vaccinations and dental cleanings accumulate over time. Low-cost pet insurance, however, provides a safety net, mitigating the financial burden of these costs. A monthly premium, often comparable to the cost of a few pet treats, can dramatically reduce the out-of-pocket expenses associated with veterinary care.

Comparison of Costs: Insurance vs. Uninsured Veterinary Care

Consider a scenario where your dog unexpectedly ingests a toxic substance requiring emergency treatment. Without insurance, the costs of emergency room visits, toxicology tests, induced vomiting, and subsequent monitoring could easily exceed $5,000. A low-cost insurance plan, even with a relatively high deductible, would significantly reduce this financial burden. The cost of the plan over a year might be $300-$500, but that’s considerably less than a potential $5,000 veterinary bill. This illustrates how low-cost insurance can offer substantial protection against catastrophic veterinary expenses. The difference between the cost of a yearly premium and the potential cost of a major veterinary event highlights the value proposition.

Managing Unexpected Veterinary Bills with Low-Cost Insurance

Unexpected illnesses and injuries are, unfortunately, a reality of pet ownership. A sudden onset of illness, a road accident, or a dog fight can result in significant and immediate veterinary expenses. Low-cost pet insurance helps manage these unexpected bills by covering a portion of the costs, depending on the plan’s coverage and deductible. This allows pet owners to focus on their pet’s recovery without the added stress of substantial financial burdens. For example, a low-cost plan might cover 80% of eligible veterinary costs after the deductible is met. This 80% reduction in expenses can be the difference between managing the situation comfortably and facing severe financial strain.

Examples of Invaluable Pet Insurance Coverage

Several scenarios highlight the value of pet insurance. For example, a dog diagnosed with cancer might require chemotherapy, radiation therapy, and ongoing medication, resulting in tens of thousands of dollars in costs. A chronic condition like diabetes requires ongoing management with insulin injections, blood glucose monitoring, and potential complications, all of which are costly. Even seemingly minor injuries, like a broken leg, can require surgery, hospitalization, and rehabilitation, leading to considerable expenses. In each of these cases, pet insurance, even a low-cost option, can provide crucial financial relief.

Long-Term Financial Benefits of Pet Insurance

The long-term financial benefits of pet insurance are significant.

- Budgetary Predictability: Regular premiums provide a predictable monthly expense, making it easier to budget for pet care.

- Reduced Financial Stress: Insurance mitigates the financial anxiety associated with unexpected veterinary bills.

- Access to Better Care: Insurance allows pet owners to afford better and more timely veterinary care, potentially improving their pet’s health outcomes.

- Peace of Mind: Knowing your pet is protected from unexpected financial burdens provides invaluable peace of mind.

- Long-Term Cost Savings: Over the lifespan of a pet, the total cost of premiums is often less than the potential cost of uninsured veterinary care.

Illustrating Savings and Potential Costs

Choosing low-cost dog insurance can significantly impact your pet’s healthcare expenses. Understanding potential savings and comparing costs across different plans is crucial for making an informed decision. This section will illustrate how low-cost insurance can mitigate unexpected veterinary bills and help you budget effectively for your dog’s health.

A scenario where low-cost insurance proves invaluable is a sudden illness or accident. Imagine your dog, a playful Labrador Retriever named Max, suddenly develops a severe case of gastroenteritis. Without insurance, the emergency visit, diagnostic tests (blood work, X-rays), medication, and hospitalization could easily cost several thousand dollars. With a low-cost plan, a significant portion of these expenses would be covered, reducing your out-of-pocket costs substantially. The specific amount covered would depend on the plan’s deductible, reimbursement percentage, and annual coverage limit.

Hypothetical Dog’s Healthcare Costs and Insurance Coverage

Let’s consider a hypothetical dog, a five-year-old Golden Retriever named Luna, prone to allergies and ear infections. Luna’s annual veterinary care might include routine checkups, allergy medication, ear cleaning, and occasional treatment for minor infections.

Suppose Luna experiences a severe ear infection requiring antibiotics, a specialist consultation, and additional diagnostic tests. The total cost could reach $800. A basic low-cost plan with a $200 deductible and 70% reimbursement would cover $420 (70% of $600, after the deductible). A more comprehensive, but still low-cost, plan with a $100 deductible and 80% reimbursement would cover $560 (80% of $700, after the deductible). A plan with no deductible and 90% reimbursement would cover $720. This illustrates how different levels of coverage significantly affect the final cost to the owner. The difference in out-of-pocket expense between the three plans ranges from $380 to $80.

Comparison of Low-Cost Insurance Plans

The following table compares the monthly premiums and annual coverage limits of three hypothetical low-cost dog insurance plans. Remember that actual premiums and coverage vary significantly between providers and depend on factors like the dog’s breed, age, and location.

| Plan Name | Monthly Premium | Annual Coverage Limit | Deductible |

|---|---|---|---|

| Basic Plan | $25 | $2,000 | $200 |

| Standard Plan | $35 | $5,000 | $100 |

| Comprehensive Plan | $50 | $10,000 | $0 |

Outcome Summary

Ultimately, securing low-cost dog insurance is a strategic investment in your pet’s well-being and your financial stability. By carefully comparing plans, understanding coverage details, and choosing a reputable provider, you can confidently safeguard your canine companion against unexpected veterinary expenses. Remember, proactive planning now can prevent significant financial burdens in the future, allowing you to focus on enjoying the unconditional love and companionship your dog brings.

FAQ Corner

What is the difference between accident-only and comprehensive low-cost dog insurance?

Accident-only plans cover injuries resulting from accidents, while comprehensive plans cover accidents and illnesses. Comprehensive plans are generally more expensive but offer broader protection.

Can I get low-cost dog insurance for a pre-existing condition?

Most low-cost insurers won’t cover pre-existing conditions. However, some may offer coverage after a waiting period, so check the policy details carefully.

How long is the waiting period before coverage begins?

Waiting periods vary by insurer and type of coverage, ranging from a few days to several months. This period usually applies to illnesses, but not always accidents.

What factors influence the cost of my dog’s insurance premiums?

Factors include your dog’s breed, age, location, the level of coverage you choose, and your deductible.

What happens if I change my address or my dog’s health status changes?

You must notify your insurer of any changes to your address or your dog’s health status, as this can affect your premiums or coverage.