Whole life insurance often evokes images of complex financial instruments, but its core purpose is remarkably simple: providing lifelong financial protection for your loved ones while simultaneously offering potential long-term growth. This guide unravels the intricacies of whole policy life insurance, demystifying its features, benefits, and potential drawbacks to empower you with the knowledge needed to make informed decisions about your financial future.

We’ll explore the fundamental differences between whole life and term life insurance, delve into the mechanics of cash value accumulation, and examine how whole life policies can serve as powerful tools in estate planning and wealth accumulation. We’ll also analyze the costs involved, compare them to alternative investment strategies, and discuss the potential tax advantages this type of insurance offers.

Defining Whole Life Insurance

Whole life insurance provides lifelong coverage, offering a death benefit payable to your beneficiaries upon your passing. Unlike term life insurance, which covers a specific period, whole life insurance remains in effect as long as premiums are paid. This enduring protection is coupled with a cash value component that grows over time, offering a unique blend of insurance and investment.

Whole life insurance policies offer several key features. These policies build cash value, a tax-deferred savings component that grows over time. Policyholders can borrow against this cash value or withdraw it, subject to certain conditions and potential tax implications. The death benefit remains in place, ensuring financial security for your loved ones. Premiums are typically level, meaning they remain constant throughout the policy’s duration, offering predictable financial planning. Dividends, which are not guaranteed, may be paid by some insurers, further enhancing the policy’s value.

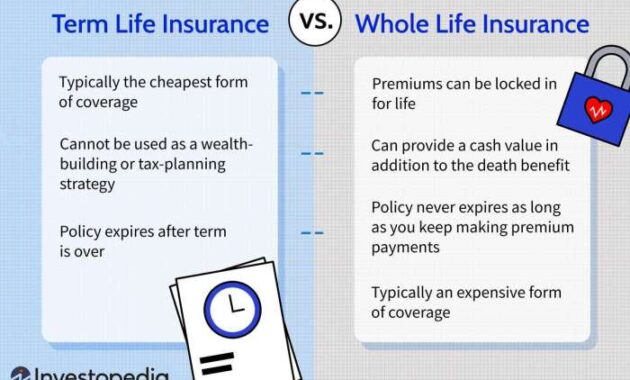

Whole Life vs. Term Life Insurance

The primary difference between whole life and term life insurance lies in the coverage duration. Term life insurance provides coverage for a specific period (e.g., 10, 20, or 30 years), after which the policy expires. Whole life insurance, conversely, offers lifelong coverage, provided premiums are consistently paid. Term life insurance premiums are generally lower than whole life premiums because they only cover a defined period. Whole life insurance, due to its permanent nature and cash value accumulation, comes with higher premiums. Term life insurance typically does not build cash value, while whole life insurance does. The choice between the two depends largely on individual financial goals and risk tolerance. Someone with a shorter-term need for coverage, such as paying off a mortgage, might opt for term life insurance. Individuals seeking lifelong coverage and a savings vehicle might prefer whole life insurance.

Cash Value Component in Whole Life Insurance

The cash value component of a whole life insurance policy is a significant feature distinguishing it from term life insurance. This component grows over time, accumulating tax-deferred interest. The growth rate is not guaranteed and varies depending on the insurer’s investment performance and the type of policy. Policyholders can borrow against this cash value, often at a favorable interest rate, without affecting the death benefit. However, outstanding loans reduce the death benefit paid to beneficiaries. Withdrawals from the cash value are possible, but they may impact the policy’s death benefit and cash value accumulation. The cash value can be a valuable source of funds for various financial needs, such as retirement planning or education expenses, offering a flexible and tax-advantaged savings vehicle.

Using Whole Life Insurance in Financial Planning

Whole life insurance can serve several purposes in a comprehensive financial plan. It provides a guaranteed death benefit, protecting loved ones from financial hardship upon the policyholder’s death. The cash value component can act as a long-term savings vehicle, accumulating funds for retirement or other significant expenses. It can provide a source of funds for emergencies or unexpected financial needs, offering flexibility and financial security. For example, a family might use whole life insurance to cover college tuition costs or to fund a child’s future. A business owner could utilize the cash value component as a source of funds for business expansion or succession planning. Furthermore, the death benefit can provide financial stability for the business in the event of the owner’s demise. These uses illustrate the versatility of whole life insurance in meeting diverse financial objectives.

Understanding Policy Costs and Benefits

Whole life insurance offers lifelong coverage, but understanding its costs and benefits is crucial before purchasing a policy. Premiums, long-term costs, and potential tax advantages all play significant roles in determining the overall value proposition. This section will delve into these key aspects to provide a clearer picture of whole life insurance’s financial implications.

Factors Influencing Whole Life Insurance Premiums

Several factors contribute to the premium amount you’ll pay for a whole life insurance policy. These factors are carefully assessed by insurance companies to accurately reflect the risk associated with insuring your life. Age is a primary factor; younger individuals generally pay lower premiums due to their statistically longer life expectancy. Health status also significantly impacts premiums, with individuals in excellent health typically receiving more favorable rates. Lifestyle choices, such as smoking or engaging in high-risk activities, can increase premiums. The policy’s face value – the death benefit – is directly proportional to the premium; a higher death benefit means higher premiums. Finally, the type of policy chosen (participating or non-participating, as discussed later) influences premium costs.

Long-Term Cost Comparison with Other Investment Options

Whole life insurance is often compared to other long-term investment options, such as mutual funds or index funds. While whole life insurance provides a guaranteed death benefit and cash value growth (albeit at a slower pace than some other investments), other investment vehicles may offer higher potential returns, but with significantly higher risk. For example, a well-diversified mutual fund portfolio might offer higher returns over the long term than the cash value growth within a whole life policy, but it also carries the risk of market fluctuations and potential losses. The choice depends heavily on individual risk tolerance and financial goals. A financial advisor can help assess the suitability of whole life insurance relative to other investment options based on your specific circumstances.

Potential Tax Advantages of Whole Life Insurance

Whole life insurance policies offer certain tax advantages that can make them attractive to some individuals. Death benefits paid to beneficiaries are generally tax-free, providing significant financial relief to the family during a difficult time. Furthermore, the cash value accumulated within the policy grows tax-deferred, meaning you don’t pay taxes on the earnings until you withdraw them. However, it’s crucial to consult a tax professional to understand the specific tax implications based on your individual situation and the intricacies of the policy structure. Tax laws are subject to change, and professional advice ensures compliance.

Comparison of Whole Life Insurance Policy Structures

The following table compares participating and non-participating whole life insurance policies:

| Feature | Participating Whole Life | Non-Participating Whole Life |

|---|---|---|

| Premiums | Generally higher | Generally lower |

| Dividends | Potentially pays dividends based on the insurer’s performance | No dividends |

| Cash Value Growth | Cash value growth can be influenced by dividends | Cash value growth is fixed |

| Flexibility | May offer more flexibility in terms of premium payments and policy adjustments | Less flexible |

Risk Assessment and Policy Selection

Choosing the right whole life insurance policy requires a careful assessment of your individual risk profile and financial goals. Understanding your needs and the policy’s features is crucial to making an informed decision. This section will guide you through the process of evaluating your risk and selecting a suitable policy.

Factors in Individual Risk Assessment

Several factors contribute to an individual’s risk profile and influence the cost and suitability of a whole life insurance policy. These include age, health status (including pre-existing conditions and family history of illness), lifestyle choices (smoking, alcohol consumption, risky hobbies), occupation (level of risk involved), and financial situation. Insurers use this information to assess the likelihood of a claim and determine the appropriate premium. For example, a younger, healthier individual with a low-risk occupation will generally receive a lower premium than an older individual with pre-existing health conditions and a high-risk job. Accurate and complete information is crucial for obtaining an accurate assessment.

Step-by-Step Guide to Policy Selection

Selecting an appropriate whole life insurance policy involves a systematic approach.

- Determine your insurance needs: Consider the amount of coverage needed to protect your beneficiaries in the event of your death. This should account for outstanding debts, future expenses, and desired legacy for your family.

- Compare policy options from multiple insurers: Obtain quotes from several reputable insurance companies to compare premiums, benefits, and policy features. Consider factors like cash value growth potential, dividend options, and riders.

- Review policy details carefully: Thoroughly examine the policy documents, paying close attention to the terms and conditions, exclusions, and any limitations on benefits.

- Seek professional advice: Consult with a qualified financial advisor or insurance broker to discuss your individual circumstances and receive personalized recommendations. They can help you navigate the complexities of insurance policies and choose the best option for your needs.

- Make an informed decision: Based on your needs, risk assessment, and professional advice, select the policy that best aligns with your financial goals and long-term objectives.

Key Aspects to Consider Before Purchasing

Before committing to a whole life insurance policy, it is vital to consider several key aspects:

- Premium affordability: Ensure the ongoing premiums are manageable within your budget throughout your lifetime.

- Policy benefits and features: Understand the coverage amount, death benefit, cash value accumulation, and any additional riders or benefits included.

- Insurer’s financial stability: Choose a financially sound and reputable insurance company with a strong track record.

- Flexibility and adjustability: Assess the policy’s flexibility in terms of premium payments, coverage adjustments, and loan options.

- Long-term financial implications: Consider the long-term cost of the policy and its impact on your overall financial plan.

Decision-Making Flowchart

A flowchart illustrating the decision-making process could be represented as follows:

[Imagine a flowchart here. The flowchart would begin with “Assess your needs and risk profile.” This would branch to “Compare policy options from different insurers.” This would then branch to “Review policy details and seek professional advice.” Finally, this would lead to “Select the most suitable policy.” Each step could have additional branching for considerations like budget, health, and long-term goals.] The flowchart visually guides the decision-making process, ensuring all critical factors are considered before a final selection.

Investment Aspects of Whole Life Insurance

Whole life insurance policies offer a unique blend of life insurance coverage and a cash value component that grows over time. Understanding how this cash value functions as an investment is crucial for assessing the policy’s overall value. This section will explore the investment features of whole life insurance, comparing its potential returns to other investment options and outlining associated risks.

The cash value component of a whole life policy accumulates through a portion of your premiums being invested by the insurance company. This investment growth is generally tax-deferred, meaning you won’t pay taxes on the earnings until you withdraw them. The growth rate isn’t fixed and depends on the insurance company’s investment performance and the specific policy’s terms. It’s important to remember that this is not a high-risk, high-reward investment; it’s designed for long-term, steady growth, offering a degree of stability and security compared to more volatile investments.

Cash Value Growth Mechanisms

The cash value in a whole life policy grows primarily through two mechanisms: the accumulation of premiums and the interest earned on the cash value. Premiums paid beyond the cost of insurance are added to the cash value. The insurer then credits interest to this cash value, typically at a rate that is specified in the policy and is often tied to a particular index or a fixed rate. The credited interest rate is not guaranteed and may fluctuate over time.

Comparison with Other Investment Options

Whole life insurance’s potential returns should be compared against other investment vehicles such as stocks, bonds, mutual funds, and real estate. Stocks offer the potential for higher returns but also carry significantly higher risk. Bonds provide more stability but typically offer lower returns. Mutual funds offer diversification, but their returns also vary depending on market conditions. Real estate investment can yield substantial returns, but it is illiquid and requires considerable management. Whole life insurance occupies a middle ground, offering a balance between growth and security, though its returns generally lag behind those of higher-risk investments during periods of strong market performance.

Risks Associated with Whole Life Insurance Investments

Investing in whole life insurance carries several risks. The primary risk is that the cash value growth may not keep pace with inflation or other investment options, especially during periods of high market returns. The credited interest rate, as previously mentioned, is not guaranteed and may be lower than anticipated. Policy fees and expenses can also erode the cash value’s growth. Furthermore, surrendering the policy early may result in significant penalties and a loss of accumulated cash value. Finally, the insurance company’s financial stability is a factor to consider.

Hypothetical Long-Term Growth Scenarios

Let’s consider two hypothetical scenarios illustrating long-term cash value growth under different market conditions.

Scenario 1: Stable Market Assume a $10,000 annual premium for a whole life policy with an average annual credited interest rate of 4% over 30 years. The total cash value at the end of 30 years could be approximately $750,000 (this is a simplified example and does not account for all fees and charges). This scenario assumes a consistently stable market environment.

Scenario 2: Volatile Market Assume the same $10,000 annual premium, but with fluctuating credited interest rates reflecting a volatile market. In some years, the credited interest rate might reach 6%, while in others it might fall to 2%. The final cash value after 30 years might be significantly lower or higher than in Scenario 1, depending on the specific fluctuations. This highlights the uncertainty inherent in projecting long-term growth.

It’s crucial to understand that these are simplified examples and actual results will vary depending on many factors including the specific policy terms, the insurance company’s investment performance, and market conditions.

Illustrative Examples and Case Studies

Understanding the practical applications of whole life insurance is crucial. The following examples illustrate how this type of policy can be a valuable tool in various financial situations, spanning estate planning to long-term wealth accumulation.

Whole Life Insurance as a Suitable Financial Planning Tool

Consider a young professional, Sarah, aged 30, with a growing family and a stable income. She anticipates future educational expenses for her children and wishes to secure her family’s financial future in the event of her untimely demise. A whole life insurance policy provides a death benefit to cover these potential costs, while also offering a cash value component that grows tax-deferred over time. This cash value can be accessed for emergencies or significant future expenses like retirement, providing a flexible financial safety net. The policy’s predictable premiums allow for budgeting and long-term financial stability.

A Case Study Illustrating Long-Term Benefits

Let’s examine the case of Mr. Jones, who purchased a $250,000 whole life policy at age 40. Over 30 years, the policy’s cash value grew significantly due to consistent premium payments and the policy’s interest accumulation. Upon retirement at age 70, he accessed a portion of his cash value to supplement his retirement income without jeopardizing the death benefit for his heirs. This illustrates how whole life insurance can act as a long-term savings vehicle and provide a reliable income stream in retirement. The death benefit also remained intact, ensuring a financial legacy for his family.

Using Whole Life Insurance for Estate Planning

A whole life insurance policy can be a powerful tool for estate planning. It provides a guaranteed death benefit that passes to your beneficiaries outside of probate, ensuring a smooth transfer of assets and minimizing potential delays or legal complications. The death benefit can be used to pay estate taxes, cover funeral expenses, or provide financial support for surviving family members. Furthermore, the policy’s cash value can be used to fund trusts or other estate planning vehicles.

Hypothetical Illustration of Cash Value Accumulation

The following table illustrates the hypothetical growth of cash value in a $250,000 whole life policy over 20 years, assuming a conservative annual interest rate of 4%. This is a simplified illustration and actual returns may vary based on the specific policy and market conditions. It’s important to consult with a financial advisor for personalized projections.

| Year | Cash Value (Approximate) |

|---|---|

| 5 | $25,000 |

| 10 | $60,000 |

| 15 | $110,000 |

| 20 | $175,000 |

Final Conclusion

Securing your family’s financial well-being is a cornerstone of responsible financial planning. Whole policy life insurance, while complex, offers a unique blend of protection and potential investment growth. By carefully considering your individual risk profile, financial goals, and understanding the associated costs and benefits, you can determine if a whole life policy aligns with your long-term financial strategy. Remember to consult with a qualified financial advisor to personalize your approach and ensure your choices are tailored to your specific circumstances.

User Queries

What are the main differences between participating and non-participating whole life insurance policies?

Participating policies offer dividends based on the insurer’s performance, potentially increasing cash value. Non-participating policies have fixed premiums and cash value growth, offering predictability but potentially lower returns.

Can I borrow against the cash value of my whole life insurance policy?

Yes, most whole life policies allow you to borrow against the accumulated cash value. Interest is typically charged on these loans, and failure to repay could impact the policy’s death benefit.

How is the cash value in a whole life policy taxed?

Growth in cash value is generally tax-deferred. However, withdrawals or loans may be subject to taxes and penalties depending on your specific circumstances. Consult a tax professional for personalized advice.

What happens to my policy if I stop paying premiums?

If premiums are not paid, the policy may lapse, resulting in the loss of the cash value and the death benefit. However, some policies offer grace periods or options to reinstate coverage.