Securing your financial future often involves navigating the complex world of life insurance. Understanding whole life insurance policy rates is crucial for making informed decisions that align with your long-term goals and financial capacity. This guide delves into the multifaceted factors influencing these rates, providing clarity and empowering you to make the best choice for your needs.

From the impact of age and health to the nuances of policy features and provider comparisons, we’ll unravel the intricacies of whole life insurance pricing. We’ll explore different policy types, offer strategies for managing costs, and provide illustrative examples to illuminate the process. By the end, you’ll possess a comprehensive understanding of how these rates are determined and how to find the most suitable policy for your circumstances.

Factors Influencing Whole Life Insurance Policy Rates

Several key factors interact to determine the cost of a whole life insurance policy. Understanding these factors empowers individuals to make informed decisions when selecting coverage. This section details how age, health, policy face value, policy type, and insurer influence premium calculations.

Age’s Impact on Whole Life Insurance Premiums

Age is a significant determinant of whole life insurance premiums. Younger applicants generally receive lower rates than older applicants because they have a statistically longer life expectancy. Insurers assess the risk of having to pay a death benefit sooner for older applicants, thus charging higher premiums to compensate for this increased risk. For example, a 30-year-old might pay significantly less than a 50-year-old for the same coverage amount. This difference reflects the actuarial tables used by insurance companies to predict longevity.

Health Status and Policy Costs

An applicant’s health status profoundly impacts premium costs. Individuals with pre-existing conditions or a history of health issues typically face higher premiums than those in excellent health. Insurers conduct thorough medical underwriting, reviewing medical history, lifestyle choices (such as smoking), and potentially requiring medical examinations to assess risk. Someone with a history of heart disease, for instance, will likely pay more than someone with a clean bill of health. This is because the insurer anticipates a higher probability of a claim being filed sooner.

Policy Face Value and Premium Amounts

The face value of the policy—the death benefit payable to the beneficiary—directly correlates with premium amounts. A higher face value necessitates a larger premium payment. This is intuitive: a larger death benefit represents a greater financial obligation for the insurer, requiring higher premiums to offset the increased risk. A $500,000 policy will, all else being equal, cost considerably more than a $100,000 policy.

Policy Type and Rate Differences: Participating vs. Non-Participating

Whole life insurance policies come in two main types: participating and non-participating. Participating policies, sometimes called mutual policies, offer the potential for dividends—a return of a portion of the premiums paid. These dividends are not guaranteed but are based on the insurer’s performance. Non-participating policies do not offer dividends. Generally, participating policies have slightly higher initial premiums than non-participating policies because of the potential dividend payout.

Rate Comparisons Among Insurance Providers

Premiums for similar whole life policies can vary considerably among different insurance providers. Factors such as the insurer’s financial strength, investment strategies, and operating costs all influence pricing. It’s crucial to compare quotes from multiple insurers to secure the most competitive rates. Shopping around and using online comparison tools can be beneficial in identifying the best value.

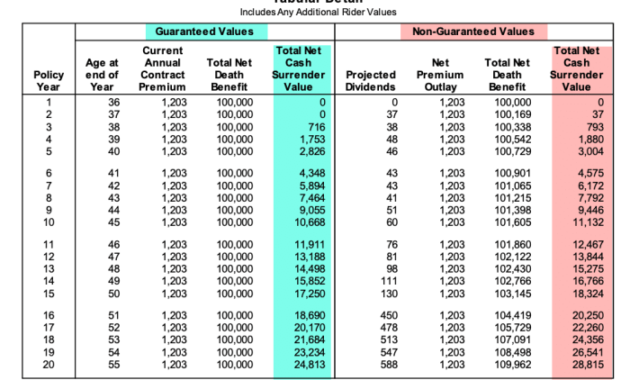

Premium Comparison Table

The following table illustrates how age and health status can influence whole life insurance premiums. Note that these are illustrative examples and actual rates will vary based on many factors including specific policy details and the insurer.

| Age | Excellent Health | Good Health | Fair Health |

|---|---|---|---|

| 35 | $500/year | $650/year | $800/year |

| 45 | $750/year | $950/year | $1200/year |

| 55 | $1200/year | $1500/year | $1800/year |

Understanding Policy Features and Their Cost Implications

Choosing a whole life insurance policy involves understanding how various features impact the overall cost. Premiums aren’t simply a flat rate; they’re influenced by several factors related to the policy’s design and your selected options. This section details these key aspects and their financial consequences.

Cash Value Accumulation and Premiums

The cash value component of a whole life policy directly influences premiums. A higher cash value accumulation generally leads to higher premiums, as the insurer is setting aside a portion of your payments to grow tax-deferred within the policy. Conversely, policies with lower cash value growth often have lower premiums. This is because less of your premium is allocated to the cash value component, and more goes towards the death benefit. For example, a policy emphasizing significant cash value growth might have premiums 15-20% higher than a similar policy with a more modest cash value component. The trade-off is between long-term savings and lower immediate cost.

Cost Differences Between Riders

Riders are optional additions to your whole life policy that enhance its coverage. However, these additions come at a cost. Accidental death benefit riders, for instance, increase the death benefit if the insured dies from an accident, but this increased coverage necessitates higher premiums. Similarly, long-term care riders provide coverage for long-term care expenses, adding a significant cost to the policy. The exact cost increase varies greatly depending on the specific terms and conditions of the rider, including the benefit amount and the length of coverage. A simple accidental death benefit rider might add only a few percent to the premium, while a comprehensive long-term care rider could substantially increase the premium, sometimes doubling or even tripling the base premium.

Payment Method and Overall Cost

The frequency of your premium payments affects the total cost due to interest. Paying annually typically results in the lowest overall cost because it avoids the interest charges associated with more frequent payments. Semi-annual or monthly payments often involve a small additional fee or a slightly higher premium to cover the insurer’s administrative costs of processing more frequent payments. While the difference may seem minimal per payment, it accumulates over the policy’s lifespan. For instance, a $1,000 annual premium might translate to $505 semi-annual payments or $85 monthly payments, representing a higher total cost over the year.

Dividend Options and Cost Over Time

Many whole life policies offer dividend options, which are essentially a return of a portion of the insurer’s profits. The choice of how to utilize these dividends impacts the overall cost and value of the policy over time. Options include taking the dividends as cash, using them to reduce premiums, adding them to the cash value, or purchasing paid-up additions to increase the death benefit. Choosing to use dividends to reduce premiums lowers the immediate cost, while applying them to the cash value enhances long-term growth. For example, consistently using dividends to reduce premiums could result in lower out-of-pocket expenses over the life of the policy, while reinvesting dividends in the policy’s cash value might lead to a higher overall cash value at maturity, although the immediate cost remains higher.

Comparison of Policy Costs with Various Riders

| Policy Type | Base Premium (Annual) | Accidental Death Benefit Rider | Long-Term Care Rider |

|---|---|---|---|

| Basic Whole Life | $1000 | +$50 | +$300 |

| Whole Life with Cash Value Emphasis | $1200 | +$60 | +$400 |

| Whole Life with Higher Death Benefit | $1500 | +$75 | +$500 |

Exploring Different Whole Life Insurance Policy Types

Whole life insurance offers lifelong coverage, but the specific type of policy significantly impacts premium costs and cash value growth. Understanding the nuances of traditional, universal, and variable whole life insurance is crucial for making an informed decision that aligns with individual financial goals and risk tolerance. This section compares and contrasts these policy types, focusing on premium structures and the relationship between death benefits and cash value accumulation.

Traditional Whole Life Insurance

Traditional whole life insurance policies offer a fixed death benefit and a fixed premium payment schedule for the insured’s entire life. The premiums remain constant, providing predictability and financial stability. Cash value grows at a guaranteed rate, though this rate is typically lower than other types of whole life policies. The policy’s cash value can be borrowed against or withdrawn, but this will reduce the death benefit and may impact the policy’s overall value.

- Key Feature: Fixed premiums and death benefit.

- Cost Implications: Premiums are generally higher than term life insurance, but lower than universal or variable whole life policies with comparable death benefits. Cash value growth is slower and predictable.

- Death Benefit and Cash Value Growth: Death benefit remains constant throughout the policy’s life. Cash value grows at a predetermined rate, often compounded annually.

Universal Whole Life Insurance

Universal whole life insurance provides a flexible premium payment structure and a death benefit that can be adjusted over time. Policyholders can pay more than the minimum premium to increase cash value accumulation, or they can pay less (subject to minimums) in certain circumstances. The cash value grows at a rate that is typically tied to a current interest rate, meaning the growth can fluctuate. This flexibility allows for greater control over premium payments and cash value growth, but it also introduces more risk.

- Key Feature: Flexible premiums and adjustable death benefit.

- Cost Implications: Premiums are generally more flexible than traditional whole life, allowing for adjustments based on financial circumstances. However, the interest rate credited to the cash value can fluctuate, impacting overall growth.

- Death Benefit and Cash Value Growth: Death benefit can be adjusted upwards or downwards, subject to policy terms and conditions. Cash value growth is influenced by the credited interest rate, which can vary over time.

Variable Whole Life Insurance

Variable whole life insurance offers a fixed premium payment structure, but the cash value growth is tied to the performance of underlying investment options chosen by the policyholder. This introduces a higher degree of risk, as the cash value growth can fluctuate significantly depending on market conditions. The death benefit also varies based on cash value accumulation.

- Key Feature: Fixed premiums, variable cash value growth linked to investment performance.

- Cost Implications: Premiums are generally higher than traditional whole life insurance to account for the potential for greater cash value growth. However, there is also a greater risk of lower cash value growth if investments underperform.

- Death Benefit and Cash Value Growth: Death benefit increases with the cash value growth, which is directly influenced by the performance of the selected investment options. This introduces market risk.

Strategies for Managing Whole Life Insurance Costs

Securing whole life insurance is a significant financial commitment, but understanding strategies for managing costs can make it more manageable and affordable. This section Artikels practical methods for obtaining competitive rates and maintaining affordability over the policy’s lifespan. Careful planning and proactive steps can significantly impact your overall cost.

Obtaining the Most Competitive Rates

Several factors influence the rates you receive. Your health, age, lifestyle, and the policy’s features all play a role. To secure the most competitive rates, it’s crucial to shop around and compare quotes from multiple insurers. Consider working with an independent insurance agent who can access a broader range of providers and policies, often securing better rates than you could find independently. Furthermore, applying for insurance when you are younger and healthier will generally result in lower premiums. Finally, consider carefully the amount of coverage you truly need; purchasing more coverage than necessary will increase your premium.

Maintaining Affordability Over the Long Term

Whole life insurance premiums are typically level, meaning they remain the same throughout the policy’s duration. However, unexpected financial challenges can still impact your ability to maintain payments. To ensure long-term affordability, regularly review your budget and consider setting aside funds specifically for premium payments. Exploring options like paying annually instead of monthly can often result in lower overall costs due to reduced administrative fees. Furthermore, regularly reviewing your policy and adjusting coverage levels as your needs change can help to maintain affordability. For example, if your financial circumstances change significantly, you might consider reducing the death benefit to lower your premiums.

Comparing Quotes from Different Insurance Providers

A step-by-step guide to comparing quotes is crucial for finding the best value.

- Gather Information: Determine your desired coverage amount, policy type, and any specific riders you want.

- Obtain Quotes: Request quotes from at least three different insurance providers. Use online quote tools or contact insurers directly.

- Analyze Quotes: Compare premiums, death benefits, cash value growth projections, and any fees or charges. Pay close attention to the fine print.

- Consider Policy Features: Evaluate the policy features offered by each provider and how they align with your needs and budget.

- Verify Provider Ratings: Check the financial strength ratings of the insurance companies from independent rating agencies like A.M. Best, Moody’s, or Standard & Poor’s to ensure their stability.

- Make a Decision: Based on your analysis, choose the policy that best meets your needs and budget.

Identifying and Avoiding Hidden Fees or Charges

Hidden fees can significantly increase the overall cost of your policy. Carefully review the policy documents for charges like surrender charges (penalties for withdrawing cash value early), administrative fees, and policy fees. Compare these fees across different providers. Ask specific questions to clarify any unclear charges. Don’t hesitate to seek a second opinion from an independent insurance professional if you have concerns about any fees or charges listed. Transparency regarding fees is a key indicator of a reputable insurer.

Securing the Best Whole Life Insurance Policy Rates: A Flowchart

The flowchart would visually represent the steps involved in securing the best rates. It would start with assessing your needs and budget, followed by obtaining quotes from multiple insurers, comparing policy features and costs, verifying provider ratings, and finally, selecting the most suitable policy. Each step would be clearly indicated with connecting arrows to illustrate the process flow. For example, a box might say “Compare Premiums and Fees,” connecting to a box that says “Choose Best Policy.” The visual representation of this process would help individuals navigate the complexities of choosing a policy effectively.

Illustrative Examples of Whole Life Insurance Premiums

Understanding the cost of whole life insurance requires considering several factors. This section provides two illustrative examples demonstrating how age, policy value, and health status influence premium calculations. Remember that these are examples only, and actual premiums will vary depending on the specific insurer and policy details.

Premium Cost for a 35-Year-Old Male with a $250,000 Policy

Let’s consider a healthy 35-year-old male who purchases a $250,000 whole life insurance policy. Several factors contribute to his premium cost. His age is a key factor; younger individuals generally receive lower premiums due to their statistically lower risk of death in the near term. His health status also plays a significant role. Assuming he is in excellent health with no pre-existing conditions, this will result in a lower premium. The type of policy chosen (e.g., participating vs. non-participating) also affects the cost, with participating policies often having slightly higher premiums but potentially offering dividends. Finally, the insurer’s underwriting process and their specific risk assessment models will influence the final premium. In this scenario, a reasonable estimate for his annual premium might be between $500 and $1,000, depending on the specific policy features and insurer.

Premium Cost for a 50-Year-Old Female with a $500,000 Policy

Now, let’s consider a 50-year-old female purchasing a $500,000 whole life insurance policy. Her age is a significant factor increasing the premium compared to the younger male in the previous example. Statistically, the risk of mortality increases with age, leading to higher premiums. Assuming she is in good health, her premium will still be affected by her age. The higher policy value of $500,000 also significantly impacts the cost; a larger death benefit necessitates a higher premium. Similar to the previous example, the specific policy type and the insurer’s underwriting will further refine the premium. A reasonable estimate for her annual premium might range from $2,000 to $4,000, reflecting the combined influence of age and policy value.

Comparison of Scenarios

The two scenarios highlight the significant impact of age and policy value on whole life insurance premiums. The 35-year-old male receives a considerably lower premium due to his younger age and lower policy value. The 50-year-old female faces substantially higher premiums due to her older age and the larger death benefit. This illustrates the importance of considering these factors when planning for whole life insurance coverage and budgeting for premiums. The difference between the estimated premiums reflects the increased risk associated with older age and larger policy amounts. It’s crucial to remember that these are illustrative examples and actual premiums will vary based on individual circumstances and insurer practices.

Final Review

Choosing a whole life insurance policy is a significant financial commitment, and understanding the factors driving policy rates is paramount. This guide has provided a framework for navigating this complexity, equipping you with the knowledge to compare policies effectively, manage costs strategically, and ultimately, secure a policy that provides the necessary protection and aligns with your individual financial situation. Remember to consult with a financial advisor for personalized guidance.

Commonly Asked Questions

What is the difference between participating and non-participating whole life insurance?

Participating policies offer dividends based on the insurer’s performance, potentially lowering the overall cost over time. Non-participating policies have fixed premiums and no dividends.

Can I change my payment method after purchasing a policy?

Generally, yes, but there may be administrative fees associated with the change. Contact your insurer to understand their specific procedures and any potential cost implications.

How often should I review my whole life insurance policy?

It’s advisable to review your policy annually or at least every few years to ensure it still meets your needs and financial situation. Life circumstances change, and your coverage requirements may evolve accordingly.

What happens to my cash value if I cancel my whole life insurance policy?

The cash value accumulation is typically returned to you, minus any surrender charges that may apply depending on the policy’s terms and the length of time the policy has been in effect.

Are there tax implications associated with whole life insurance policies?

Yes, there are potential tax implications depending on how the policy is structured and used. Consult with a tax professional to fully understand the tax ramifications of your specific policy.