Choosing auto insurance can feel like navigating a minefield. Understanding the complex landscape of insurance company ratings is crucial for securing the best coverage at a fair price. This guide unravels the intricacies of auto insurance ratings, empowering you to make informed decisions based on a clear understanding of various rating systems and their implications for your financial well-being.

From deciphering financial strength ratings to understanding the nuances of claims handling assessments, we’ll explore the key factors influencing these ratings and how they directly impact your experience as a policyholder. We’ll also delve into the process of finding reliable rating sources and interpreting the information effectively, equipping you with the knowledge to confidently compare insurers and choose the right policy for your needs.

Understanding Auto Insurance Ratings

Auto insurance ratings are crucial for consumers seeking reliable and financially sound insurance providers. These ratings, provided by independent rating agencies, assess the financial strength and operational stability of insurance companies. Understanding these ratings empowers consumers to make informed decisions when choosing an insurer.

Factors Influencing Auto Insurance Ratings

Several key factors contribute to an insurance company’s rating. Financial strength, as measured by reserves, surplus, and underwriting performance, is paramount. Claims paying ability, the insurer’s capacity to promptly settle claims, is another critical element. The company’s management quality, including its operational efficiency and strategic planning, also significantly impacts its rating. Furthermore, the insurer’s investment portfolio and its overall business profile, including its market share and geographic diversification, play a role in the assessment. Finally, the rating agencies also consider the company’s legal and regulatory compliance.

Rating Agency Methodology

Rating agencies employ a rigorous methodology to evaluate insurance companies. This typically involves a comprehensive review of the insurer’s financial statements, including balance sheets, income statements, and cash flow statements. Analysts examine key financial ratios and metrics to assess the company’s profitability, liquidity, and solvency. They also conduct on-site visits and interviews with company management to gather qualitative information about the insurer’s operations and risk management practices. The agencies use sophisticated quantitative models to incorporate various factors into a holistic assessment of the company’s financial strength and creditworthiness. The final rating reflects the agency’s overall judgment of the insurer’s ability to meet its obligations to policyholders.

Impact of Ratings on Consumers

Auto insurance ratings directly impact consumers in several ways. Higher ratings from reputable agencies generally indicate a lower risk of the insurer failing to pay claims. Consumers are more likely to choose highly-rated companies, ensuring greater peace of mind. These ratings also influence the pricing of insurance policies. Insurers with strong ratings often secure better reinsurance terms, leading to potentially lower premiums for consumers. Conversely, insurers with lower ratings may face higher reinsurance costs, potentially resulting in increased premiums for their policyholders. Furthermore, some financial institutions might consider an insurer’s rating when deciding whether to offer financing or other services to the company, indirectly affecting the insurer’s ability to offer competitive policies.

Comparison of Top Rating Agencies

The following table compares five leading rating agencies and their rating scales. Note that specific rating scales and interpretations can vary slightly between agencies.

| Rating Agency | Highest Rating | Lowest Rating | Rating Scale Description |

|---|---|---|---|

| A.M. Best | A++ (Superior) | D (In Liquidation) | Ranges from A++ to F, reflecting financial strength and creditworthiness. |

| Moody’s | Aaa | Caa | Uses a letter grade system with modifiers (+ and -) to indicate varying levels of creditworthiness. |

| Standard & Poor’s (S&P) | AAA | D | Similar to Moody’s, employs a letter grade system with modifiers. |

| Fitch Ratings | AAA | D | Utilizes a letter grade system with modifiers, reflecting creditworthiness. |

| Weiss Ratings | A+ | E | Employs a letter grade system with modifiers, focusing on financial strength and operational efficiency. |

Types of Auto Insurance Ratings

Choosing the right auto insurance policy can feel overwhelming, but understanding the different ways insurance companies are rated is crucial for making an informed decision. Various organizations assess insurers across several key areas, providing consumers with valuable insights into their reliability and performance. These ratings help you compare companies and choose one that best suits your needs and risk tolerance.

Several types of ratings exist, each offering a different perspective on an insurance company’s capabilities and trustworthiness. These ratings are not always directly comparable, as they focus on different aspects of the insurance business. However, taken together, they paint a more complete picture.

Financial Strength Ratings

Financial strength ratings assess an insurer’s ability to pay claims. These ratings, typically issued by independent rating agencies like A.M. Best, Moody’s, Standard & Poor’s, and Fitch, evaluate the company’s financial stability, including its reserves, investment performance, and overall financial health. A high financial strength rating indicates a lower risk of the insurer becoming insolvent and failing to meet its obligations to policyholders. For example, an A++ rating generally suggests exceptional financial strength, while a lower rating, like a B+, might signal some concerns. Consumers should prioritize insurers with strong financial strength ratings to ensure their claims are paid even in challenging economic times.

Claims Handling Ratings

Claims handling ratings focus on how efficiently and fairly an insurance company processes claims. These ratings are often based on customer surveys and feedback, evaluating aspects like ease of filing a claim, speed of processing, and overall customer satisfaction with the claims process. While not all rating agencies provide specific claims handling scores, many customer review sites and surveys offer insights into an insurer’s claims handling performance. A positive experience with claims handling can be critical in a time of need, significantly impacting the overall customer experience. For instance, a company with a high average customer satisfaction rating in claims handling may indicate a smoother and less stressful experience should you need to file a claim.

Customer Satisfaction Ratings

Customer satisfaction ratings measure overall customer happiness with an insurance company. These ratings, frequently provided by J.D. Power, consider factors like customer service responsiveness, policy clarity, and the overall ease of doing business with the insurer. High customer satisfaction ratings suggest a positive experience, including prompt responses to inquiries, clear communication, and a generally positive relationship with the company. These ratings can provide a valuable perspective, offering insights beyond financial stability and claims processing efficiency. For example, a company with consistently high customer satisfaction scores may indicate a better overall experience, even if their financial strength rating isn’t the highest.

Interpreting Auto Insurance Ratings

Understanding auto insurance ratings can be surprisingly complex, even for seasoned consumers. The sheer volume of rating agencies, the varying methodologies they employ, and the nuanced way ratings are presented all contribute to consumer confusion. This section aims to clarify the process of interpreting these ratings and empower consumers to make informed decisions.

Challenges in Interpreting Auto Insurance Ratings

Consumers often struggle with deciphering auto insurance ratings due to several factors. Different rating agencies use different scoring systems and weighting methodologies, making direct comparisons difficult. Furthermore, ratings may focus on different aspects of an insurer’s performance, such as financial strength, customer satisfaction, or claims handling efficiency. The lack of standardization and the technical nature of the rating reports can also be overwhelming for the average consumer. Finally, the subtle differences between ratings can be hard to interpret, leading to misinterpretations and potentially poor choices.

Tips for Understanding and Comparing Ratings from Different Sources

When comparing auto insurance ratings, it’s crucial to consider the source’s methodology. Look for detailed explanations of how the ratings are calculated, the factors considered, and the weighting given to each factor. Compare ratings from multiple reputable sources to get a more comprehensive picture. Don’t rely solely on a single rating; consider it one piece of the puzzle. Pay close attention to the date of the rating, as financial strength and performance can change over time. Finally, remember that ratings are just one factor to consider when choosing an insurer; customer service, policy features, and price also play important roles.

A Simple Guide for Evaluating Auto Insurance Ratings

To effectively evaluate auto insurance ratings, follow these steps:

- Identify Reputable Rating Agencies: Focus on well-established and widely respected agencies such as AM Best, Moody’s, Standard & Poor’s, and Fitch Ratings. These agencies have rigorous methodologies and a long history of evaluating insurance companies.

- Understand the Rating Scales: Each agency uses its own rating scale, typically ranging from excellent to poor. Familiarize yourself with the specific meanings of each rating level within each agency’s system. For example, AM Best uses letter grades (A++, A+, A, etc.), while others may use numerical scores.

- Compare Ratings Across Multiple Sources: Don’t rely on a single rating. Check ratings from at least two or three reputable agencies to get a broader perspective on the insurer’s financial stability and performance.

- Consider the Rating’s Focus: Note whether the rating focuses on financial strength, customer satisfaction, or claims handling. A high rating in one area doesn’t necessarily guarantee a high rating in others.

- Check the Rating Date: Ensure the ratings you are reviewing are current. Insurance company performance can change, so older ratings may not reflect the current situation.

Interpreting Specific Rating Scores and Their Implications

Let’s consider a hypothetical example. Suppose Company A receives an A+ rating from AM Best and a AA- rating from Standard & Poor’s. Both ratings indicate strong financial stability. However, the slight difference might suggest that Standard & Poor’s assesses Company A as having a marginally higher level of financial strength than AM Best. Conversely, if a company receives a lower rating, such as a B+ from AM Best, it might indicate a higher risk of financial instability and potential difficulty paying claims. This would likely influence your decision-making process; you might choose to seek out an insurer with higher ratings for greater peace of mind. Always remember to consider the complete picture and compare across multiple sources.

Impact of Ratings on Consumers

Auto insurance ratings significantly influence consumers’ choices and experiences. Understanding how these ratings affect premium costs, claims processing, and overall trust is crucial for making informed decisions. This section will explore the direct impact of insurance company ratings on the average consumer.

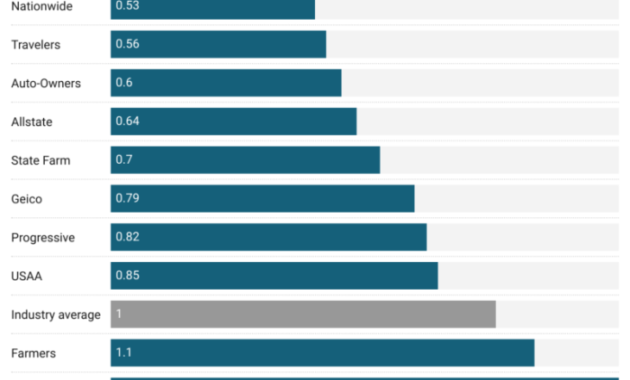

Ratings directly impact the cost of auto insurance premiums. Companies with higher ratings, reflecting financial stability and efficient claims handling, often offer lower premiums. This is because insurers with strong ratings are perceived as less risky, meaning there’s a lower probability of them failing to pay out claims. Conversely, insurers with lower ratings may charge higher premiums to offset their increased risk profile. This difference can be substantial, potentially saving or costing hundreds of dollars annually depending on the rating and the individual’s risk profile.

Premium Cost Variations Based on Ratings

Insurers use a variety of factors to calculate premiums, including driving history, age, location, and the type of vehicle. However, the insurer’s financial strength rating is a significant component. A hypothetical example illustrates this: Consider two drivers with identical profiles. Driver A chooses an insurer with a high rating (e.g., A++), while Driver B chooses an insurer with a low rating (e.g., B-). Driver A is likely to receive a lower premium than Driver B, even though their risk profiles are identical. The difference reflects the market’s assessment of the insurers’ financial stability and ability to pay claims. This difference can range from a few percentage points to a significant amount depending on the specific rating agencies and the insurers involved.

Claims Payment Likelihood and Ratings

A high rating generally indicates a higher likelihood of claims being paid promptly and fairly. Insurers with strong financial ratings have the resources and established processes to handle claims efficiently. Conversely, insurers with low ratings may experience delays in processing claims or may be less likely to pay out claims in full, particularly in complex or disputed cases. This can lead to significant financial hardship for consumers involved in accidents. For instance, a consumer with a significant injury claim might face prolonged legal battles and financial strain if their insurer has a history of slow or unfair claims handling, often associated with lower ratings.

Consumer Trust and Confidence

Auto insurance ratings significantly impact consumer trust and confidence. Consumers are more likely to trust and choose insurers with high ratings, perceiving them as reliable and financially secure. This trust translates into a willingness to pay premiums and maintain a long-term relationship with the insurer. Conversely, low ratings can erode consumer trust, leading to hesitation in choosing the insurer, even if the premiums are lower. The potential for delayed or denied claims outweighs the perceived cost savings for many consumers. This effect is particularly pronounced for large claims, where the financial implications are more significant.

Impact of High vs. Low Ratings on Consumer Choices

The following text-based illustration depicts the contrasting choices consumers might make:

High Rating Insurer (A++): Premium: $1200/year; Claims Handling: Fast and Fair; Consumer Perception: High Trust and Confidence; Choice Likelihood: High.

Low Rating Insurer (B-): Premium: $1000/year; Claims Handling: Slow and Potentially Unfair; Consumer Perception: Low Trust and Distrust; Choice Likelihood: Low.

This simple comparison demonstrates how the perceived value, considering both premium and the likelihood of a fair claims process, heavily influences consumer decisions, even when a lower premium is offered by a poorly rated insurer.

Finding and Using Auto Insurance Ratings

Navigating the world of auto insurance can feel overwhelming, especially when trying to decipher the various ratings assigned to different companies. Understanding how to find and interpret these ratings is crucial for making informed decisions and securing the best possible coverage at a fair price. This section will guide you through the process of locating reliable sources, comparing ratings, and ultimately using this information to your advantage.

Reliable Sources for Auto Insurance Ratings

Several reputable organizations provide independent ratings of auto insurance companies. These ratings assess factors like financial strength, customer satisfaction, and claims handling. Relying on multiple sources offers a more comprehensive view than relying on a single rating. Key sources include AM Best, Moody’s, Standard & Poor’s, and J.D. Power. Each source employs different methodologies, so comparing ratings across multiple sources provides a more balanced perspective. For example, AM Best focuses heavily on financial stability, while J.D. Power emphasizes customer satisfaction.

Searching and Comparing Auto Insurance Ratings

The process of finding and comparing ratings typically involves visiting the websites of the rating agencies mentioned above. Most offer searchable databases allowing you to look up specific insurance companies. Pay close attention to the rating scale used by each agency; they may not all use the same system. For instance, AM Best uses letter ratings (A++, A+, etc.), while others might use numerical scores. Directly comparing ratings across different scales requires careful consideration of each agency’s rating criteria. It’s beneficial to create a spreadsheet to organize the information gathered from different sources, enabling a side-by-side comparison of ratings for several companies.

Strategies for Effective Use of Ratings

Using insurance ratings effectively involves more than simply looking at the highest number or letter grade. Consider the specific aspects of each rating. For example, a high financial strength rating indicates the company is unlikely to go bankrupt, ensuring your claims will be paid. A high customer satisfaction rating suggests a positive experience with claims processing and customer service. However, remember that ratings are just one piece of the puzzle. You should also consider factors such as price, coverage options, and the company’s reputation in your specific area. Don’t solely rely on ratings; use them in conjunction with other research methods, such as reading online reviews and comparing quotes from multiple insurers.

Auto Insurance Rating Sources

The following table summarizes key sources for auto insurance ratings, highlighting their rating types, accessibility, and reliability. Note that reliability is subjective and depends on individual needs and priorities.

| Source | Rating Type | Accessibility | Reliability |

|---|---|---|---|

| AM Best | Financial Strength Ratings (Letter Grades) | Website; subscription for detailed reports | High; widely respected in the insurance industry |

| Moody’s | Financial Strength Ratings (Numerical Scores) | Website; subscription for detailed reports | High; another major credit rating agency |

| Standard & Poor’s | Financial Strength Ratings (Letter Grades) | Website; subscription for detailed reports | High; another major credit rating agency |

| J.D. Power | Customer Satisfaction Ratings (Numerical Scores) | Website; some reports may require purchase | High; focuses on customer experience |

Beyond Numerical Ratings

While numerical ratings provide a convenient snapshot of an auto insurance company’s performance, they don’t tell the whole story. A comprehensive assessment requires looking beyond the numbers and considering other crucial factors that can significantly impact your experience. A high numerical rating doesn’t guarantee a positive experience, and a lower rating doesn’t automatically mean poor service.

Customer reviews and testimonials offer invaluable insights into the actual experiences of policyholders. They provide a more nuanced perspective than numerical scores alone, revealing aspects like the responsiveness of customer service, the ease of filing a claim, and the overall fairness of claim settlements. These qualitative factors can be just as, if not more, important than the numerical rating itself.

The Importance of Customer Reviews and Testimonials

Customer reviews act as a powerful form of social proof. They provide firsthand accounts of interactions with the insurance company, covering a wide range of experiences, from initial policy acquisition to claim resolution. Reading multiple reviews can help identify patterns and trends, giving you a clearer picture of the company’s strengths and weaknesses. For instance, consistently positive reviews regarding claim handling suggest a company that prioritizes its customers’ needs during difficult times. Conversely, a high volume of negative reviews about slow claim processing or unresponsive customer service should raise significant concerns, regardless of the numerical rating.

Non-Numerical Indicators of a Good Insurance Company

Several non-numerical factors signal a reliable and customer-focused auto insurance company. A strong financial stability rating from a reputable agency like A.M. Best demonstrates the company’s ability to pay out claims even during challenging economic periods. This is crucial; a company with shaky finances might struggle to meet its obligations when you need them most. Another important factor is the availability of various communication channels – easy access to customer service via phone, email, and online chat – indicates a commitment to customer convenience and accessibility. Furthermore, a transparent and easily understandable policy document, devoid of confusing jargon, suggests a company that prioritizes clear communication with its customers. Finally, the availability of additional services, such as roadside assistance or accident forgiveness programs, can add significant value beyond the basic coverage.

Incorporating Qualitative Information into the Decision-Making Process

To make an informed decision, you should integrate both numerical ratings and qualitative information. Start by researching numerical ratings from reputable sources. Then, delve into customer reviews on sites like Yelp, Google Reviews, and the Better Business Bureau. Look for recurring themes and patterns in the reviews. Do many customers praise the company’s responsiveness? Are there frequent complaints about specific aspects of the service? By carefully analyzing both the numerical scores and the qualitative feedback, you can create a well-rounded picture of the insurance company and choose the one that best aligns with your needs and expectations. For example, a company with a slightly lower numerical rating but consistently positive customer reviews about claim handling might be a better choice than a company with a higher numerical rating but numerous complaints about slow or unhelpful customer service.

Last Word

Ultimately, understanding auto insurance ratings is not just about finding the cheapest policy; it’s about securing financial protection and peace of mind. By diligently researching and comparing ratings from various reputable sources, and by considering both quantitative and qualitative factors, you can confidently choose an insurer that aligns with your risk tolerance and financial priorities. Remember, informed decisions lead to better outcomes – and in the world of auto insurance, that translates to significant savings and a more secure future.

Popular Questions

What happens if my insurer’s rating drops significantly?

A significant drop in an insurer’s rating may indicate increased financial instability or problems with claims handling. You might consider shopping for a new policy with a more highly-rated insurer to protect yourself.

Are customer satisfaction ratings as important as financial strength ratings?

Both are crucial. Financial strength ensures the insurer can pay claims, while customer satisfaction reflects the quality of service you can expect. A good balance is ideal.

How often are auto insurance ratings updated?

The frequency varies by rating agency. Some update ratings annually, others more frequently, depending on the insurer’s performance and available data.

Can I find ratings for smaller, regional insurance companies?

While major national insurers are more likely to be rated by multiple agencies, you might still find ratings for some smaller companies through specialized sources or state insurance departments.

На этом сайте у вас есть возможность приобрести виртуальные телефонные номера различных операторов. Они могут использоваться для подтверждения аккаунтов в различных сервисах и приложениях.

В каталоге доступны как постоянные, так и временные номера, что можно использовать чтобы принять сообщений. Это простое решение для тех, кто не желает указывать основной номер в интернете.

аренда номера для смс

Оформление заказа максимально удобный: определяетесь с подходящий номер, вносите оплату, и он будет доступен. Оцените сервис уже сегодня!