Navigating the world of auto insurance can feel like deciphering a complex code. Understanding what your policy covers is crucial, not only for financial protection but also for peace of mind. This guide unravels the intricacies of auto insurance, explaining the core coverages, optional add-ons, and factors influencing your premiums. We’ll explore everything from liability and collision coverage to the often-overlooked uninsured/underinsured motorist protection, empowering you to make informed decisions about your insurance needs.

From the basics of liability coverage to the nuances of collision and comprehensive protection, we’ll break down the key components of a standard auto insurance policy. We’ll also delve into optional add-ons that can enhance your coverage and discuss the factors that affect your premium costs, such as your driving history and credit score. Ultimately, this guide aims to equip you with the knowledge necessary to choose the right policy for your individual circumstances.

Basic Auto Insurance Coverage

Understanding the core components of your auto insurance policy is crucial for protecting yourself financially in the event of an accident. A standard policy typically includes several key coverages designed to address various scenarios. This section will break down the fundamental aspects of basic auto insurance.

Liability Coverage

Liability coverage is arguably the most important part of your auto insurance policy. It protects you financially if you cause an accident that results in injuries to others or damage to their property. This coverage pays for the medical expenses, lost wages, and other damages incurred by the other party, not your own. It’s vital to understand that liability coverage only covers the other person’s losses, not yours.

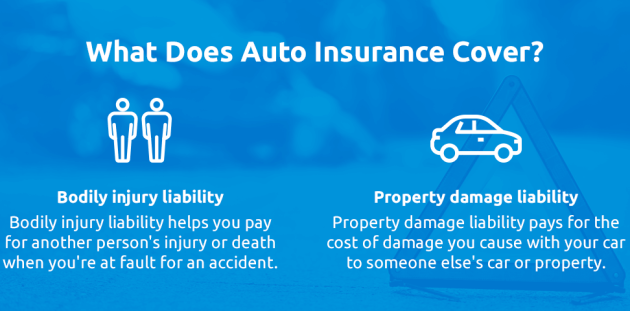

Bodily Injury and Property Damage

Liability coverage is further divided into two main components: bodily injury liability and property damage liability. Bodily injury liability covers medical bills, lost wages, and pain and suffering for individuals injured in an accident you caused. Property damage liability covers the cost of repairing or replacing the other person’s vehicle or other property damaged in the accident.

Liability Coverage Limits

Liability coverage limits are expressed as numerical values, typically represented as three numbers: for example, 25/50/25. This means:

- $25,000 is the maximum amount the insurance company will pay for bodily injury to one person in an accident.

- $50,000 is the maximum amount the insurance company will pay for total bodily injury to all people involved in the accident.

- $25,000 is the maximum amount the insurance company will pay for damage to property in an accident.

It’s important to choose coverage limits that adequately protect you, considering the potential costs of serious accidents. Higher limits offer greater protection but usually come with higher premiums. Failing to have sufficient liability coverage could leave you personally responsible for significant financial liabilities.

Liability Coverage Levels and Estimated Premiums

The cost of auto insurance varies widely based on several factors, including your driving record, location, and the type of vehicle you drive. However, the following table provides a general illustration of how liability coverage limits and premiums might relate. These are estimates and actual costs may differ significantly.

| Coverage Level | Bodily Injury Limit | Property Damage Limit | Estimated Premium (Annual) |

|---|---|---|---|

| Low | 25/50/25 | $25,000 | $500 – $700 |

| Medium | 100/300/100 | $100,000 | $700 – $900 |

| High | 250/500/250 | $250,000 | $900 – $1200 |

| Very High | 500/1000/500 | $500,000 | $1200 – $1500+ |

Collision and Comprehensive Coverage

Collision and comprehensive coverage represent two crucial components of many auto insurance policies, offering protection against different types of vehicle damage. Understanding their distinctions is key to selecting the right coverage for your individual needs and risk tolerance. Both coverages are optional, meaning they are not always required by law, but they can significantly reduce your financial burden in the event of an accident or unforeseen damage.

Collision and comprehensive coverage protect your vehicle from various incidents, but they differ significantly in what they cover. Collision coverage protects your car against damage resulting from a collision with another vehicle or object, such as a tree or a building. Comprehensive coverage, on the other hand, covers damage caused by events other than collisions, encompassing a broader range of incidents.

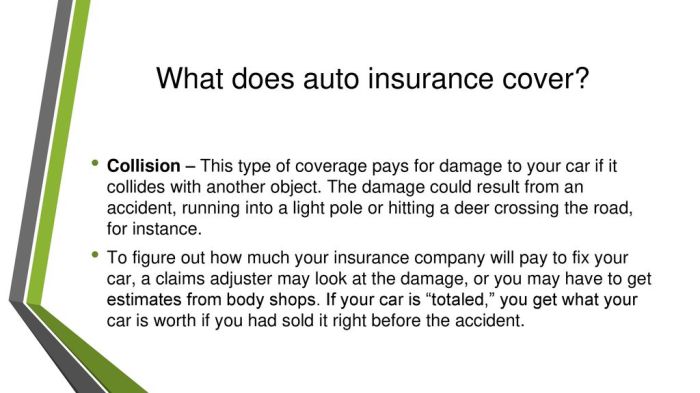

Collision Coverage Details

Collision coverage reimburses you for damage to your vehicle caused by an impact with another vehicle or object, regardless of who is at fault. This includes incidents like fender benders, rollovers, and hitting a stationary object. For example, if you rear-end another car, or if a deer runs into your vehicle, collision coverage will typically pay for the repairs or replacement of your vehicle, less your deductible. The amount paid will depend on the extent of the damage and your policy limits. Note that collision coverage usually doesn’t cover injuries to you or others involved in the accident; that’s what liability coverage is for.

Comprehensive Coverage Details

Comprehensive coverage protects your vehicle against damage from events not involving a collision. This includes a wide variety of scenarios such as theft, vandalism, fire, hail, flood, and even damage from animals. For instance, if your car is stolen and recovered damaged, or if a tree falls on your car during a storm, comprehensive coverage will typically cover the repair or replacement costs, again less your deductible. Unlike collision coverage, comprehensive coverage is typically less expensive, reflecting the lower likelihood of these events compared to collisions.

Deductibles for Collision and Comprehensive Claims

Both collision and comprehensive coverage involve deductibles. A deductible is the amount you pay out-of-pocket before your insurance company begins to cover the remaining costs of repairs or replacement. Deductibles can range from a few hundred dollars to several thousand dollars. A higher deductible typically results in lower monthly premiums, while a lower deductible leads to higher premiums. Choosing the right deductible involves balancing the monthly savings with the potential out-of-pocket expense in case of a claim.

Deductible Amount Comparison

The following table illustrates the potential trade-offs between choosing a higher or lower deductible for collision and comprehensive coverage:

| Deductible Amount | Monthly Premium Savings | Out-of-Pocket Expense in a Claim | Overall Cost Savings |

|---|---|---|---|

| $250 | $0 (or minimal) | $250 | Potentially negative if no claims |

| $500 | $5-$15 (example) | $500 | Potentially positive if no claims, or only minor claims |

| $1000 | $10-$30 (example) | $1000 | Potentially very positive if no claims, or only minor claims |

| $2500 | $20-$50 (example) | $2500 | Potentially highly positive if no claims, or only minor claims |

Note: The monthly premium savings and overall cost savings are illustrative examples and will vary depending on factors such as your driving record, location, vehicle type, and insurance company. The actual figures might differ significantly.

Uninsured/Underinsured Motorist Coverage

Uninsured/underinsured motorist (UM/UIM) coverage is a crucial addition to your auto insurance policy, offering vital protection in situations where you’re involved in an accident caused by a driver who lacks sufficient insurance or is uninsured altogether. This coverage safeguards you and your passengers from significant financial burdens that can arise from medical bills, property damage, lost wages, and other expenses.

This coverage acts as a safety net, stepping in to compensate you for your losses even when the at-fault driver is unable to cover the damages. Your own UM/UIM policy will cover your medical expenses, lost wages, and vehicle repairs, up to your policy limits, regardless of who caused the accident. It essentially ensures that you are not left financially vulnerable due to another driver’s negligence or lack of insurance.

Scenarios Benefiting from UM/UIM Coverage

Several scenarios highlight the critical role of UM/UIM coverage. Imagine being involved in an accident with a hit-and-run driver who flees the scene. Your medical bills alone could easily exceed tens of thousands of dollars. Without UM/UIM coverage, you would be solely responsible for these costs. Similarly, consider a collision with a driver whose liability coverage is far below the actual cost of your injuries and vehicle repairs. UM/UIM coverage would bridge that gap, ensuring you receive the compensation you deserve. Another example is an accident where you are seriously injured by an underinsured driver. Their insurance might only cover a fraction of your medical bills and lost wages, but your UM/UIM coverage will make up the difference, preventing financial ruin.

Importance of Sufficient UM/UIM Coverage

The importance of adequate UM/UIM coverage cannot be overstated. Consider these points:

- Protection from High Medical Costs: Medical expenses, especially after serious accidents, can be astronomical. UM/UIM coverage helps cover these costs.

- Compensation for Lost Wages: If you are unable to work due to injuries sustained in an accident, UM/UIM coverage can help replace lost income.

- Vehicle Repair or Replacement Costs: Repairing or replacing a damaged vehicle can be expensive. UM/UIM coverage can help cover these costs even if the at-fault driver is uninsured or underinsured.

- Legal Fees: If you need to pursue legal action against the at-fault driver, UM/UIM coverage can help cover associated legal fees.

- Peace of Mind: Knowing you have sufficient UM/UIM coverage provides significant peace of mind, knowing you’re protected in unforeseen circumstances.

Final Wrap-Up

Securing adequate auto insurance is a vital step in responsible vehicle ownership. By understanding the various coverage options, their limitations, and the factors affecting premiums, you can confidently select a policy that aligns with your needs and budget. Remember to regularly review your policy and don’t hesitate to contact your insurer with any questions or to make necessary adjustments. Proactive insurance management can provide significant financial security and peace of mind on the road.

FAQ Summary

What happens if I’m in an accident and the other driver is at fault but uninsured?

Uninsured/Underinsured Motorist coverage protects you in such scenarios, covering your medical bills and vehicle repairs.

Can I choose my own repair shop after an accident?

Often, yes. However, your insurance company may have preferred shops or a process for approvals. Check your policy details.

How often can I expect my auto insurance rates to change?

Rates can change annually, or even more frequently depending on your insurer and any changes in your driving record or risk profile.

What is the difference between a claim and a quote?

A quote is an estimate of your insurance cost before you have a policy. A claim is a formal request for payment after an accident or covered incident.

Does my auto insurance cover damage to my car if it’s parked and vandalized?

Comprehensive coverage typically covers damage from vandalism, theft, and other non-collision events.