The cost of car insurance can vary dramatically, leaving many drivers wondering how to find the cheapest options without sacrificing necessary coverage. Factors like age, driving history, vehicle type, and location all play a significant role in determining your premium. This guide delves into the intricacies of car insurance pricing, offering strategies to help you secure affordable yet adequate protection for your vehicle.

Understanding the nuances of car insurance policies is crucial for making informed decisions. This guide explores various coverage levels, explains the impact of different factors on your rates, and provides actionable steps to compare quotes and potentially negotiate lower premiums. Ultimately, our goal is to empower you to navigate the world of car insurance with confidence and find a policy that fits both your budget and your needs.

Factors Affecting Car Insurance Costs

Several key factors significantly influence the price of car insurance. Understanding these factors can help you make informed decisions and potentially save money on your premiums. These factors interact in complex ways, so a single change can have a ripple effect on your overall cost.

Age and Driving History

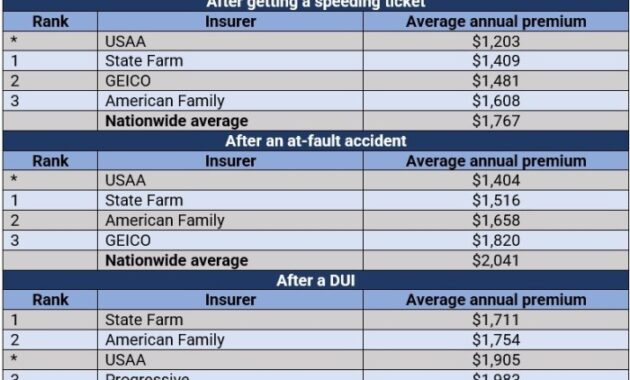

Age is a significant factor in determining insurance premiums. Younger drivers, particularly those under 25, generally pay higher rates due to statistically higher accident rates within this demographic. Insurance companies perceive them as higher risk. Conversely, older drivers, typically over 65, may also see increased premiums, though often for different reasons, such as potential health concerns impacting driving ability. Driving history plays a crucial role; a clean driving record with no accidents or traffic violations results in lower premiums. Conversely, accidents, speeding tickets, or DUI convictions significantly increase premiums, often for several years following the incident. The severity of the offense directly correlates with the premium increase. For example, a minor fender bender will impact premiums less than a serious accident involving injury or property damage.

Vehicle Type

The type of vehicle you drive directly impacts your insurance costs. Sports cars, luxury vehicles, and high-performance cars are generally more expensive to insure due to higher repair costs, greater potential for theft, and a higher risk of accidents. These vehicles often command higher premiums due to their higher value and the associated repair expenses. Conversely, smaller, less expensive vehicles typically attract lower premiums. Factors such as safety ratings and anti-theft features also influence the cost; vehicles with advanced safety technology and robust anti-theft systems may qualify for discounts.

Coverage Levels

Insurance coverage levels significantly affect premiums. Liability coverage, which pays for damages to others in an accident you cause, is typically the most basic and cheapest option. Collision coverage, which pays for damage to your vehicle regardless of fault, and comprehensive coverage, which covers damage from non-collision events (e.g., theft, vandalism, hail), are additional coverages that increase premiums. A higher coverage limit for liability increases your premium, as it reflects a greater potential payout by the insurance company. Similarly, choosing comprehensive and collision coverage adds to the cost, but offers broader protection. The decision of which coverage levels to choose involves balancing cost with the level of risk you’re willing to accept.

Location

Geographic location heavily influences car insurance rates. Insurance companies assess risk based on factors such as accident rates, crime rates, and the cost of vehicle repairs in specific areas. Urban areas with high traffic density and higher crime rates tend to have higher insurance premiums compared to rural areas with lower accident rates. State regulations also play a significant role; states with mandatory insurance requirements or stricter regulations might lead to higher premiums.

| City | State | Average Annual Premium (Liability Only) | Average Annual Premium (Liability + Collision + Comprehensive) |

|---|---|---|---|

| New York City | NY | $1200 | $2500 |

| Los Angeles | CA | $1000 | $2200 |

| Chicago | IL | $900 | $2000 |

| Houston | TX | $700 | $1500 |

Finding the Cheapest Rates

Securing the most affordable car insurance involves a strategic approach to comparing quotes and leveraging available discounts. This requires understanding how different insurers calculate premiums and actively seeking out the best deals. By employing the techniques Artikeld below, you can significantly reduce your insurance costs.

Finding the lowest car insurance rates involves a multi-pronged approach. This includes actively comparing quotes from multiple providers, utilizing online comparison tools effectively, and identifying and applying all eligible discounts. Remember, insurance premiums are not static; they vary widely based on individual circumstances and the specific insurer.

Comparing Insurance Quotes

To effectively compare quotes, gather information about your vehicle, driving history, and desired coverage. Then, request quotes from at least three to five different insurance providers. Don’t just focus on the initial price; carefully examine the policy details, including deductibles and coverage limits, to ensure you’re comparing apples to apples. Note any differences in coverage before making a decision based solely on price. Keep a spreadsheet to track your quotes, noting each insurer’s price and the specifics of their policy. This will allow for a clear comparison of value, not just cost.

Using Online Comparison Tools

Online comparison tools offer a convenient way to gather multiple quotes simultaneously. The benefit is the speed and efficiency of obtaining numerous quotes in a short time. However, these tools may not always present every insurer available in your area, and the displayed rates might be estimates rather than firm quotes. Always verify the information provided by these tools by contacting the insurers directly to confirm the quoted price and policy details. Be aware that some comparison sites may prioritize insurers who pay them referral fees, potentially skewing the results.

Available Discounts

Many insurers offer a variety of discounts to lower premiums. These can include good student discounts (often requiring a certain GPA), safe driver discounts (based on a clean driving record and lack of accidents or violations), and discounts for bundling home and auto insurance with the same provider. Other potential discounts include those for anti-theft devices, driver training courses, and even affiliations with certain employers or organizations. Contact insurers directly to inquire about all potential discounts you may qualify for. Proactively providing documentation, such as proof of good grades or a defensive driving certificate, can expedite the discount application process.

Obtaining Car Insurance Quotes: A Step-by-Step Guide

- Gather Necessary Information: Compile your driver’s license information, vehicle information (year, make, model, VIN), address, and driving history (including accidents and violations).

- Choose Insurance Providers: Select at least three to five different insurance providers to compare quotes from. Consider a mix of large national insurers and smaller regional companies.

- Request Quotes: Contact each provider either online or by phone to request a quote. Be prepared to answer questions about your driving history and vehicle.

- Compare Quotes: Carefully review each quote, paying close attention to coverage details, deductibles, and premiums. Use a spreadsheet to organize the information for easy comparison.

- Verify Information: Confirm the accuracy of the quotes with each provider before making a decision. Ensure the coverage meets your needs.

- Select a Policy: Choose the policy that best balances cost and coverage, based on your individual needs and risk tolerance.

- Purchase the Policy: Complete the application process and make the necessary payments to activate your policy.

Understanding Insurance Policies

Choosing the cheapest car insurance is only half the battle; understanding what your policy covers is equally crucial. A comprehensive understanding of your policy’s components ensures you’re adequately protected and avoid unexpected costs in the event of an accident or other incident. This section will break down the key elements of a standard car insurance policy, clarifying the differences between various coverage types and highlighting common exclusions.

Key Components of a Standard Car Insurance Policy

A standard car insurance policy typically includes several key components designed to protect you financially in different scenarios. These components often involve a combination of liability coverage, collision coverage, comprehensive coverage, and uninsured/underinsured motorist coverage. The specific components and their limits will vary depending on your chosen policy and state regulations. Premiums are calculated based on a combination of these coverage types, your driving record, vehicle details, and location.

Liability Coverage vs. Collision Coverage

Liability coverage protects you financially if you cause an accident that results in injury or damage to another person or their property. It covers the costs of medical bills, property repairs, and legal fees for the other party. Collision coverage, on the other hand, protects your own vehicle in the event of an accident, regardless of who is at fault. This means your insurer will pay for repairs or replacement of your vehicle, even if you caused the accident.

Examples of Coverage Necessity

Consider this scenario: You rear-end another car, causing significant damage to their vehicle and injuring the driver. Your liability coverage would pay for the other driver’s medical bills and vehicle repairs. However, if your car also sustained damage, your collision coverage would take care of those repair costs. Conversely, if a tree falls on your parked car during a storm, your comprehensive coverage (often a part of a standard policy, but sometimes sold separately) would cover the damage, as this wasn’t caused by a collision. If an uninsured driver hits your car, your uninsured/underinsured motorist coverage will help pay for the damages to your vehicle and your medical expenses.

Common Policy Exclusions

It’s important to understand what your policy *doesn’t* cover. Understanding these exclusions can prevent unexpected out-of-pocket expenses.

- Damage caused by wear and tear: Normal wear and tear on your vehicle, such as tire wear or brake pad replacement, is typically not covered.

- Damage from intentional acts: If you deliberately damage your car, your insurance likely won’t cover the repairs.

- Damage from driving under the influence: Driving under the influence of alcohol or drugs often voids your coverage.

- Damage caused by racing or other illegal activities: Participating in illegal activities such as street racing will likely result in your claim being denied.

- Damage resulting from lack of proper maintenance: Failure to maintain your vehicle properly (e.g., neglecting necessary repairs) might affect coverage for related issues.

Saving Money on Car Insurance

Securing affordable car insurance is a significant financial consideration for most drivers. Numerous strategies exist to reduce premiums, allowing you to keep more money in your pocket while maintaining adequate coverage. By understanding these strategies and implementing them effectively, you can significantly lower your annual insurance costs.

Methods for Reducing Insurance Premiums

Several effective methods can significantly reduce your car insurance premiums. These strategies often involve lifestyle adjustments, careful policy selection, and proactive engagement with your insurance provider.

- Bundle your insurance policies: Many insurance companies offer discounts for bundling home, auto, and other insurance policies. This often results in substantial savings compared to purchasing each policy separately.

- Shop around and compare quotes: Don’t settle for the first quote you receive. Obtain quotes from multiple insurers to compare coverage options and pricing. Online comparison tools can streamline this process.

- Maintain a good driving record: A clean driving record, free of accidents and traffic violations, is a major factor in determining your insurance premium. Safe driving habits directly translate to lower costs.

- Increase your deductible: Choosing a higher deductible will generally lower your premium. However, carefully weigh the cost savings against your ability to afford a larger out-of-pocket expense in case of an accident.

- Consider safety features: Cars equipped with advanced safety features, such as anti-theft systems, airbags, and anti-lock brakes, often qualify for discounts.

- Take a defensive driving course: Completing a defensive driving course can demonstrate your commitment to safe driving and often results in premium reductions.

Cost-Effectiveness of Different Driving Habits

Driving habits significantly impact insurance costs. Reducing mileage, for instance, can lead to lower premiums as insurers often base rates partly on annual mileage. Similarly, avoiding risky driving behaviors, such as speeding or aggressive driving, directly correlates with lower premiums.

- Reduced Mileage: If you can reduce your annual driving distance, many insurers offer discounts for lower mileage drivers. For example, someone who commutes less or works from home might qualify for a significant reduction in their premium. This is often achieved through telematics programs that track driving habits.

- Safe Driving Practices: Maintaining a safe driving record significantly impacts insurance costs. Avoiding accidents and traffic violations is crucial. Insurance companies often reward safe driving with lower premiums and even driver reward programs.

Impact of Credit Score on Insurance Rates

In many states, your credit score is a factor in determining your car insurance rates. A higher credit score generally leads to lower premiums, while a lower score can result in higher premiums. This is because a good credit score is often seen as an indicator of responsible financial behavior.

- Credit Score Improvement: Improving your credit score can be a significant way to lower your insurance costs. Strategies for improving your credit score include paying bills on time, reducing credit utilization, and addressing any errors on your credit report. Even a small improvement in your credit score can lead to noticeable savings on your insurance premiums.

Negotiating Lower Premiums

Don’t hesitate to negotiate your car insurance premiums. Insurance companies often have some flexibility in their pricing. Be prepared to discuss your driving record, policy details, and any discounts you qualify for.

- Loyalty Discounts: Inquire about loyalty discounts for long-term customers. Many insurers reward their loyal customers with reduced premiums.

- Competitive Quotes: Use quotes from other insurers as leverage during negotiations. This can encourage your current insurer to offer a more competitive rate.

- Bundling and Discounts: Highlight any potential discounts you qualify for, such as bundling multiple policies or having safety features in your vehicle.

Illustrative Examples

Understanding car insurance costs requires looking beyond simple risk assessments. Several factors interact in complex ways, leading to outcomes that may seem counterintuitive at first glance. The following examples illustrate how seemingly similar individuals can experience vastly different insurance premiums.

High-Risk Driver Finding Affordable Insurance

A young driver with a history of speeding tickets and a recent at-fault accident might seem destined for sky-high premiums. However, this driver could find more affordable insurance by taking a defensive driving course, installing a telematics device that monitors their driving habits, and opting for a higher deductible. The defensive driving course demonstrates a commitment to safer driving, potentially lowering their risk profile. Telematics data, showing improved driving behavior, can also influence premiums. A higher deductible, while requiring a larger upfront payment in case of an accident, significantly reduces the overall cost of the policy. Combining these strategies could yield surprisingly lower premiums than expected.

Low-Risk Driver Experiencing High Premiums

A middle-aged driver with a spotless driving record and a safe vehicle might be shocked to find their premiums unexpectedly high. This could be due to several factors. Living in a high-crime area with a high frequency of car thefts or accidents significantly increases premiums, regardless of the driver’s personal record. The make and model of their car, even if safe, could be a target for theft, thus increasing insurance costs. Additionally, certain optional add-ons, such as roadside assistance or rental car reimbursement, can significantly inflate the overall premium.

Bundling Insurance for Significant Savings

A homeowner with a car and renters insurance might save considerably by bundling their policies with the same insurance provider. Let’s say their car insurance costs $1200 annually, and their homeowners insurance costs $1500 annually. Bundling these policies could result in a discount of 15%, saving them $375 annually ($1200 + $1500 = $2700 * 0.15 = $405). Even a smaller discount, say 10%, would still represent a significant saving of $270. This is because insurance companies often reward loyalty and reduced administrative costs associated with managing multiple policies for a single client.

Visual Comparison of Insurance Costs

Imagine two bars representing insurance costs. The first bar, representing a young driver with multiple accidents and speeding tickets, is significantly taller, perhaps twice the height of the second bar. The second bar, representing an older driver with a clean driving record and a low-risk vehicle, is considerably shorter. The visual clearly demonstrates the impact of risk factors on insurance premiums. The taller bar could be labeled “High-Risk Driver: $2400/year,” while the shorter bar could be labeled “Low-Risk Driver: $1200/year.” This simple representation visually emphasizes the substantial difference in insurance costs based on risk profiles.

Final Review

Securing the cheapest car insurance doesn’t necessarily mean compromising on essential coverage. By carefully considering the factors influencing your premiums, actively comparing quotes from multiple providers, and employing smart strategies to reduce costs, you can find a policy that offers the right balance of affordability and protection. Remember, proactive research and a thorough understanding of your insurance options are key to making informed decisions and saving money.

Query Resolution

What is the difference between liability and collision coverage?

Liability coverage pays for damages you cause to others’ property or injuries you inflict on others in an accident. Collision coverage pays for damage to your own vehicle, regardless of fault.

Can I get car insurance if I have a poor driving record?

Yes, but you’ll likely pay higher premiums. Companies specializing in high-risk drivers exist, although the rates will generally be more expensive.

How often should I shop for car insurance?

It’s advisable to compare rates annually, or even more frequently, as rates can change based on many factors. This allows you to take advantage of any potential savings.

What is a SR-22 form?

An SR-22 is a certificate of insurance that proves you have the minimum required liability coverage. It’s often required by states after serious driving offenses.